Lending money might be easy, but collecting it back can often be challenging. During these times, remember, asking for repayment is not a wrongdoing—the person who borrowed is the one who broke their promise. No matter the reason behind the borrowing, there is always a way to handle it when someone owes you money and refuses to pay. Sometimes, a simple reminder is enough. However, being prepared to take more assertive actions will help you achieve your goal and minimize unnecessary distractions.

Steps

Request Payment

Identify the point when you no longer trust the borrower to pay voluntarily. If a specific due date wasn’t mentioned in the original agreement, decide for yourself: based on your judgment, how likely is it that the person will pay without needing a reminder?

- Consider the loan amount. A small debt may not be worth pursuing immediately, while a larger one might take longer to collect.

- If someone owes money related to a business transaction, request payment as soon as possible. Waiting only makes the situation more difficult.

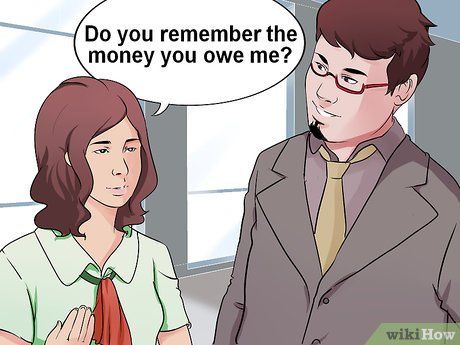

Politely inquire about the debt. Once the payment deadline has passed, kindly ask the borrower to settle the debt. At this stage, all you need is to make them aware that their loan is still unpaid. Often, people simply forget about the debt, and a gentle reminder is all it takes. Formally, this is referred to as a 'payment request.'

- Instead of demanding payment, consider reminding them ('Do you still remember the amount you owe me?') to maintain their dignity.

- Provide all relevant information when inquiring about the debt. Be prepared to mention the loan amount, the last payment date, the outstanding balance, any repayment agreements you are willing to accept, contact details, and a clear payment deadline.

- If dealing with a company or customer, sending an official letter can be helpful. It serves as written evidence in case the situation escalates.

- For the deadline, a typical period of 10 to 20 days from the request is reasonable: it’s not too long, but not so short as to alarm the borrower.

Consider accepting alternative forms of payment. Is it worth waiting? If the amount is small or you don't trust the borrower to pay, consider accepting something else in return—such as services or privileges—if you feel the arrangement is acceptable. In such cases, clarify the alternative offer and aim to finalize it as quickly as possible.

- Don’t rush into negotiations too quickly, as it might signal that the debt can be bargained down, or that the borrower could extend the time further.

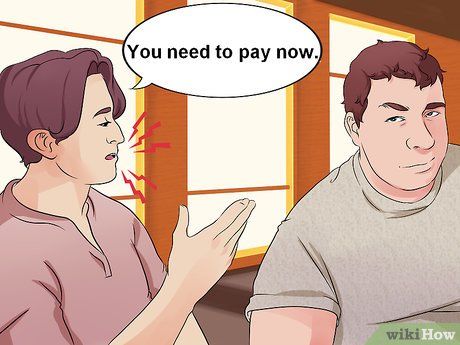

Be more assertive with the 'payment request.' If the borrower does not respond, you should become more direct. Make it clear that you expect immediate payment, define the payment obligation, and provide specific instructions on how to settle the debt.

- The language used should be more direct and convey urgency. Phrases like 'You need to pay now' or 'We need to reach an agreement on this immediately' will make it clear that you are serious and not open to negotiation.

- When making a request, outline the consequences of non-payment so the borrower understands your intentions and is prepared for their enforcement.

Become more aggressive in your debt collection efforts. If your request for payment yields no results, it’s likely that the borrower either lacks the funds or simply refuses to pay. Your task is to prioritize your payment, whether through phone calls, letters, emails, or face-to-face meetings, and ensure they pay you before anyone else (or before they disappear).

Consider using a collection agency. Taking this step demonstrates that you are serious and helps you avoid the hassle of directly contacting the borrower to arrange payments. A debt collection agency may charge a fee of up to 50% of the debt owed. Therefore, before deciding to use such services, you should weigh whether recovering part of the debt is better than recovering nothing.

- If the fees are too high, you might consider skipping this step and going straight to the relevant court.

Know your limits. When collecting a debt yourself, certain actions may be illegal depending on your location. In the United States, federal laws such as the Fair Debt Collection Practices Act may apply if you are considered a debt collector. It is also possible that you need to follow local laws. Although these laws may vary, it is generally best to avoid the following tactics:

- Calling at inappropriate times;

- Adding extra fees;

- Deliberately delaying payment to increase fees;

- Revealing debt information to their contacts;

- Lying about the amount owed;

- Making false threats.

Lawsuit

File a lawsuit in the local district court where the defendant resides or works. Research local laws or the court's website to understand how to file a claim. The statute of limitations for filing a claim is two years from when you first realize your legal rights have been violated. In the U.S., check out small claims courts, which handle cases with claims between $2,500 and $25,000, depending on the state. You can find court rules and websites via [this list] from the National Center for State Courts website.

- If you decide to file a lawsuit, be prepared for your court hearing. Gather all relevant documents, such as contracts, debt notes, and any evidence you can present, and make enough copies for the judge and the defendant or their representative.

- This can be a significant step. Ensure the debt is worth the trouble of going to court. If the borrower is a friend or family member, this action will likely harm your relationship.

Appeal to a higher court. If unsuccessful in the district court or if you are not permitted to file there, consider filing in a higher court. Seek advice or hire representation, complete the correct forms, and prepare for court with all the documents you can gather.

- Considering court fees and lawyer costs, this option is usually more expensive. However, if successful, it may prove to be a better option than using a collection agency.

- Threatening a lawsuit might be enough to prompt someone to pay. However, only make threats if you are serious about following through.

File a motion for a subpoena. Once you have won a judgment against the debtor, you can file for a subpoena if they refuse to pay, disregarding the court’s decision. Along with the subpoena, the court will schedule a hearing and require the defendant to explain why they haven’t paid.

- During the hearing, request the right to garnish the debtor's wages.

Receive payment

Collect the debt. After reminders, requests, and legal action, the debtor will be required to pay. Sometimes, simply asking for payment will be sufficient. At other times, you may need to involve legal enforcement, such as obtaining a court order or exercising a lien on collateral.

- If you have filed a lawsuit and hired a lawyer, you should seek their advice to determine the most appropriate course of action.

Identify the debtor's employer. Once the court grants wage control, it becomes your responsibility to locate the debtor’s employer. The easiest way is to directly ask the debtor. If they are unwilling to share, you may need to send an interrogatory – a set of questions that must be answered in writing under oath. Be sure to check your local court's website for the necessary forms.

Send to the debtor's employer. Once you have identified their current employer, you must send the interrogatories to confirm that the debtor is indeed employed there and that their wages have not been garnished to the maximum allowable limit.

Request a wage garnishment order. Once confirmation is obtained, you may request the court to issue a garnishment order, which will be sent to the debtor's employer, and their wages will be redirected to you.

- Keep in mind that different jurisdictions have varying wage garnishment laws, so ensure you are familiar with the laws in your area.

Advice

- Don’t feel guilty about reclaiming what’s rightfully yours. You haven’t broken any promises. The borrower did, and you have every right to ask for it back.

- Remember to stay calm and avoid becoming frustrated. The debtor should be the one feeling upset for not fulfilling their obligation to repay. Be firm but polite. It will increase your chances of success.

- If payment is a persistent problem with an individual or business, exercise caution when dealing with them in the future.

- Keep records of all documentation during the collection process, especially if you need to take the matter to court. For business transactions, retain legal records whenever possible.

- This article outlines the debt recovery process for informational purposes. Keep in mind that the paperwork required can vary significantly, and procedures may not be consistent. Be sure to research thoroughly before filing a claim or hiring a lawyer.

- If you run a small business or are a freelancer, you may need a different approach when dealing with clients who refuse to pay.

Warning

- If you are in the United States and dealing with business debt, ensure you are familiar with the Fair Debt Collection Practices Act (https://www.ftc.gov/enforcement/rules/rulemaking-regulatory-reform-proceedings/fair-debt-collection-practices-act-text) and any other applicable laws. Otherwise, you could end up being the one at fault.

- Be careful about disclosing to anyone that the debtor hasn’t paid you, as you might be accused of defamation or slander, depending on the situation.

- If the debtor files for bankruptcy, you must immediately halt any collection efforts to avoid violating bankruptcy laws and government debt collection regulations.