A bond is a debt instrument that pays a fixed interest rate until it matures. Upon maturity, the principal amount of the bond is returned to the bondholder. Many investors calculate the present value of bonds. The present value (the discounted value of future income streams) is one of the factors considered when investors decide whether to purchase an investment. The present value of a bond is based on two calculations: the present value of the interest payments and the present value of the principal amount to be repaid upon maturity.

Steps

Understanding the Basics of Bonds

Learn how bonds work and why they are issued. Bonds are debt instruments. Organizations issue bonds to raise capital for specific purposes. Governments issue bonds to fund public projects like roads or bridges. Companies issue bonds to raise funds for business expansion.

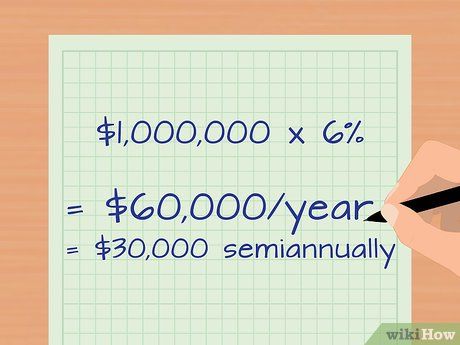

- All characteristics of a bond are outlined in the bond agreement. Bonds are usually issued in multiples of $1,000. For example, if IBM issues a $1,000,000 bond for 10 years at a 6% interest rate, the bond pays interest twice a year.

- $1,000,000 is the amount stated on the bond or the principal of the bond. This is the amount the issuer must repay when the bond matures.

- IBM (the issuer) must repay $1,000,000 to the investor after 10 years. The bond matures in 10 years.

- The bond has an interest rate of (1,000,000 USD multiplied by 6%), which is $60,000 per year. Since the bond pays interest twice a year, the issuer must make two payments of $30,000 each.

Consider how investors can profit from owning bonds. As shown in the example above, remember that dozens of investors can buy a portion of a $1,000,000 bond issued. Each investor will receive interest payments twice a year. The investor will also get their initial investment back (the principal or face value of the bond) when the bond matures.

- Many retirees often buy bonds because of the predictable income from interest payments.

- All bonds are rated based on the issuer's ability to pay interest and principal on time. Bonds with higher ratings are seen as safer investments due to collateral backing the bonds and/or the financial stability of the issuer.

- All else being equal, lower-rated bonds typically offer higher interest rates as these are considered riskier investments.

- For example, if both IBM and Acme Corporation issue bonds over 10 years, IBM, with a high credit rating, offers an interest rate of 6%. If Acme has a lower rating, it will need to offer a higher interest rate than 6% to attract investors.

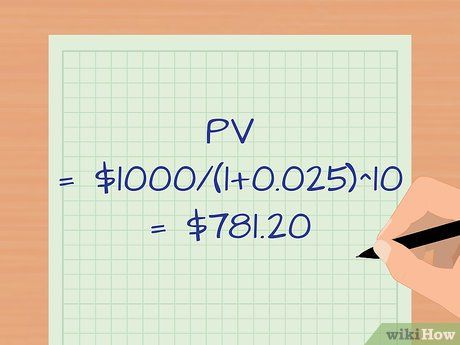

Review the present value. To calculate the bond's value at any given time, you should add the present value of the interest payments with the present value of the principal amount you will receive at maturity.

- The present value adjusts the future payment amounts to their current dollar value. For instance, if you will receive $100 in 5 years, to determine its worth today, you will calculate the present value of that $100.

- The amount is discounted at the yield rate. This discount rate is often referred to as the discount factor.

- An investor may choose a discount rate using several different methods. The discount rate could be your estimate of inflation over the bond’s remaining term. It could also be the minimum expected return rate based on the bond’s credit rating and the interest rate of similar-quality bonds.

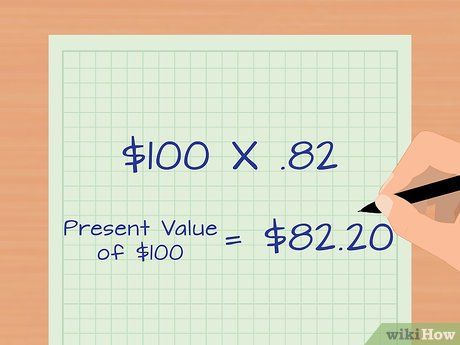

- Suppose you determine the discount rate to be 4% for the $100 payment in 5 years. The discount rate is used to reduce (discount) the future payment value to its current USD value. In this case, you're calculating the present value of a total amount of money.

- You can find present value tables online, or simply use an online present value calculator. If using a table, you’ll find the present value factor for a 4% discount rate over 5 years is 0.822. Therefore, the present value of $100 is ($100 x 0.822 = $82.20).

- The present value of a bond is the sum of (the present value of all the interest payments) + (the present value of the principal paid at maturity).

Use the present value formula

Apply the annuity concept to calculate the value of interest payments. An annuity is a specific amount of money paid to an investor over a set period. Your bond interest payments are considered a form of annuity.

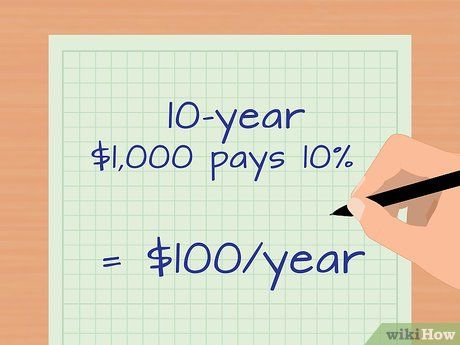

- To calculate the present value of interest payments, you need to calculate the value of a series of equal payments made each year on a cycle. For example, if you have a $1,000 bond with a 10-year term and a 10% interest rate, you’ll receive a fixed $100 per year for 10 years.

- The present value formula requires you to break the annual interest payments into smaller amounts that you will receive throughout the year. For example, if the $1,000 bond pays interest twice per year, you will have two payments of $50 each in your present value calculation.

- The earlier any payment is received, the more valuable it is. This concept is sometimes referred to as the 'time value of money' – $1 received today is worth more than $1 received tomorrow because you could invest (or simply spend) that $1 to earn a return. In this logic, receiving $50 in June and $50 in December is more valuable than receiving $100 in December, as you have the opportunity to use the $50 earlier.

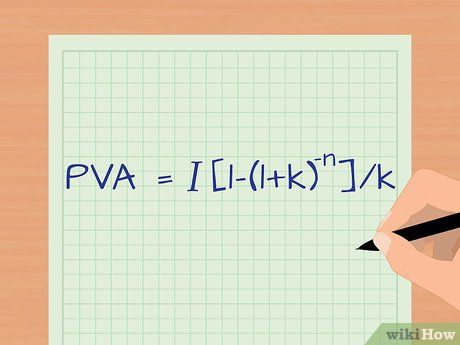

Apply the present value of annuity formula (PVA) to the interest payments.

Apply the present value of annuity formula (PVA) to the interest payments. Enter the variable values and compute the present value of the principal payments.

Enter the variable values and compute the present value of the principal payments.