In some cases, calculating the interest earned from a savings account is as simple as multiplying the interest rate by the principal amount. However, this is not always the case. For example, many savings accounts offer an annual interest rate but compound interest on a monthly basis. Each month, a portion of the interest is calculated and added to the principal, affecting the interest for the following months. This gradual and continuous addition to the principal is called compound interest, and the easiest way to calculate future earnings is by using the compound interest formula. Continue reading to learn more about the advantages and disadvantages of this method of calculation.

Steps

Calculate Compound Interest

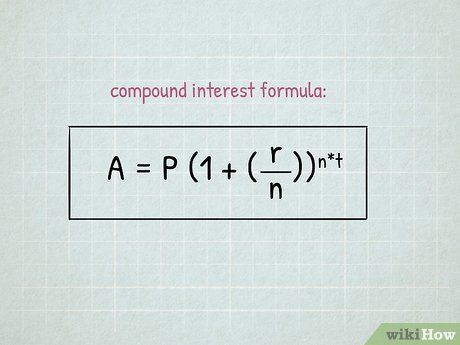

Understand the formula for calculating the impact of compound interest.

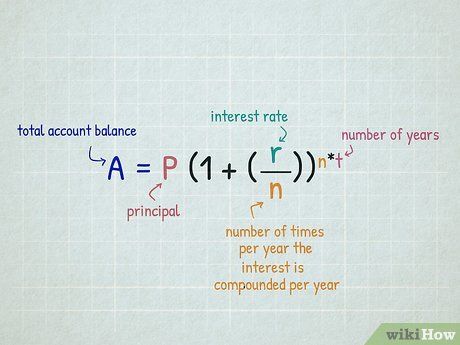

Understand the formula for calculating the impact of compound interest.- (P) is the principal amount, (r) is the annual interest rate, and (n) represents the number of times interest is compounded per year. (A) is the account balance calculated under the influence of compound interest.

- (t) is the time over which interest is accumulated. This number should correspond to the interest rate used (for example, if the interest is calculated annually, (t) should be the number or fraction of a year). If the period is shorter than a year, divide the total months by 12 or the total days by 365.

Identify the variables used in the formula. Review the terms of your personal savings account or contact your bank representative to input values into the equation.

- Principal (P) is the initial deposit or the amount currently available used to calculate the interest.

- The interest rate (r) should be written as a decimal. For example, 3% should be entered as 0.03. To convert, simply divide 3 by 100.

- The value (n) is the number of times interest is calculated and added to the principal (compound interest) in a year. The most common compounding frequencies are monthly (n=12), quarterly (n=4), and annually (n=1). However, there may be other options depending on the specific terms of your savings account.

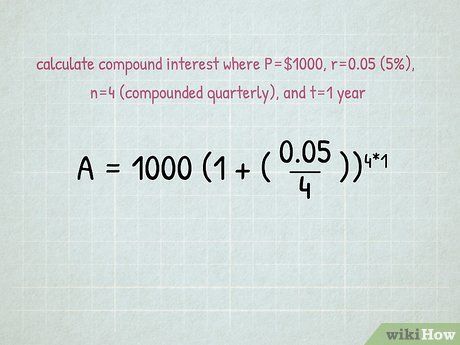

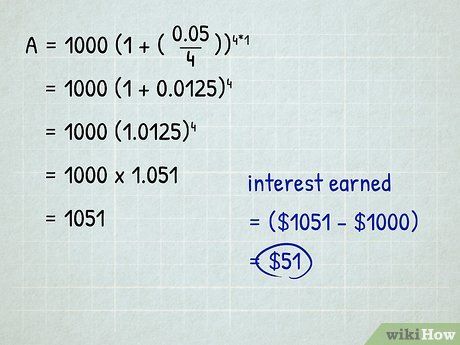

Insert values into the formula.

Insert values into the formula.- Compound interest calculated daily follows the same method, except in this case, the variable (n) is 365 instead of 4 as previously stated.

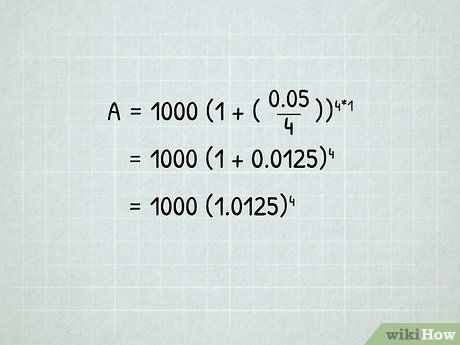

Proceed with the calculation.

Proceed with the calculation. Solve the equation.

Solve the equation.Calculating interest with regular contributions

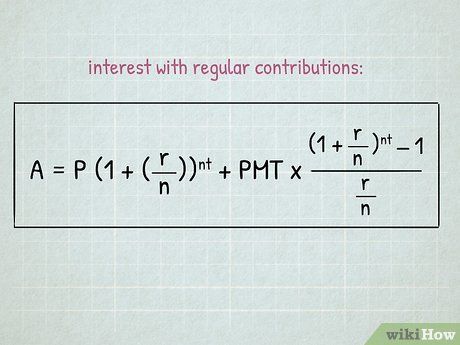

First, apply the accumulation savings formula.

First, apply the accumulation savings formula.- Another simple method is to separate the compound interest of the principal from the interest earned from additional contributions (or payments/PMT). To begin, calculate the interest on the principal using the accumulation savings formula.

- This formula allows you to compute the interest earned on a savings account that receives monthly deposits, as well as compound interest based on daily, monthly, or quarterly periods.

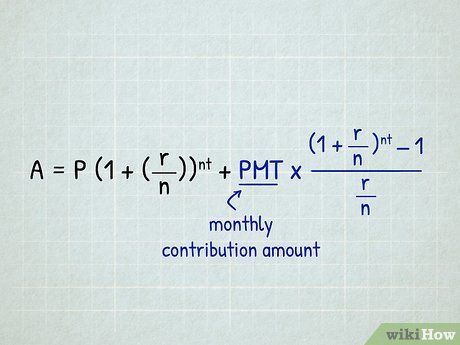

Use the second part of the formula to calculate the interest on contributions. (PMT) represents the monthly contributions made.

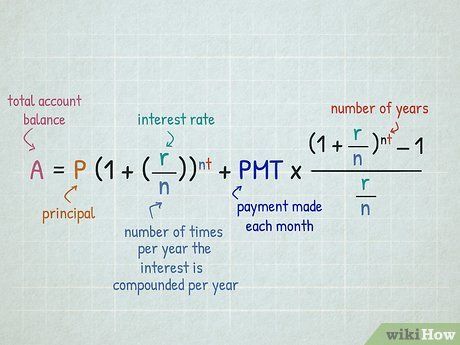

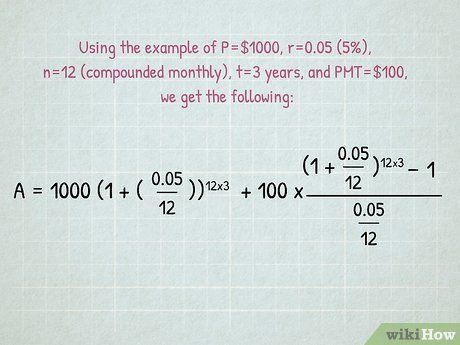

Identify the variables. Review your investment or savings agreement to find the following variables: principal "P", annual interest rate "r", and the number of periods per year "n". If these are not readily available, contact your bank. The variable "t" represents the number of years or part of a year used for interest calculation, and "PMT" is the monthly contribution/payment amount. "A" is the total account value calculated based on the time and contributions specified.

- The principal "P" can also represent the account value at the chosen starting point for interest calculations.

- The interest rate "r" indicates the annual rate paid to the account. It should be expressed as a decimal in the formula. For example, a 3% interest rate should be written as 0.03. To get this decimal, simply divide the percentage by 100.

- "n" is the number of compounding periods in a year. This would be 365 if compounded daily, 12 for monthly compounding, and 4 for quarterly compounding.

- Similarly, "t" represents the time in years used for calculating interest. It can be in whole years or as a fraction if the time is less than one year (e.g., 0.0833 for one month, which is 1/12 of a year).

Substitute the values into the formula.

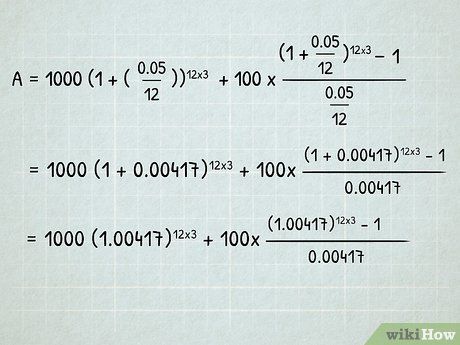

Substitute the values into the formula. Simplify the equation.

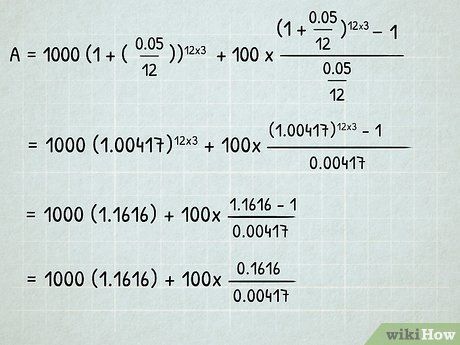

Simplify the equation. Calculate the power.

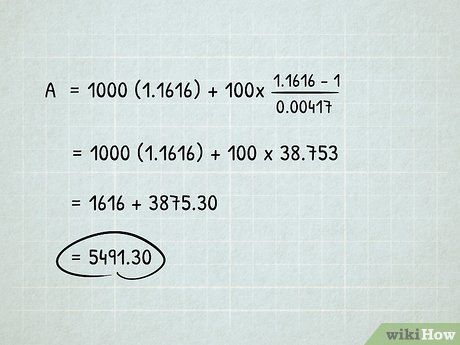

Calculate the power. Proceed with the final calculations.

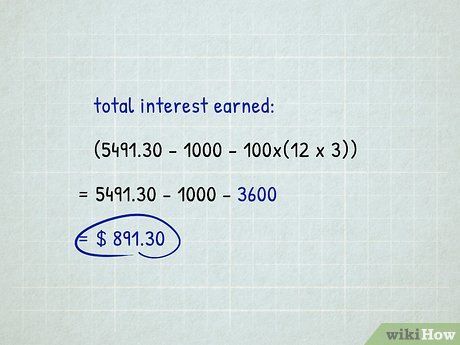

Proceed with the final calculations. Calculate the total profit earned.

Calculate the total profit earned.Use a spreadsheet to calculate compound interest.

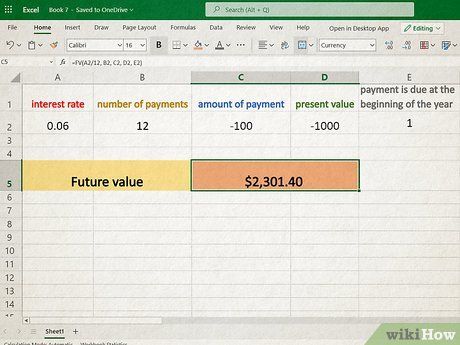

Create a new spreadsheet. Programs like Excel or similar spreadsheet tools (such as Google Sheets) save you time on calculations and even offer shortcuts in the form of pre-designed financial functions to assist in calculating compound interest.

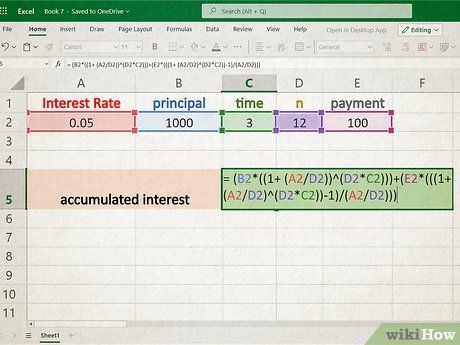

Label the variables. When using a spreadsheet, it's always helpful to keep everything organized and clear. Start by labeling the columns for the important data that will be used in your calculations (e.g., interest rate, principal, time, n, contributions).

Enter the variables into the spreadsheet. Now, fill in your account data into the next column. This way, the spreadsheet will not only be easier to read and interpret later, but it will also allow you to adjust one or more variables to explore different savings scenarios.

Create the equation.

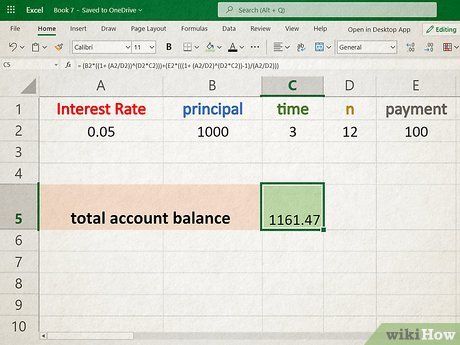

Create the equation. Use the financial function.and

Use the financial function.andAdvice

- In addition, compound interest calculations can become more complicated with variable contributions. In this case, you would need to calculate the interest for each individual contribution/payment separately (using the same formula mentioned earlier), and it is best to use a spreadsheet to simplify the process.

- You can also use online tools for calculating the annual percentage yield to determine the interest earned on your savings account. Search for "annual interest calculator" to find numerous websites offering this free service.