1. Declaration of Value-Added Tax

- Value-Added Tax should only be declared when there is an original invoice or tax payment receipt. If the original document is not available or not yet available, do not declare. Note that the original invoice must be demanded under conditions to facilitate declaration when requested.

- Use tax payment receipts to declare imported goods. Only declare when there is a tax payment receipt. If you declare before the period stated in the tax payment receipt, you will be penalized for incorrect tax declaration behavior and may be fined for late payment of value-added tax. After declaring taxes and submitting tax reports, you should export the declaration to a Word or Excel file and keep it until tax settlement.

- When you see the HTKK3.3.0 form, you still need to enter all the data because it will be used for tax settlement. In many cases, the new form may not have explanations and data entry is not done until settlement, requiring continuous data entry. Moreover, you also need a reconciliation table.

2. Goods

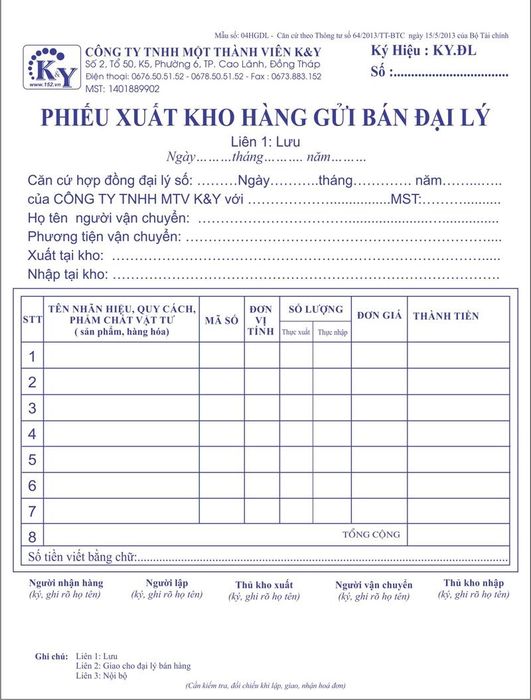

All goods leaving the warehouse must be invoiced, including promotional items, internal goods, warranty items, and inventory items to be liquidated due to quality issues. Invoices are frequently scrutinized and requested for explanation. Issuing invoices and declaring both output and input VAT fulfills your obligations. For instance, inventory items must be checked against the year-end inventory report to ensure accuracy and prepare explanations for discrepancies. Is there excessive inventory? Have all outgoing and incoming slips been properly signed and stamped? If not, request rectification immediately after inspection.

3. Cash and Cash Equivalents

- When your company borrows money from a bank, you should not keep the highest cash reserve, especially when banks disburse funds. If the cash reserve is too high, you need to create an expense voucher to reduce it. For example, expenses for marketing, parties, conferences, etc., any expenses without invoices should be recorded. The purpose of this is to reduce the reserve, so record as many as possible but it must be reasonable to avoid tax settlement issues.

- The cash reserve of your company should not be negative. In case of cash shortage, as an accountant, you must make a loan agreement with a higher authority or a major shareholder with a 0% interest rate per month. After the cash reserve of the company has increased, you should proceed to liquidate that loan agreement to repay it.

4. Storage of Inbound Invoices

- Inbound invoices should be hole-punched, bound into a ledger by month or quarter, and managed accordingly. Arrange them in the same order as the VAT declaration form for easy retrieval.

- You may print one or two ledger books (e.g., 133 ledger) reconciled with the company's purchase ledger to cross-check end-of-period balances and transaction discrepancies between the tax report and the accounting ledger.

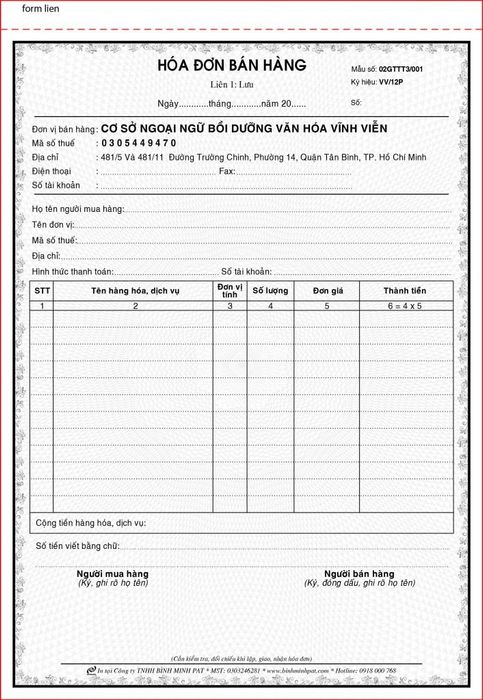

5. Storage of Outbound Invoices

- All invoices should be sequentially numbered within each ledger for easy retrieval if the invoices don't already have sequential numbers.

- In the case of canceled invoices, list the canceled numbers and attach sticky notes to the cover of the ledger. Besides, maintain this information in an Excel file for consistent data management across the company.

- The tax authority's verification of canceled invoices will involve cross-referencing invoice usage with the outbound ledger. They may even inspect the actual invoice ledger to verify the authenticity of canceled invoices or any errors. Mainly, they check if there is documentation accompanying the canceled invoice to avoid penalties. For canceled invoices returned by customers, affix them directly onto the ledger before tearing them and attach the cancellation notice alongside.

6. Non-Commercial Goods Transactions

Non-commercial goods transactions refer to items supplied or gifted for demonstration purposes, incurring import taxes, VAT, and shipping costs without monetary exchange. VAT remains deductible if the items are used for business purposes and not sold. However, no invoices can be issued if the goods are damaged and sold by your company.

7. Bills Exceeding 20 Million

Bills exceeding 20 million must be settled via electronic transfer. Upon payment, it is advisable to attach a copy of the payment order or clearly note the payment date on the invoice. Tax authorities will verify the presence of the payment order. Failure to provide the payment order may result in non-deductible VAT for the company.

8. Expense Allocation

- During expense allocation, it's essential to categorize expenses properly, separating reasonable from unreasonable ones for easier settlement.

- You can utilize account 6423 for allocating all expenses without invoices, excluded invoices, or sensitive company expenses.

9. Ledger

- You must maintain all primary ledgers and subsidiary ledgers on a monthly basis for your company, including subsidiary ledgers, debit notes, credit notes, accompanying documents such as (payment authorizations, deposit slips, payment orders, receipt orders, etc.). It's advisable to keep an annual backup for smooth operations.

- Additionally, prepare physical subsidiary ledgers and soft file ledgers extracted from Internet Banking to facilitate the settlement process. If your company hasn't registered for Internet Banking, it's recommended to request your superiors to proceed with the registration.

- Avoid engaging in business with ghost companies. Dealing with such entities may result in legitimate taxes like input value-added tax being excluded from reasonable expenses and penalties for various offenses such as administrative fines, late tax payments, fraudulent acts, tax evasion, etc. Therefore, it's crucial to thoroughly verify partners associated with your company.

10. Miscellaneous Expenses

- If your company operates at a loss in any year, miscellaneous expenses such as 13th-month salary bonuses, Tet holiday gifts for customers will not be considered reasonable expenses. Therefore, you only need to record them as general business expenses.

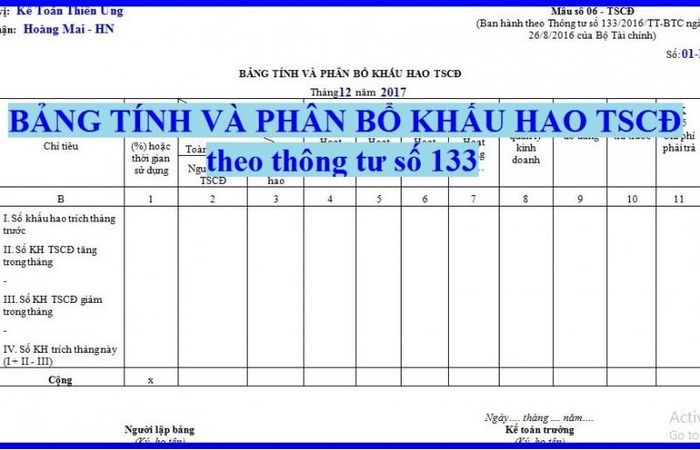

- The allocation table for fixed asset depreciation, equipment, and supplies must have clear soft copies. You need to review the fixed asset records regarding items such as: input invoices, installation expense invoices, purchase and sale contracts, asset handover records, acceptance records, cards. Then, reconcile them with the generated balance sheet.

- Check depreciation, ensure the company has registered depreciation with the tax authorities. If not, you must request superiors to register depreciation to protect the company's interests.