When unpaid bills pile up in your mailbox, it's essential to address the situation as quickly as possible. If you're facing financial challenges, you must learn to organize, pay on time, and prioritize your bills effectively.

Steps

Track Your Bills

Open bills immediately. When you receive payment notices, open them right away. Delaying increases the likelihood of ignoring incoming bills. Avoiding bills does no good for your financial health.

- Even those who receive electronic bills tend to delay opening them. Many people avoid viewing bills if they don't appear physically. If this sounds like you, consider switching from electronic to paper bills.

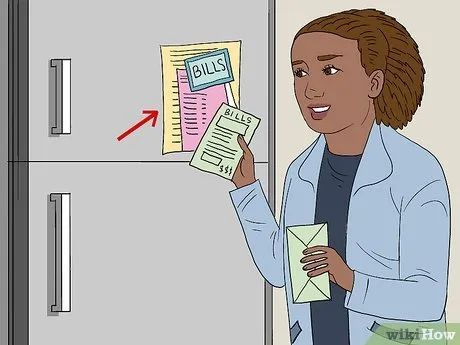

Organize bills in one place. This might sound unusual, but not everyone does it. Even those who know they should sometimes fail to follow through. Gather all your bills in a single location, moving them from your mailbox to this spot. This could be your desk, refrigerator door, or living room table—anywhere you’ll see them daily and can’t ignore them.

Pay bills as soon as you receive them. The easiest way to stay on top of your bills is to pay them immediately upon receipt. This eliminates worries about late payments or overspending on unnecessary items. The money you allocate will already be spent on essential expenses.

Categorize bills into two groups. Even when trying to pay all your bills, some may remain unpaid temporarily. Sort your bills into two categories: those due at the beginning of the month and those due mid-month. Prioritize paying the early-month bills first, followed by the mid-month ones.

Negotiate extended payment deadlines. Ideally, the number of early-month bills should match the mid-month ones. Most companies will adjust payment dates upon request. If one category has more bills than the other, contact the company’s customer service to request a date change.

Mark your calendar. To avoid missing payments, mark two dates on your calendar for bill payments. These dates should be earlier than the actual due dates. For example, on the 1st and 15th of each month, set aside an hour to review and settle your bills. Stay committed to these dates.

Use bill payment reminder apps or websites. If you need a tool for reminders instead of a calendar, you can install an app or visit a bill payment website. Popular features include automatic linking of debit and credit cards, reminders for overdue bills, and alerts for low bank account balances. Many useful apps and websites are available, such as Mint Bills, Prism Bills and Money, and Evolve Money.

Sign up for online bill payments. Automatic online bill payments consolidate all your bills into one account. You won’t need to worry about organizing bills or remembering to write and mail checks. You can set up online payments through a website, an available online app, or automate payments directly with the bill issuer.

Calculate bill payment amounts

Create a separate account for bill payments and personal expenses. This is one of the simplest budgeting methods you should adopt. Calculate your total monthly bill payments. Divide this amount by your monthly salary to determine how much to allocate for bills each payday. When you receive your salary, set aside the bill payment amount in a dedicated account.

Budget for irregular expenses. Some costs, like vehicle registration, taxes, and insurance, are paid once or twice a year instead of monthly. You need to plan for these expenses. Write down the total amount of irregular bills and divide it into 12 parts to determine how much to save monthly.

- To avoid overlooking irregular expenses, deposit the amount into your general bill payment account monthly. The funds will be there when needed.

- Budget for non-monthly purchases like clothing to use when you need to buy new items.

Set up an emergency savings account. This is crucial, and many financial experts recommend saving three to six months' worth of income for emergencies. After paying your bills, prioritize building this fund. The amount you save depends on your needs. For example, if your car insurance deductible is 5 million, aim to save at least 5 million in your emergency fund in case of an accident.

Paying bills during financial difficulties

Prioritize the most critical bills. This may sound simple, but to execute it, divide your bills into three categories: essential, secured debt, and unsecured debt.

- Essential bills are those necessary for daily living, such as rent or mortgage, utilities, groceries, and expenses that enable you to work, like childcare or car maintenance.

- Secured debt involves collateral. If you fail to pay, the creditor can claim the asset without going to court. This includes mortgage payments, car loans (also essential), child support (using income as collateral), and unpaid taxes. After covering essential expenses, address these debts.

- Finally, pay unsecured debts. Creditors must sue to seize assets for unsecured debts, which takes time. If you fall behind, you have more room to negotiate compared to secured debts and essential expenses.

- For large, irregular bills, consider spreading payments over several months if you can't pay in full. Negotiate installment plans with creditors. The key is to make an effort to pay rather than doing nothing.

Cut unnecessary expenses. This isn't easy, but if you're running a monthly deficit, you need to reduce spending. Consider canceling cable TV or downgrading your smartphone to a landline, or selling items until you regain financial control.

Communicate with creditors as soon as possible. Many lenders or utility companies will work with you to lower your bills if you're facing financial hardship.

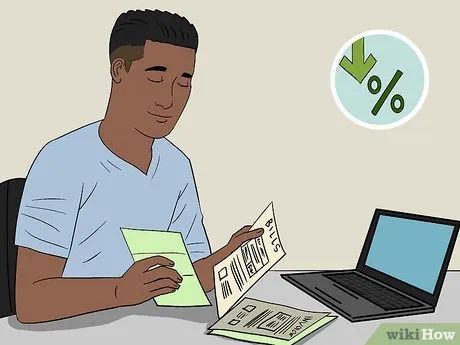

Explore ways to reduce insurance costs. For instance, you can opt for a higher car insurance deductible or switch to a more affordable insurance plan that aligns with your financial situation.

Seek financial counseling. Reach out to a nonprofit credit counseling or financial planning organization. Counselors can help you create a budget and negotiate with creditors on your behalf. Be cautious of fraudulent financial counseling services and choose reputable advisors. Verify if the organization is nonprofit, inquire about the counselor's qualifications, fees, terms, conditions, and payment methods.

Tips

- When paying bills online, create a password-protected record containing all website addresses, usernames, and passwords. Avoid using the same password for all sites.

- Set up direct savings from your paycheck. The savings will be automatically transferred to your bank account, saving time and reducing the temptation to spend cash when depositing manually.