Overhead costs refer to the expenses necessary to run a business, regardless of whether the company is handling a large number of orders or operating at a minimal pace. Properly managing these overhead costs allows businesses to offer better prices for their products or services and discover ways to reduce costs and streamline their business model. However, these benefits are only achievable if the accounting staff keeps detailed and accurate records. Read on to learn the best methods for calculating overhead costs.

Steps

Identifying Overhead Costs

It’s important to understand that overhead costs are expenses that are not directly tied to your product. These are also referred to as indirect costs. Indirect expenses such as rent, salaries for administrative staff, machine repair costs, and marketing costs are vital for business operations and must be incurred regularly.

- In our example, indirect expenses such as postage fees and insurance are necessary for the business to function but are not direct costs of producing the product.

- When calculating overhead costs, always consider whether the cost is fixed or variable. Fixed costs remain constant, while variable costs fluctuate depending on the company's activity level and production volume.

Direct costs are the expenses directly tied to the production of goods or services. These costs fluctuate based on customer demand for your product and the market prices of the input materials. For example, if you run a bakery, direct costs would include wages and ingredients. If you run a clinic, direct costs would include doctors' salaries, stethoscopes, and so on.

- The most common direct costs, as mentioned earlier, are wages and raw materials.

- Simply put, direct costs are paid for things that appear on the production line, while indirect costs are paid for the 'production line' itself.

Create a list of each type of cost by month, quarter, or year. You can choose the time period according to your preference, and usually, companies analyze costs on a monthly basis.

- Set a fixed period for consistency. If you calculate indirect costs monthly, you should also calculate direct costs monthly.

- Consider using programs like QuickBooks, Excel, or FreshBooks to help manage your data more effectively and efficiently.

- Don’t worry about where to place each cost just yet. It’s essential to get an overall cost picture before calculating your overhead costs.

Now, identify your overhead costs (indirect costs). Companies are required to pay for costs such as taxes, rent, insurance premiums, licensing fees, utilities, accounting and legal services, administrative staff salaries, equipment maintenance costs, etc. Search for all indirect costs.

- Review past cost reports and invoices to ensure no expense is overlooked.

- Don’t forget about recurring costs, like renewing licenses or submitting forms. Although these costs may appear infrequently, they are still considered overhead costs.

Use past costs or estimate them if you don’t know your exact expenses yet. If you’re a new entrepreneur or ambitious, you should conduct a thorough study of supply costs, labor, and other potential overhead costs.

- If you have past accounting data, you can use it for your budget for the coming year. The figures in your plan often remain the same from year to year, unless you make significant changes to your business plan.

- Take an average of the costs over 3 to 4 months to minimize the effect of any unusual costs.

Classify the costs on your list as direct and indirect based on your business model. Different industries will classify costs differently, and it’s up to you to decide how to categorize them. For example, legal fees are often considered overhead costs, but they are directly related to business operations if you run a law firm.

- If you’re still confused about the categorization, think of overhead costs as those expenses you’d have to pay even if you stopped production immediately. So, which costs would be considered overhead?

- Keep this list updated whenever you encounter new costs.

Sum all your indirect costs to calculate the total overhead costs. This is the amount you need to spend to keep your business running. In the example above, the initial overhead cost is $16,800. This figure is crucial when preparing a business plan.

Gain a deeper understanding of Overhead Costs

Next, calculate the percentage of overhead costs in relation to total costs. This percentage will show how much your company is spending to maintain operations versus how much is spent on producing a product. To do this, follow these steps:

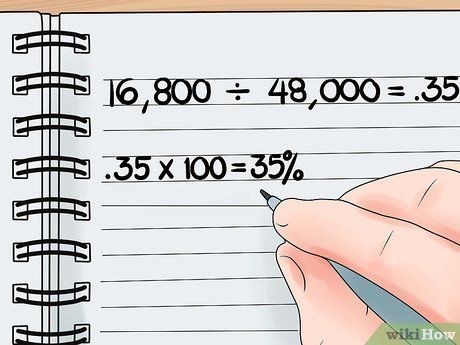

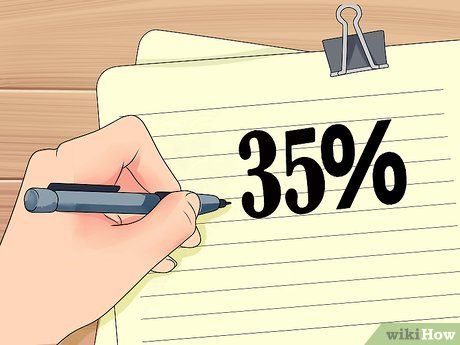

- First, divide the indirect costs by the direct costs. In this example, the overhead ratio is 0.35 (16,800 / 48,000 = 0.35).

- Next, multiply this number by 100 to get the percentage of overhead costs. In this case, the percentage is 35%.

- This means your company spends 35% of its total costs on overhead expenses like legal fees, administrative salaries, rent, etc., for each product produced.

- The lower the overhead costs, the higher the profit. Thus, a low overhead percentage is desirable.

Now, compare your company’s overhead costs with those of other companies. Here, the assumption is that companies pay similar direct costs, and the company with the lower overhead percentage will make more profit from selling products. By reducing overhead costs, your company can sell products at more competitive prices and/or achieve higher profit margins.

Leverage Overhead Costs to Improve Business Performance

Calculate the overhead costs in relation to labor costs to assess how effectively you are utilizing your resources. Multiply by 100 to find the percentage of overhead costs per employee.

- If this ratio is low, it indicates that your company is managing costs effectively.

- If it's high, your company may be employing too many staff members.

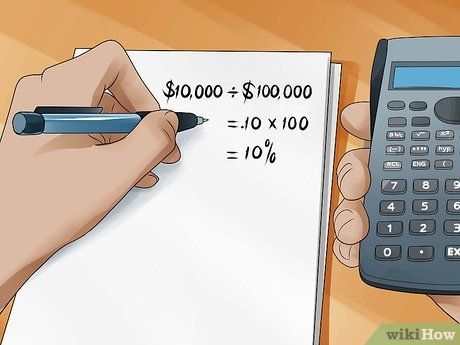

Calculate the percentage of revenue allocated to overhead costs. Divide the overhead costs by your revenue, then multiply by 100 to get the percentage. This is a simple way to check if you're selling enough goods/services to maintain business operations.

- For example, if my company sells $100,000 worth of soap every month and I pay $10,000 to cover overhead, this means I'm spending 10% of revenue on overhead costs.

- The higher this percentage, the lower the profit margin.

Look for ways to cut or better manage overhead costs if these ratios are high. High overhead is one of the main reasons you might not be making much profit. You could be paying too much in rent or need to sell more products to offset overhead costs. Maybe your staff is too large, and you’re not managing them effectively enough for maximum productivity. Use these numbers to analyze your business model further and make necessary changes.

- All industries and companies have overhead costs, but those who manage them effectively tend to generate higher profits.

- However, high overhead isn’t always negative. If you're investing in quality equipment or satisfying employees, you may achieve higher productivity and greater profits.

Advice

- If you're calculating past overhead costs, you can use existing data to perform the calculations. If you want to estimate future overhead, you'll need to use average figures. For example, to calculate future indirect costs, gather data from several past accounting periods to find the average indirect costs for each category that may arise in the future. Similarly, for direct costs, estimate the average cost based on current and past data. For instance, direct labor costs can be calculated by multiplying the average hourly wage by the average number of working hours over a period. The result may not be exact, but it will provide a close estimate.

- Continuously track the overhead cost ratio – monthly, quarterly, and annually – to mitigate the impact of fluctuations caused by cycles, buying psychology, and the availability/cost of raw materials.

Warning

- The steps outlined above are designed to assist you in better analyzing quantitative data. Each company has its own unique characteristics, so optimizing overhead costs is not an exact science.