The term "pay yourself first" has gained significant popularity in the world of personal finance and investing. Rather than paying all your bills and expenses first and saving what’s left, the idea is to reverse the process. Set aside funds for investments, retirement, college savings, future down payments, or any long-term goals before addressing other expenses.

Steps

Identify Your Current Expenses

Determine Your Monthly Income. Before paying yourself first, you need to know how much you need to allocate. Start by reviewing your current monthly income. To do this, simply add up all your sources of income for the month.

- Note that this should be your "net" income or the amount you take home after taxes and deductions.

- If your income fluctuates from month to month, use the average income over the past six months or a slightly lower figure. It's often safer to use a lower figure as it can lead to more accurate projections, preventing potential shortfalls.

Identify Your Monthly Expenses. The easiest way to determine your monthly expenses is by reviewing your bank statements from recent months. Simply add up all bill payments, cash withdrawals, and transfers. Don’t forget to include any cash income you’ve spent.

- There are two primary types of expenses to keep in mind: fixed costs and variable costs. Fixed costs remain constant each month and typically include rent, utilities, phone/internet bills, debt repayments, and insurance. Variable costs fluctuate from month to month and can include expenses like groceries, entertainment, fuel, or miscellaneous purchases.

- If tracking your spending seems like a difficult task, you might consider using software like Mint (or many similar apps). With Mint, you can sync your bank account, and the software will track your expenses by category. It offers a clear, organized view of your spending habits, keeping you updated regularly.

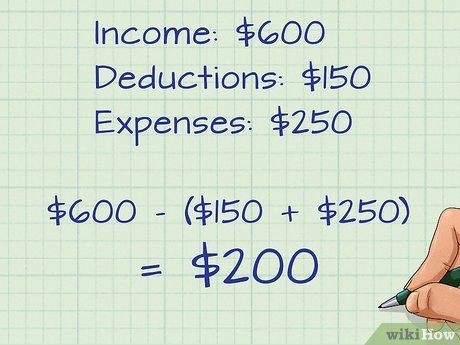

Subtract Expenses from Income. This way, you can determine how much you’ll have left at the end of the month. This step is crucial because it helps you figure out how much you can allocate to paying yourself first. You wouldn’t want to save for the future only to realize that what’s left can’t even cover your essential monthly costs.

- If your monthly income is 40 million VND and total expenses are 32 million VND, you’ll have around 8 million VND available to pay yourself first. This gives you a good idea of how much you can accumulate each month.

- Note that this number could be even higher. Once you know how much money you have left each month, you can begin to trim expenses to save even more.

- Cutting costs will be even more important if you end up with a deficit at the end of the month.

Set a Budget Based on Lower Expenses

Find Ways to Reduce Fixed Expenses. Although fixed, this doesn’t mean you can’t replace them with similar, lower-cost alternatives. Review each fixed expense and see if there’s a way to reduce them.

- For example, although your mobile phone bill is fixed each month, could you plan to use less data to save on costs? Similarly, while your rent might be fixed, if it takes up more than half your income, consider downsizing to a one-bedroom apartment or moving to a more affordable area.

- If you pay for car insurance, be sure to check with your broker annually to see if there are any better options. You can also keep looking for a better deal.

- If your credit card debt is high, consider consolidating your debts to reduce your fixed interest costs. This way, you can pay off your credit card debt with a loan that has a lower interest rate.

Find Ways to Cut Variable Costs. A large portion of savings can come from here. Review your monthly expenses carefully and pinpoint where your variable costs are going. Look at the small, recurring expenses that can add up over time, like coffee, dining out, grocery bills, fuel, or entertainment.

- When looking to reduce these costs, think about what you want versus what you need. Cut back on as many “wants” as possible. For example, at work, you might need lunch every day, but buying lunch at the canteen is a “want.” You can easily choose a more affordable solution like bringing your own lunch.

- The key here is to focus on the variable expenses that make up the bulk of your budget. Is most of your overspending going toward fuel, food, entertainment, or impulse shopping? You can reduce these areas by taking public transportation, preparing your own meals, or choosing more affordable forms of entertainment. Also, consider leaving your credit card at home to curb impulsive purchases.

- Search online for creative ways to cut spending in the categories that challenge you most.

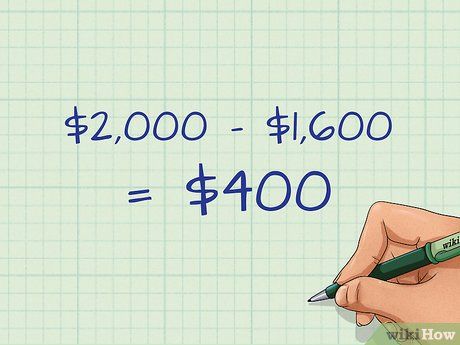

Calculate Remaining Money After Cuts. Once you’ve identified areas to cut back on, subtract them from your total expenses. Then, subtract the new total from your monthly income to find out how much you’ll have left by the end of the month.

- For example, if your monthly income is 40 million VND and total expenses are 32 million VND, after making cuts, you might save an additional 4 million VND, reducing your monthly costs to 28 million VND. This means you’ll have 12 million VND remaining each month.

Pay Yourself First

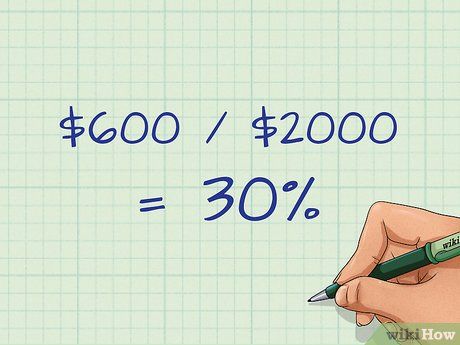

Decide How Much to Pay Yourself First. Now that you know how much you’ll have left at the end of the month, you can determine how much to allocate to yourself first. Experts vary on the recommended amount, but in the famous personal finance book *The Wealthy Barber*, author David Chilton suggests paying yourself 10% of your net income (after taxes and deductions). Other experts suggest figures ranging from 1% to 5%.

- The best strategy is to pay yourself as much as possible based on the remaining money each month. For example, if you have 12 million VND left after expenses and earn 40 million VND, you could save up to 30% of your income (though you may prefer to save 20%, leaving some room for unexpected expenses or rewards).

Set Savings Goals. Once you know how much you can allocate to yourself, set clear savings goals. These might include saving for retirement, education, or a down payment on a house. Determine the cost of each goal and divide it by how much you can pay yourself each month to calculate how many months it will take.

- For example, if you want to save 1 billion VND for a house down payment, and you have 12 million VND left each month to save, you would need 13 years to reach your goal.

- You could speed up the process by increasing your monthly savings to 12 million VND, cutting the time required in half.

- Remember, if you invest your savings in a high-interest account or other investment vehicles, the interest earned will shorten the time needed to reach your goal. To see how quickly your savings will grow with a given interest rate (such as 2% annually), search online for the term "Compound Interest Calculator".

Open a Separate Account for This Purpose. This account should only be used for a specific goal, usually saving or investing. If possible, choose an account with a higher interest rate. These types of accounts often limit the number of withdrawals, which is actually beneficial since you won’t need to make withdrawals frequently.

- Consider opening a high-interest savings account. Many financial institutions offer this type of account, and they typically provide much higher interest rates than standard checking accounts.

- If you're in the U.S., you might also consider opening a Roth IRA for your savings. A Roth IRA allows your assets to grow over time without being taxed. Within a Roth IRA, you can invest in stocks, mutual funds, bonds, or exchange-traded funds, all of which offer higher returns than a high-interest savings account.

- Other options include a Traditional IRA or a 401(k) plan.

Deposit Money into Your Account as Soon as You Receive It. If your salary is directly deposited, set up an automatic transfer of part of your income into a separate account. You can also schedule weekly or monthly automatic transfers from your main account to this account, as long as you maintain a necessary balance to avoid excessive withdrawal fees. The key here is to do this before spending any money on other expenses, including bills and rent.

Leave the Money There. Don’t touch it. Don’t withdraw it. You should have a separate emergency fund for unexpected situations. Typically, this fund should be sufficient to cover three to six months of expenses. Don’t confuse your emergency fund with investment or savings accounts. If you find yourself unable to pay bills, look for other ways to make money or reduce your costs. Don’t rely on credit cards (see the *Warning* section below).

Advice

- Even small savings will be valuable in the future.

- Start small, if necessary. Saving 100 or even 20 VND each week is better than saving nothing. As your expenses decrease or income increases, you can raise the amount you pay yourself.

- Set goals, such as "I will save 400 million VND in five years." This will help you stay committed to paying yourself first.

- The idea behind this is that if we don’t pay ourselves first in some way, we will find ways to spend all our money until very little is left. In other words, it seems that costs always "grow" to match our income. By cutting income through paying yourself first, your expenses will remain manageable. If not, you may need to become resourceful instead of depleting your own savings.

Warning

- If you become overly reliant on credit cards to pay yourself first, you lose the point of doing so. Why save 400 million for a down payment in the future when you’ll end up borrowing that amount (with interest)?

- It can be difficult to pay yourself first as advised above when you have urgent financial obligations, such as an overdue rent payment or a creditor knocking at your door. Some people believe that, regardless of the situation, you should always pay yourself first. Others believe that there are times when paying others first is the right choice. The line between these approaches is for you to define.