Whether you're managing a tight budget or enjoying a comfortable lifestyle, sticking to a financial plan can significantly improve your money management skills. By doing so, you gain a clearer insight into your spending patterns and identify areas where you can cut back. While budgeting might not always be exciting, the financial freedom it brings is well worth the effort of reviewing your spending habits and creating a realistic plan to manage your finances!

Steps

Budgeting

Create a preliminary budget by subtracting expenses from income. To start budgeting, add up all your monthly income. Next, calculate your average monthly expenses and any other expenditures. Finally, subtract your expenses from your income to see if your spending exceeds your earnings.

- Your income may include earnings from work, family contributions, or financial aid and support payments you receive.

- Your expenses will cover bills like rent or mortgage and insurance, as well as costs for food, clothing, education, and entertainment. Some expenses are fixed monthly (like rent), while others need to be averaged (like food).

- Try using this budgeting worksheet to create a preliminary budget: https://www.consumer.gov/content/make-budget-worksheet

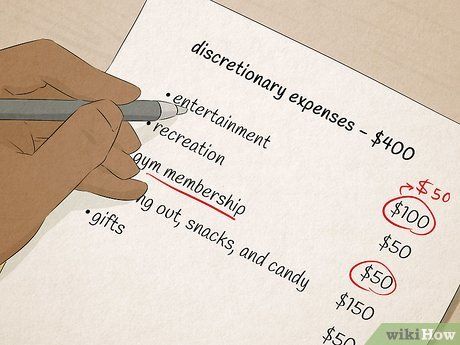

Set spending limits based on your preliminary budget. Once you have a general idea of where your money is going, review your spending habits. If there are areas where you're overspending, try gradually cutting back to give your budget a little more breathing room.

- Break down your expenses into categories to see what you're spending on. For example, you can list costs like rent, phone bills, and utilities under "Utilities." Expenses like groceries and dining out can go under "Food," and items like clothing and school supplies for kids can be listed under "Children."

- Unless you need to make drastic cuts, start with small, achievable goals to save money. For instance, if you're spending too much on streaming services, begin by canceling the least-used subscription instead of cutting them all at once.

- When budgeting, prioritize what matters most to you. For example, while you might not dine out or go to bars every night, if you can't live without these activities, consider cutting back elsewhere, such as canceling your cable TV package.

Track your spending to ensure you stay within limits. Setting limits isn't enough; you also need to monitor your actual spending to avoid exceeding them. The best way to do this depends on what works for you—you might find it easier to jot down each purchase as you make it or review your bank and credit card statements at the end of the month to see where your money went.

- One benefit of recording every purchase is that it helps you remember exactly what you bought, though many find this tedious.

- It's crucial to know where your money is going to avoid accidentally overspending.

Allocate a portion of your budget for discretionary spending. Sticking to a budget can feel restrictive if it doesn't allow for any enjoyment. If possible, set aside a small amount each month for things you love, like a night out with friends or new materials for your hobbies.

- Living on a budget can actually free up money for discretionary spending by reducing impulsive purchases on unnecessary items.

- Be realistic—if you can't find room for discretionary spending in your budget, it's okay to skip it.

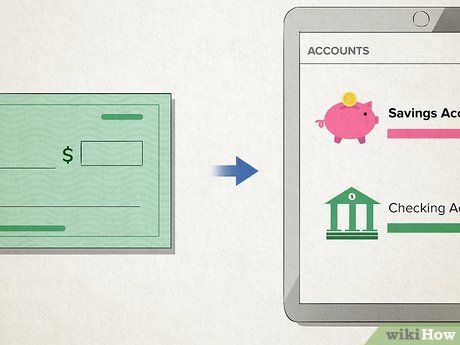

Set aside a portion of each paycheck for savings. Saving can seem challenging when you're sticking to a budget, but having a small emergency fund for unexpected expenses can be a lifesaver. Every time you receive a payment, set aside a little to transfer into your savings account. Even if it seems insignificant, it will add up over time!

- Start with a realistic goal, like saving 200,000 – 400,000 each week for a few months. Once you're comfortable, challenge yourself to increase your savings if possible.

- Even saving 100,000 - 200,000 a month is better than saving nothing.

- Ultimately, aim to save enough to cover 3-6 months of expenses in case you're unable to work.

Try the envelope method to manage cash spending. If you primarily use cash for expenses, it can be hard to track where your money goes. One way to manage cash is to divide it into different envelopes. Label each envelope with a spending category and only use the money inside for that purpose.

- For example, you might label envelopes as "Food," "Clothing," "Healthcare," and "Dining Out." If you plan to have lunch with friends, grab the "Dining Out" envelope.

- Avoid borrowing from other envelopes if you overspend, or you might fall short in other categories by the end of the month.

Schedule your bills to ensure timely payments. Purchase a calendar, planner, or download an app to track each monthly bill and its due date. This way, you won’t accidentally miss a payment and incur late fees or penalties.

- Late payments can also harm your budget in the long run. They can lower your credit score, meaning you’ll pay higher interest rates on loans like car loans or mortgages, which increases your monthly payments.

Maintain Discipline

Learn to say no and resist temptation. In today’s world, opportunities to spend money seem endless. To stick to your budget, you’ll need willpower and discipline. This isn’t always easy, but keep your goals in mind whenever you feel the urge to buy something unnecessary. Additionally, practice occasionally saying no when friends invite you out, especially if you tend to overspend during social outings.

- Avoid places that tempt you to overspend, especially at first. If you’re an online shopper, unsubscribe from promotional emails to avoid feeling like you’re missing out.

- When going out, bring cash and only spend what you can afford.

- Try repeating a “mantra” when tempted to spend. For example, if you’re saving for a vacation, your mantra could be “Beach getaway!”

Automate transfers to your savings account. Each week, transfer a set amount from your paycheck directly into your savings account. You’ll find it much easier to save if the money is out of sight from the start.

- This method can also apply to retirement and healthcare accounts, if applicable.

- If you’re paid in cash, make it a habit to set aside savings immediately after receiving your payment—preferably before spending on anything else.

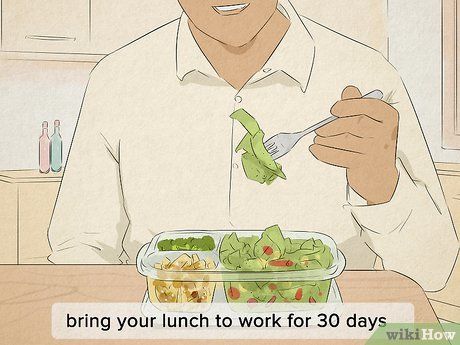

Set personal challenges for yourself. If you want to manage your money even better, try challenging yourself, such as bringing lunch to work for 30 days or avoiding new clothes for 3 months. Sometimes, you just need an extra push to change your habits.

- Share your challenge with a friend to hold yourself accountable!

Avoid using credit cards unless you can pay off the balance. When you buy something with a credit card, you typically won’t incur interest if you pay the full amount each month. However, if you only make the minimum payment, you’ll continue to accrue interest monthly until the balance is paid off.

- Credit cards can lead to overspending because they create the illusion of free money. If you struggle to control your spending, it’s best to avoid using credit cards altogether.

Keep going, even if you’ve strayed from your plan. While responsible spending is important, don’t be too hard on yourself if you occasionally splurge. Even if you’ve made significant mistakes, focus on the future and take small steps toward your financial goals.

- Remember, forming new habits takes time, so don’t get discouraged if progress is slow. Sometimes, it’s a sign that your budget needs adjusting rather than your spending habits. Continuously evaluate and tweak your financial plan each month.

Find Ways to Save Money

Compare prices before making purchases. The internet makes it easier than ever to check prices across multiple stores, ensuring you always get the best deal. You can compare prices for everything from groceries and school supplies to phone plans and car loans, so take advantage of available resources to avoid overspending.

- Try using websites like Google Shopping, Shopzilla, and Bizrate to compare prices from different retailers.

- Also, compare different products and weigh their pros and cons to ensure you’re getting the best value for your money.

Cook at home regularly. Even if you don’t think you eat out often, you might be spending more than you realize on things like fast food and snacks from convenience stores. To avoid this, plan your meals ahead of time and visit the grocery store weekly to buy all the ingredients you need.

- Take advantage of coupons to save even more. Additionally, consider using one ingredient across multiple meals.

- If you find a good deal on meat or other products, buy in bulk and freeze for later use.

- Turn inexpensive ingredients into delicious meals! For example, you can elevate instant ramen by adding a fried egg and chopped green onions.

Purchase second-hand and clearance items whenever possible. You can save a significant amount of money by opting for used items instead of new ones. Check out thrift stores and consignment shops for items you need. You might also find great deals by shopping for off-season clothing in the clearance sections of your favorite stores.

- Look for “free shipping” offers when shopping online or use membership coupons that include free shipping.

- Don’t forget to browse resale and auction websites! However, be cautious when meeting sellers in person—it’s best to bring someone you know and leave immediately if something feels off.

Cancel your cable subscription if you primarily use streaming services. If most of your viewing time is spent on platforms like Netflix, Prime Video, or Hulu, you might find that you don’t need cable at all. Cutting the cord is an increasingly popular way to save extra money each month.

- On the other hand, bundling services like internet, cable, and phone might offer better value. In this case, consider canceling streaming services you rarely use.