Generally, calculating proportional wages for employees is quite simple; typically, you only need to determine the proportion of the regular pay period that the employee has worked and pay the appropriate amount. Both daily payment and percentage-based payment methods comply with U.S. federal laws. The results will be the same if the employee receives weekly wages and usually very close if the employee is paid monthly.

Steps

Daily Payment Method

Determine the pre-tax annual salary. Start with the employee's official annual salary. Do not include taxes at this stage; they will be deducted at the end of this section.

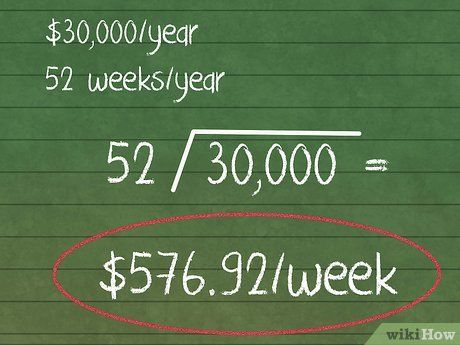

Divide the annual salary by the number of working weeks in a year. This is the amount the employee earns in one week. Use the pre-tax annual salary and deductions.

- For employees working the entire year, the working period is 52 weeks.

- For example, an employee earning $30,000 annually; their weekly income would be $30,000 ÷ 52 = $576.92.

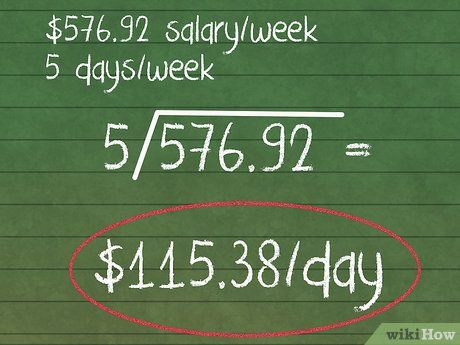

Divide the weekly salary by the number of working days in a week. This is the daily wage, or the amount the employee earns each day.

- Continuing the example above, an employee with a weekly salary of $576.92 working 5 days a week. Their daily wage is $576.92 ÷ 5 = $115.38.

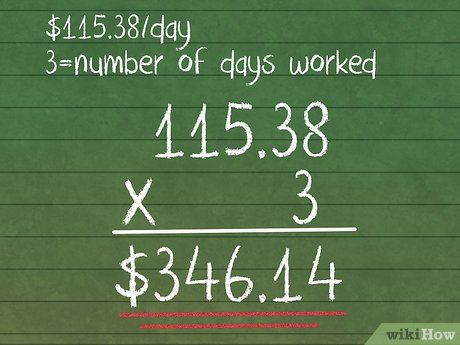

Multiply the result by the number of working days. Calculate the number of days the employee worked during the pay period you are prorating. Multiply this by the daily wage calculated earlier.

- In our example, if the employee worked 3 days during the prorated period, their earnings would be $115.38 x 3 = $346.14.

Deduct standard taxes. Remember that prorated wage payments are treated as regular taxable income. This means you need to subtract the applicable tax percentage, just like a regular paycheck. If the employee has a retirement account or other special deductions, these should also be accounted for.

- If you are in the U.S., refer to our article on federal tax deductions for more information. Additional state taxes may also apply.

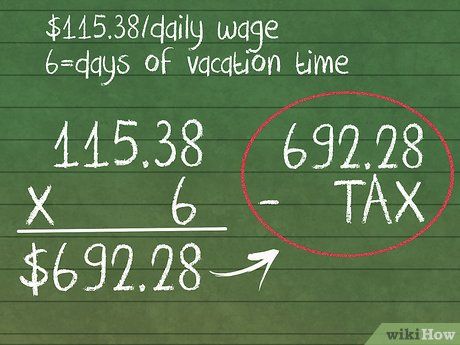

Compensate former employees for unused leave. If an employee leaves the company due to vacation or sick leave, the employer must still pay them for this period as required by law. Use the same method to calculate the daily amount owed.

- If the employee in the example above has 6 days of unused leave, they should be paid an additional $115.38 (daily wage) per day, totaling $115.38 x 6 = $692.28.

- Deduct taxes from this amount.

Percentage-Based Payment Calculation Method

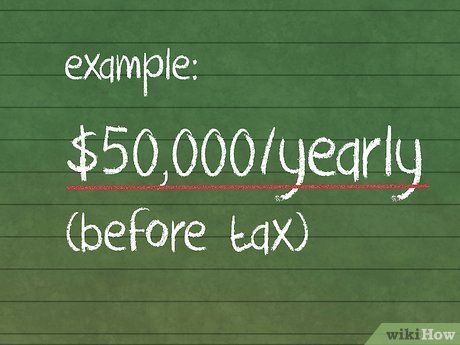

Write down the employee's pre-tax annual salary. This is the first step in determining how much the employee earns during their working period. Use the official salary, not the amount received after taxes.

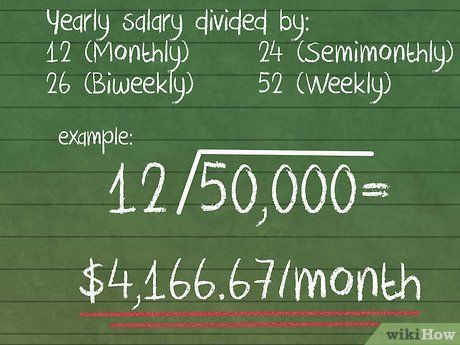

Determine the earnings per pay period. This is the amount the employee receives each pay period. If you don’t have this information readily available, calculate it based on the employee’s typical earnings:

- Monthly salary → divide the annual salary by 12.

- Twice a month → divide by 24.

- Every two weeks → divide by 26.

- Weekly → divide by 52.

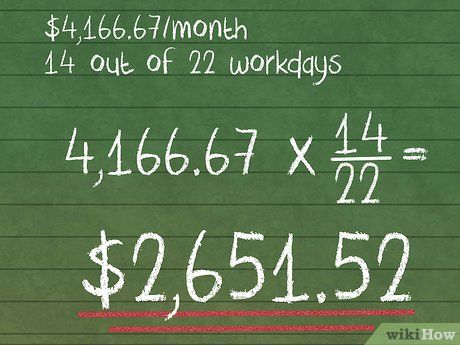

- For example, an employee earning $50,000 annually with monthly pay would receive $50,000 ÷ 12 = $4,166.67.

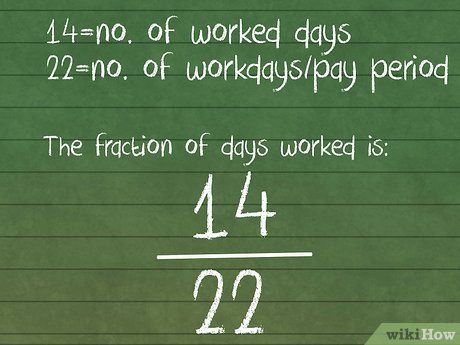

Calculate the ratio of days worked during the pay period. Look at the specific pay period in question and compute as follows:

- Note the number of days the employee worked (for the salary you are calculating).

- Divide by the total working days in that pay period. Calculate carefully. Do not assume every pay period has the same number of working days.

- For example, an employee worked only 14 days in September instead of the usual 22 days. Their working day ratio would be 14/22.

Multiply this ratio by the pay per period. This calculation will give you the exact amount you need to pay the employee.

- For example, an employee earning $4,166.67 monthly but working only 14 days instead of 22 in September would receive $4,166.67 x 14/22 = $2,651.52.

Tax Deductions. Calculate any income tax withholdings, pension fund deductions, and other specific deductions typically applied to the employee.

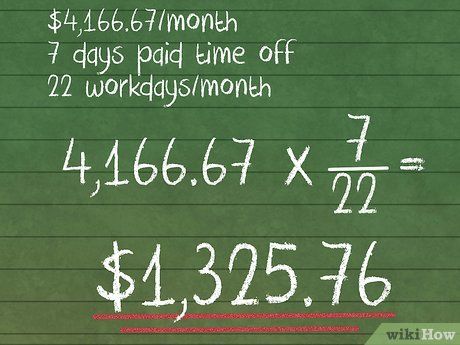

Compensating Employees for Sick Leave and Vacation Time. In such cases, employers are often required to pay out any unused leave as mandated by law. Employees should receive their regular wages for this period, calculated using the same method and rate as usual.

- For example, if the employee in the above scenario has 7 days of accrued paid leave, they would receive an additional amount of 4,166.67 x 7/22 = 1,325.76 dollars.

- This compensation is also subject to the same tax deductions as regular wages.

Advice

- For hourly employees, the above method is unnecessary. Simply multiply the hourly wage by the number of hours worked during the pay period. Hourly wages are also subject to standard tax deductions.

- Overtime pay is calculated similarly, using the same proportional rate as regular wages.

- Remember that many states have their own wage/income tax regulations in addition to federal laws. When calculating proportional wages, ensure these deductions are accounted for to determine the final payment to the employee.

Warning

- In the U.S., a salaried employee can only be paid on a proportional basis under specific conditions, most commonly when their employment starts or ends mid-pay period. Employers cannot reduce their wages due to reduced working hours.

- Employers may face legal consequences for choosing a method that results in lower payments for employees. It is best to apply a consistent method for all proportionally paid employees.