Working capital is a measure of the cash and current assets available to meet the daily operational needs of a company. Understanding this information will aid in business management and help make sound investment decisions. By calculating working capital, you can assess whether a company can meet its short-term obligations and how much time is required to do so. Without adequate working capital, the company's future could be uncertain. It also helps evaluate how efficiently a company is utilizing its resources. The formula for working capital is:

Working Capital = Current Assets - Current Liabilities

Steps

Perform a simple calculation

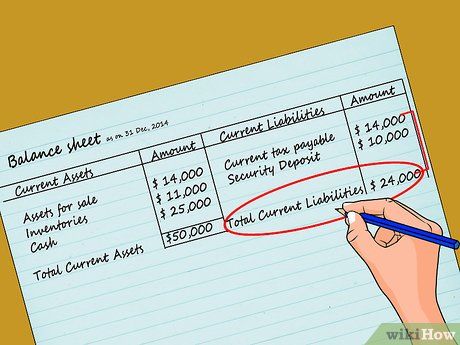

Calculate Current Assets. Current assets are assets that a business can convert to cash within one year. These include cash and other short-term accounts such as accounts receivable, prepaid expenses, and inventory.

- Typically, this information can be found on the company's balance sheet under total current assets.

- If the balance sheet doesn't include total current assets, check each line of the sheet. Add up all accounts that meet the definition of current assets to get the total. For example, you would sum "accounts receivable", "inventory", and "cash and cash equivalents".

Calculate Short-Term Liabilities. Short-term liabilities are those that must be paid within one year. These include accounts payable, accrued liabilities, and short-term loans.

- The balance sheet should show the total short-term liabilities. If not, you can use the information provided in the balance sheet to calculate this total by summing up the listed short-term liability accounts. For example, these may include "accounts payable and provisions", "taxes payable", and "short-term debt".

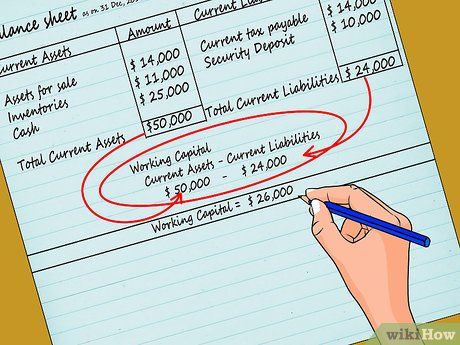

Calculate Working Capital. This is simply a basic subtraction. Subtract total short-term liabilities from total current assets.

- For example, if a company has current assets of 1 billion VND and short-term liabilities of 480 million VND, the working capital would be 620 million VND. With the current assets available, the company can pay off all its short-term debts and still have cash for other purposes. The company can use this cash for business operations or to pay off long-term debt. It can also be used to pay dividends to shareholders.

- If short-term liabilities exceed current assets, it indicates a shortfall in working capital. A working capital shortfall is a warning sign that the company might be at risk of default. In this case, the company may need to seek long-term financing. This could signal trouble for the company and might not make it an ideal investment choice.

- For example, suppose a company has 2 billion VND in current assets and 2.4 billion VND in short-term liabilities. The company’s working capital would be in deficit by 400 million VND (or -400 million VND). In other words, the company will not be able to meet its short-term obligations and will have to sell 400 million VND worth of long-term assets or seek other financing sources.

Understand and Manage Working Capital

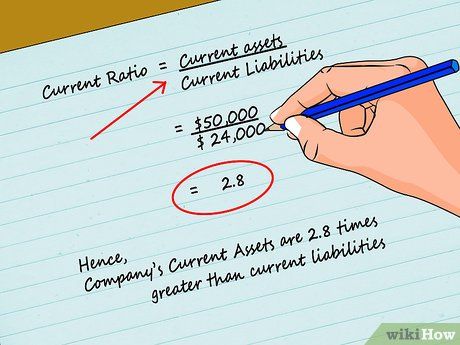

Calculate the Current Ratio. For a deeper analysis, many analysts use the "current ratio" – a metric that reflects the financial strength of a company. Using the same data from the first two steps, instead of measuring in monetary units, the current ratio gives a comparison ratio.

- A ratio compares two values and shows their relationship. Calculating the ratio is usually just a simple division problem.

- To calculate the current ratio, divide current assets by short-term liabilities. Current Ratio = Current Assets ÷ Short-Term Liabilities.

- Continuing with the example from section 1, the company's current ratio is 1,000,000,000 ÷ 480,000,000 = 2.08. This means the company has 2.08 times as many current assets as short-term liabilities.

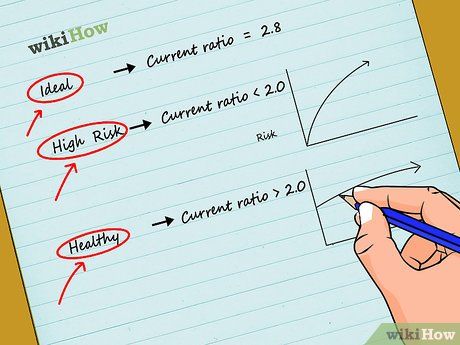

Understand the Significance of the Ratio. The current ratio is used to assess a company’s ability to meet its short-term obligations. In simple terms, it indicates how easily the company can pay its bills. The current ratio is useful when comparing companies or industries.

- An ideal current ratio is around 2.0. A ratio below 2.0 may indicate a higher risk of default. On the other hand, a ratio above 2.0 might suggest that management is overly conservative and not taking advantage of current opportunities.

- In the above example, the current ratio of 2.08 is considered a healthy indicator. It suggests that current assets could cover short-term liabilities for more than two years. Of course, this assumes that short-term liabilities remain at the current level.

- Different industries may have different accepted current ratios. Some industries require significant capital and may need to borrow funds to meet operational needs. For instance, manufacturing companies tend to have higher current ratios.

Manage Your Working Capital. Business managers must monitor every component to maintain an adequate level of working capital. This includes inventory, receivables, and payables. Management should assess the potential profitability and risks associated with having too little or too much working capital.

- For instance, a company with insufficient working capital risks being unable to pay its short-term liabilities. However, holding too much working capital may also be detrimental. A company with excess working capital may invest in long-term productivity improvements. For example, surplus working capital can be used for investments in manufacturing facilities or retail stores. Such investments can boost future revenue.

- If working capital is too high or too low, consider the following tips to help improve the current ratio.

Advice

- Manage credit accounts to avoid late payments from customers. If urgent collections are needed, consider offering early payment discounts.

- Pay off short-term debts when they are due.

- Avoid purchasing fixed assets (like a new factory or building) using short-term loans. Converting fixed assets into cash quickly enough to settle debt is challenging. This will affect your working capital.

- Manage inventory levels. Try to avoid stock shortages or overstocking. Many manufacturers use Just-In-Time (J.I.T.) inventory management because it is cost-effective. It also requires less space and reduces inventory damage and spoilage.