Business-related expenses are typically divided into two categories: variable costs and fixed costs. Variable costs fluctuate based on production volume, while fixed costs remain constant. Understanding how to classify costs is the first step toward managing and improving business efficiency. Specifically, knowing how to calculate variable costs can help reduce expenses per production unit, ultimately increasing profitability for the business.

Steps

Calculating Variable Costs

Categorize costs as either fixed or variable. Fixed costs are expenses that do not change, regardless of production volume. Rent and administrative salaries are examples of fixed costs. Whether you produce 1 unit or 10,000 units, these costs remain the same each month. On the other hand, variable costs change with production volume. For instance, expenses for raw materials, packaging, shipping, and worker wages fall under variable costs. The more units produced, the higher these costs.

- Once you understand the difference between fixed and variable costs, begin categorizing your business expenses. Many costs, like those mentioned above, are straightforward to classify. However, some expenses can be ambiguous.

- Certain costs may be challenging to categorize, as they don't fit clearly into fixed or variable models. For example, an employee might receive a fixed salary plus a commission that varies with sales volume. These costs are split into separate fixed and variable components. In this case, only the employee's commission would be considered a variable cost.

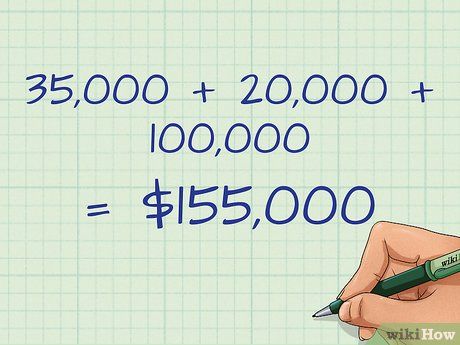

Sum up all variable costs over a specific period.

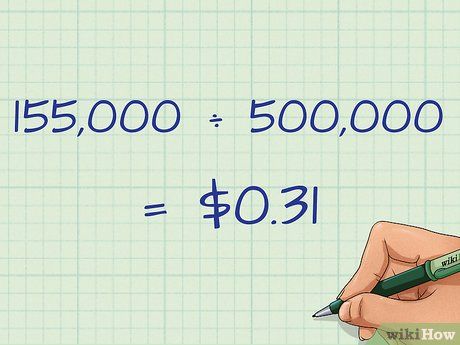

Sum up all variable costs over a specific period. Divide the total variable costs by the production volume.

Divide the total variable costs by the production volume.- The unit variable cost is simply the variable cost per production unit. It represents the expense incurred when producing one additional unit. For example, if the business produces an extra 100 units, they would incur an additional production cost of $31.

Use the high-low method

Understand mixed costs. Sometimes, it’s not straightforward to classify certain costs as purely variable or fixed. These costs may vary with production but are also necessary even when there is no production or revenue. Such costs are referred to as mixed costs. Mixed costs can still be broken down into fixed and variable components for accurate cost calculation.

- An example of a mixed cost is the salary of an employee who earns a base wage plus commission. The base wage is paid regardless of sales, but the commission depends on sales volume. In this case, the commission is the variable cost, and the base wage is the fixed cost.

- Mixed costs can also apply to hourly workers who are guaranteed a fixed number of hours per pay period. Regular hours are considered fixed costs, while any overtime hours are variable costs.

- Additionally, employee benefits can be recognized as mixed costs.

- A more complex example of mixed costs is utility expenses. Whether or not you produce, you still pay for electricity, water, and gas. However, utility usage may increase with higher production levels. Separating these costs into fixed and variable components requires a more sophisticated approach.

Calculate activity and costs. To separate mixed costs into fixed and variable components, you can use the "high-low method." This method starts by identifying the mixed costs from the highest and lowest production months and uses the difference to calculate the variable cost rate. First, determine which month had the highest production and which had the lowest. Record the measurable activity (such as machine hours) and the mixed cost you want to evaluate for each month.

- For example, imagine your company uses a water jet cutter for metal cutting, which is part of the production process. Water is required for this process, making it a variable cost that increases with production volume. However, water costs also arise from facility operations (e.g., drinking, sanitation, etc.). Thus, water costs are mixed costs.

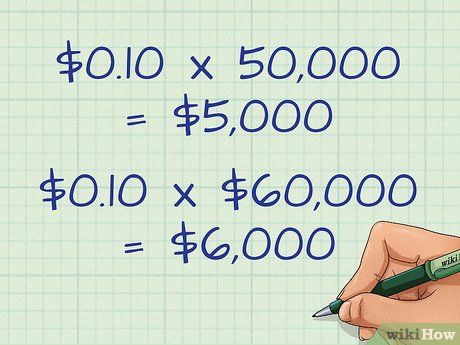

- In this example, the month with the highest water bill was $9,000 with 60,000 production hours, and the month with the lowest water bill was $8,000 with 50,000 production hours.

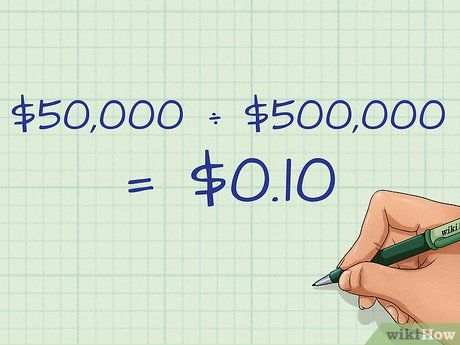

Calculate the variable cost rate.

Calculate the variable cost rate. Determine the variable cost.

Determine the variable cost.Use variable cost information

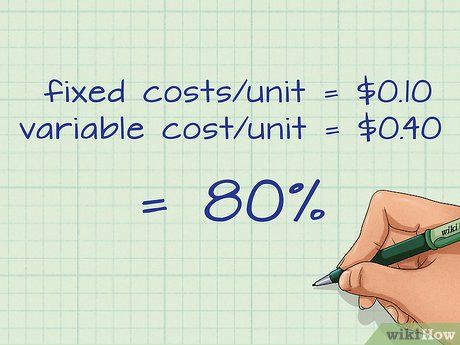

Analyze the trend of variable costs.

Analyze the trend of variable costs. Use the variable cost ratio to assess risk.

Use the variable cost ratio to assess risk.- If a company's production costs are primarily variable, it may have more stable per-unit costs. Consequently, profit margins are also more stable, assuming steady sales.

- This is true for large retailers like Walmart and Costco. Their fixed costs are relatively low compared to variable costs, which make up a significant portion of their per-unit revenue-related expenses.

- However, a company with a higher proportion of fixed costs may benefit more from economies of scale (larger production reduces per-unit costs) as revenue grows much faster than expenses.

- For example, a software company has fixed costs related to product development and support staff but can scale software sales without incurring significant variable costs.

- When revenue declines, a company relying mainly on variable costs can more easily scale back production while remaining profitable, whereas a company with high fixed costs must find ways to manage the significantly higher per-unit fixed costs.

- A company with high fixed costs and low variable costs also has production leverage, which amplifies profits or losses depending on revenue. Essentially, sales above a certain threshold yield higher profits, while sales below this level are much more costly.

- Ideally, a company should strive to balance risk and reward by adjusting fixed and variable costs.

Compare with other companies in the same industry. Calculate the variable cost per unit and total variable costs for a specific company. Then, find data on the average variable costs for that company's industry. This provides a benchmark for evaluation. Higher per-unit variable costs may indicate inefficiency, while lower per-unit variable costs can be a competitive advantage.

- Higher per-unit variable costs suggest the company uses more resources (labor, materials, utilities) or spends more on them compared to competitors. This could be due to inefficiency or higher-cost resources. In either case, the company is less profitable than competitors unless it can reduce costs or increase prices.

- On the other hand, a company that can produce the same goods at a lower cost gains a competitive edge by offering lower market prices.

- This cost advantage may stem from cheaper resources, lower labor costs, or greater production efficiency.

- For example, a company might purchase cotton at a lower price than its competitors, enabling it to produce shirts at a lower variable cost and sell them at a lower price.

- Public companies often disclose financial reports on their websites or through the Securities and Exchange Commission (SEC). Variable cost information can be found in their income statements.

Conduct a break-even analysis.

Conduct a break-even analysis.Tips

- Note: The method and sample calculation formula above can be applied to other currencies.