Switzerland is globally recognized for its banking system, which boasts exceptional privacy policies. In Switzerland, it is a criminal act for bank employees to disclose clients' private information. In the past, this system was exploited by individuals seeking to hide illegally obtained money or valuables. However, current concerns over terrorism and smuggling have led Swiss authorities to deny services to clients suspected of illegal activities. Some Swiss banks now refuse to serve American clients due to extensive investigations by the U.S. Department of Justice. Although Swiss banks may not be as glamorous as portrayed in spy or action movies, they operate efficiently and securely. Each bank has its own account opening process, but understanding general information and required documents can make opening a bank account in Switzerland easier.

Steps

Choose a Bank and Service

- Citizens of certain countries are prohibited from opening accounts in Swiss banks. This can be due to various reasons, such as sanctions (for countries like Russia and Iraq) and other political exceptions.

- Regardless of your nationality or income source, your application may be rejected if you are considered a 'politically exposed person'—someone involved in scandals or with a notorious reputation. Banks fear that such individuals could pose a significant risk to their reputation.

- If privacy is a priority, consider choosing a bank without branches in your home country. Most banks are regulated by the laws of the countries where they operate, not necessarily where their headquarters are located.

- Note that if a bank is not classified as a 'Qualified Intermediary' (QI), it must report account holders and any funds received from the U.S. to the IRS if the account holder is a U.S. citizen.

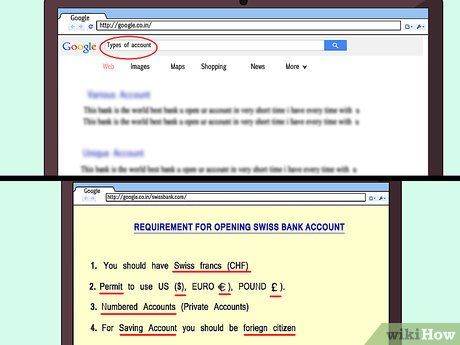

- Some banks require clients to use Swiss francs (CHF), while others allow transactions in USD, EUR, or other global currencies. Check with your chosen bank to confirm accepted currencies if you’re concerned about currency conversion.

- One of the most secure account types is the 'numbered account.' These accounts are not 'secret' or 'anonymous.' Senior bank staff will know the account holder’s identity, but the accounts offer a high level of privacy, as banks use only the account number in transactions. However, these accounts come with restrictions and may incur annual fees of up to 2,000 Swiss francs.

- Be aware that some Swiss banks may be reluctant to offer savings accounts to foreign nationals. Instead, they focus on providing investment opportunities and wealth management products.

Open an Investment Account

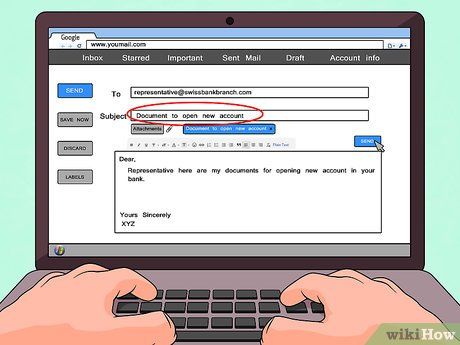

- Some banks may allow you to complete the process via mail. A certified copy of your government-issued passport must be authenticated by an authorized body and sent to the bank where you wish to open the account.

- Clients may need to provide a valid passport for identification.

- The bank representative may request documents to verify income sources. For example, they might ask for a copy of a contract proving the sale of a property, stock transaction receipts, or certified bank statements from previous transactions.

- Banks may verify a client’s address by sending a letter to that location.

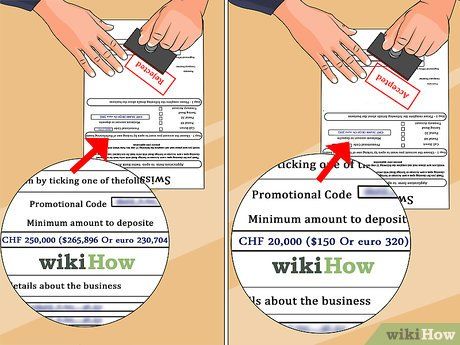

- Many private banks will not serve clients who cannot invest at least 250,000 CHF (approximately 265,896.64 USD, 230,704.37 EUR, or 5,599,724,116 VND). However, other banks, including UBS and Credit Suisse, may accept investments below 50,000 CHF (approximately 53,179.33 USD, 46,140.87 EUR, or 1,119,944,823 VND). Check with your preferred bank to learn about their minimum requirements.

Open a Personal Account

- Clients living outside Switzerland who wish to open a Swiss bank account but cannot visit a branch in person may request account opening documents by mail. The provided documents must be authenticated by a notary office, a Swiss bank employee, or an employee of a partner bank that the Swiss bank collaborates with.

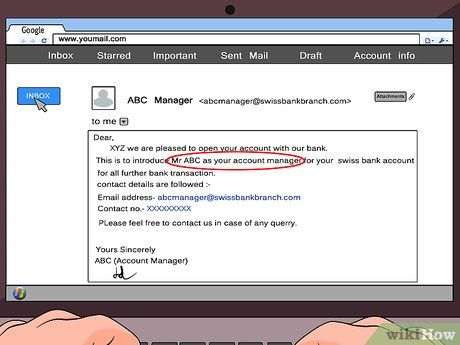

- Branches in major cities often have at least one account manager who speaks a foreign language, including English. Otherwise, they will be fluent in one of Switzerland’s four main languages: German, French, Italian, or Romansh. If you need someone who speaks a language other than these four, call ahead to arrange it.

- New clients will be asked to confirm their identity and residential address. If your ID card does not show your Swiss address, you may need to provide a copy of your rental agreement.

- Some banks may require proof of employment. Clients might need to present employment contracts and personal income tax returns to complete the verification process. Demonstrating proof of employment assures banks that the funds you deposit are not derived from illegal activities.

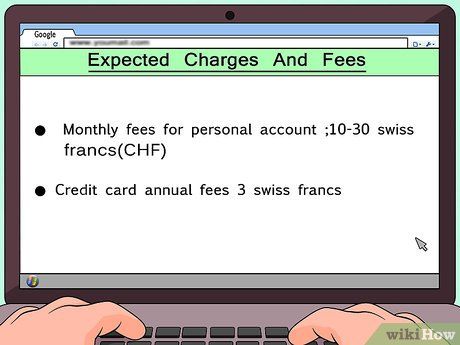

- Monthly fees for personal accounts typically range from 10 to 30 CHF, though clients may receive discounts or waivers by switching to electronic statements, having a mortgage with the bank, or maintaining a large account balance.

- Credit cards and Carte Maestro cards often have annual fees of up to 3 CHF.

Using Funds in Your Swiss Bank Account

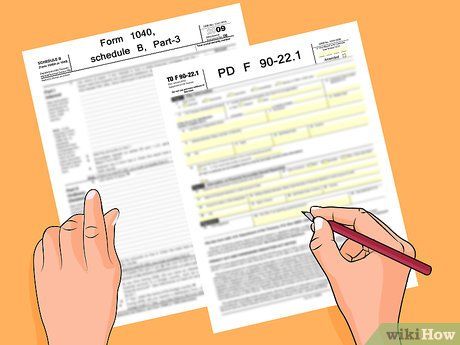

- File Form 1040, Schedule B, Part III, disclosing the opening of a foreign bank account.

- Submit Form TD F 90-22.1 by June 30 each year to notify the IRS of any foreign accounts exceeding $10,000 at any point in the previous year.

- Investors with private Swiss bank accounts who prioritize security may avoid using debit cards or checkbooks. Writing checks or using debit cards leaves a clear trail to your bank account. If maintaining account secrecy is crucial, issuing debit cards or checkbooks increases the risk of exposure.

Tips

- To view a list of Swiss banks, visit http://www.swconsult.ch/cgi-bin/banklist2.pl