A financial report is a crucial document that reflects the financial situation of a company or organization. It includes the balance sheet, income statement, and cash flow statement. Financial reports are typically reviewed and analyzed by business managers, executives, investors, financial analysts, and government agencies. Besides being accurate and clear, these reports must also be prepared and submitted on time. You may feel overwhelmed when tasked with creating a financial report, but the accounting tasks involved are not as difficult as they may seem.

Steps

Preparation

Set the reporting period. Before starting, you need to determine the reporting period. While some companies report monthly, most financial reports are generated on a quarterly or annual basis.

- To identify the required reporting period, check your organization’s governing documents, such as the company’s rules, regulations, or founding documents. These may specify how frequently financial reports should be created.

- Ask the company director how often financial reports are required.

- If you are the company director, consider the most useful reporting period for you and use that as the date for the financial report.

Review the general ledger. Next, you need to ensure that all details in the general ledger are updated and recorded properly. Your financial report will be meaningless if the accounting figures it includes are inaccurate.

- For example, make sure all accounts payable and receivable are processed, reconcile bank account balances, and verify whether all purchase transactions and sales contracts have been recorded.

- You should also consider any debts that may not yet be recognized as of the financial reporting date. For instance, is the company using any services that have not been invoiced? Are there wages owed to employees but not yet paid? These items represent accrued liabilities and should be included in the financial report.

Gather any missing information. If reviewing the general ledger reveals missing information, check and search to ensure the completeness and accuracy of the financial report.

Prepare the Balance Sheet

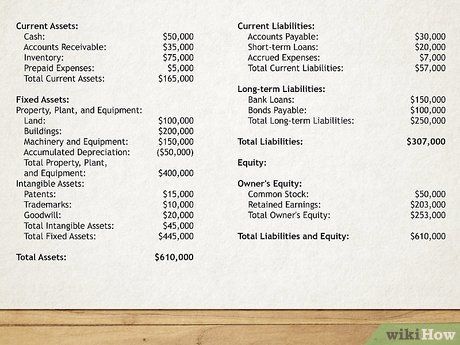

Create the balance sheet page. The balance sheet reflects assets (owned), liabilities (owed), and equity accounts such as common stock and retained earnings at a specific point in time. Title the first page of the financial report as “Balance Sheet,” and include the company name and the date the balance sheet is valid.

- Accounts in the balance sheet are recorded as of a particular date in the year. For instance, the balance sheet might be prepared using data as of December 31st.

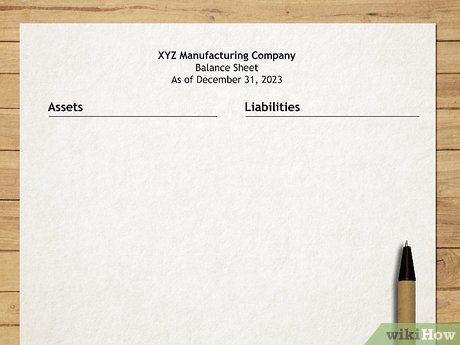

Format the balance sheet appropriately. Most balance sheets present assets on the left and liabilities/equity on the right. An alternative presentation format may be used, showing assets at the top and liabilities/equity at the bottom.

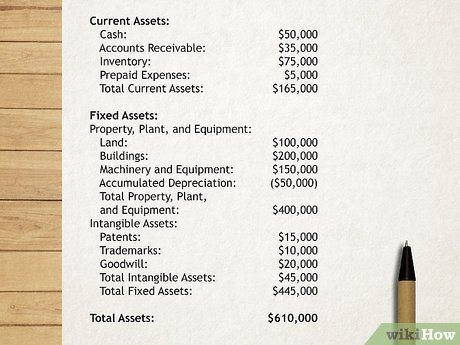

List assets. Begin the first section of the balance sheet with the title “Assets.” List all the different assets owned by the company.

- Start with current assets such as cash or any items that can be converted to cash within a year from the balance sheet date. Add a line for the total current assets at the bottom.

- Next, list long-term assets. These are assets that are not cash and cannot be easily converted to cash in the near future. Examples include real estate, equipment, and long-term receivables. Add a line for the total long-term assets at the bottom.

- Finally, add up the totals for current and long-term assets and label this line as “Total Assets.”

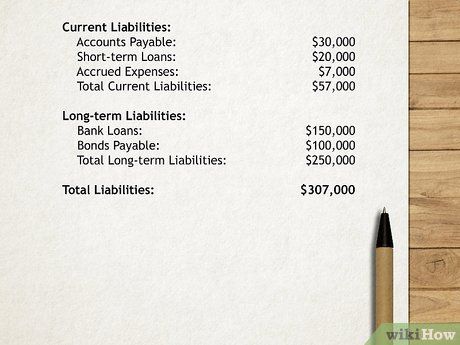

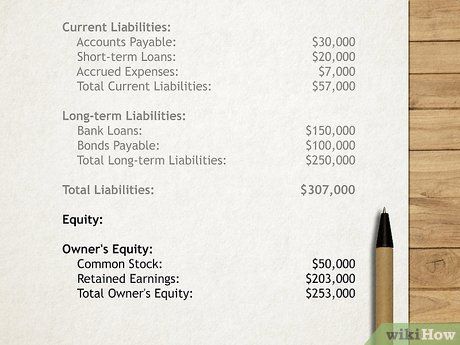

List liabilities. The next section of the balance sheet shows liabilities and equity. This section should be titled “Liabilities and Equity.”

- Start with short-term liabilities. These debts are due within one year and typically include accounts payable, accrued expenses, short-term mortgages, and other obligations. Add a line for the total short-term liabilities at the end.

- Next, list long-term liabilities. These are debts that are due beyond one year, such as long-term loans and bonds payable. Add a line for the total long-term liabilities at the end.

- Sum the totals for short-term and long-term liabilities, and name this line “Total Liabilities.”

List all equity sources. The equity section of the balance sheet follows the liabilities section and reflects the remaining value of the company if it were to sell all assets and settle all debts.

- Here, list all equity accounts such as common stock, treasury stock, and retained earnings. After listing them all, add them together and label this line “Total Equity.”

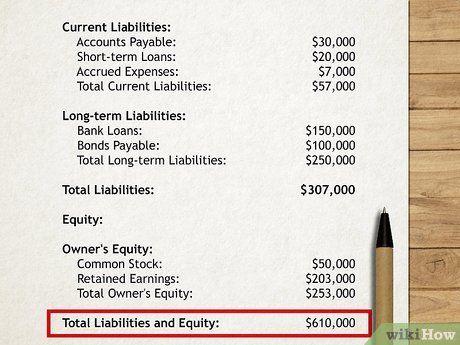

Add liabilities and equity. Add “Total Liabilities” and “Total Equity.” This line should be labeled “Total Liabilities and Equity.”

Check the balance. The figure for “Total Assets” should match “Total Liabilities and Equity” on the balance sheet. If this is true, your balance sheet is now complete, and you can proceed with the income statement.

- Equity should match the difference between the company’s assets and liabilities. As stated earlier, this is the amount left over if the company sold all its assets and paid off its debts. Therefore, liabilities plus equity should equal assets.

- If the balance sheet does not balance, review it. You may have missed or incorrectly allocated an account. Go through each column carefully to ensure everything required has been listed. Perhaps you forgot a valuable asset or an important liability.

Prepare the Income Statement

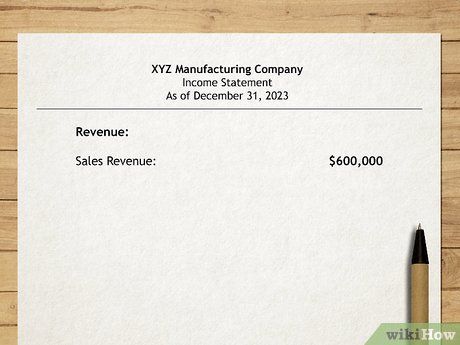

Prepare the income statement page. The income statement shows how much the company has earned and spent over a specific period. Label this page in your report as “Income Statement,” and include the company’s name as well as the reporting period.

- For example, the income statement is often prepared for the period from January 1st to December 31st of a particular year.

- Note that although the income statement might cover an entire year, you can also prepare financial reports for a quarter or a month. It is easier to understand financial statements when they represent the same time frame, though this is not required.

List revenue sources. List the different revenue sources and the values they generate.

- Ensure that each revenue source is listed separately, adjusted for any sales discounts or reductions as necessary, such as “Sales Revenue, 200,000,000 VND” and “Service Provision, 100,000,000 VND.”

- Arrange the revenue sources logically, based on how the company uses them. For example, you might organize them by geographic area, management team, or individual products.

- Once all sources of revenue are recorded, total them and label this total as “Total Revenue.”

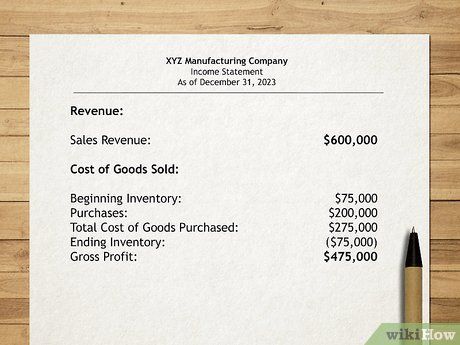

Record the cost of goods sold. This represents the total cost of developing or producing the products or services offered during the reporting period.

- To calculate the cost of goods sold, sum up direct material costs, direct labor, factory overhead, and shipping expenses.

- Subtract the cost of goods sold from the total revenue, and label this result as “Gross Profit from Sales and Service Provision.”

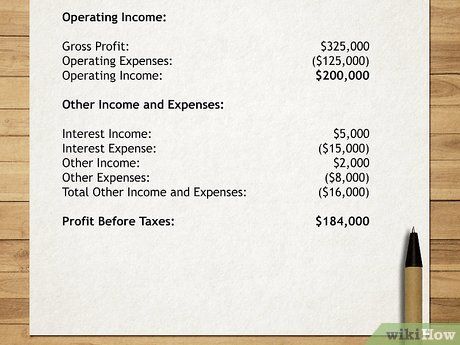

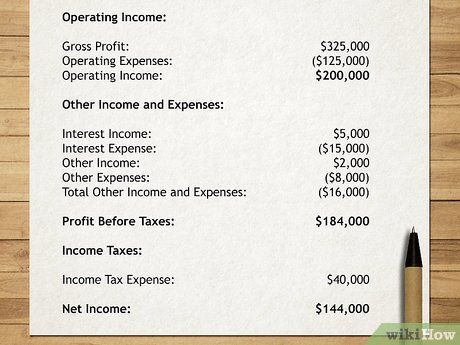

Record business operating expenses. These expenses include all the necessary costs for your business to operate. They cover administrative expenses and overhead such as salaries, rental fees, office supplies, and depreciation of fixed assets. It also includes advertising, research, and development costs. You may list these expenses separately to give the reader a clear overview of the company’s spending.

- Subtract these total operating expenses from the gross profit, and label the result as “Total Accounting Profit Before Tax.”

Record retained earnings. “Retained Earnings” represents the cumulative net profits and losses of the company from its inception.

- Add the retained earnings from the beginning of the year to the current year’s net profit or loss in order to balance the retained earnings.

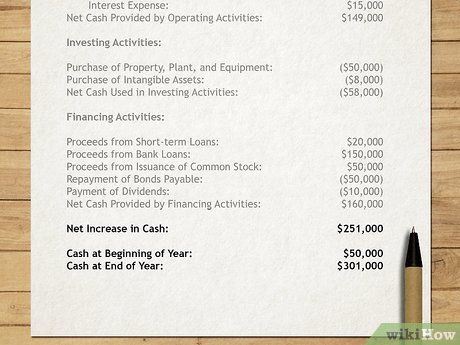

Prepare the Cash Flow Statement

Prepare the cash flow statement page. This statement monitors the inflow and outflow of cash for the company. Title the page as “Cash Flow Statement” and include both the company’s name and the reporting period.

- Similar to the income statement, the cash flow statement covers a set period, such as from January 1st to December 31st.

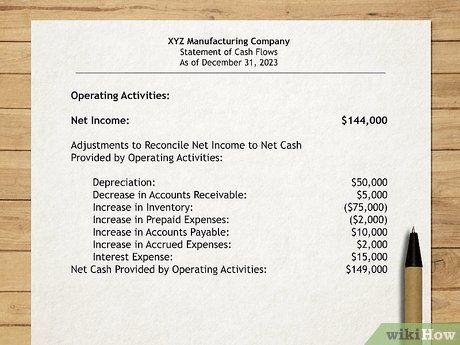

Create the operating activities section. This section is titled “Cash Flow from Operating Activities” and corresponds to the income statement you previously prepared.

- List all of the company’s business activities. This might include cash received from sales, services provided, or payments to suppliers. Sum up these items and label the result as “Net Cash Flow from Operating Activities.”

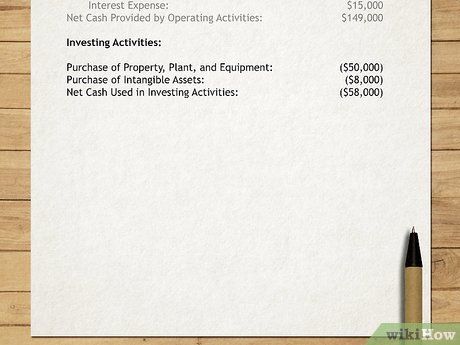

Create the investing activities section. This section is called “Cash Flow from Investing Activities” and aligns with the income statement you’ve prepared.

- This section involves cash transactions from investments in real estate, equipment, and securities such as stocks or bonds.

- Sum these amounts and name the total “Net Cash Flow from Investing Activities.”

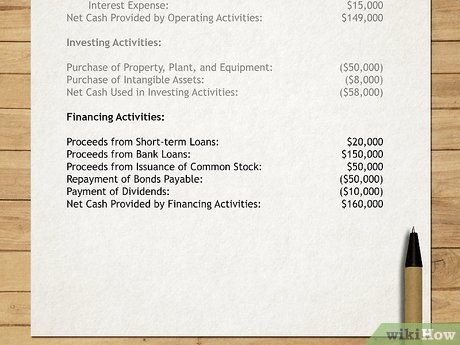

Record financial activities. The final section is titled “Cash Flow from Financing Activities”. This section pertains to the equity section of the balance sheet.

- It shows cash inflows and outflows related to securities and debts issued by the company. Sum these transactions and label the total as “Cash Flow from Financing Activities”.

Calculate the total. Sum the three sections from the cash flow statement and title it as “Net Cash Flow for the Period”.

- You may also add the net cash flow for the period to the starting balance of cash for the period. The sum of these two figures will equal the cash balance shown on the balance sheet.

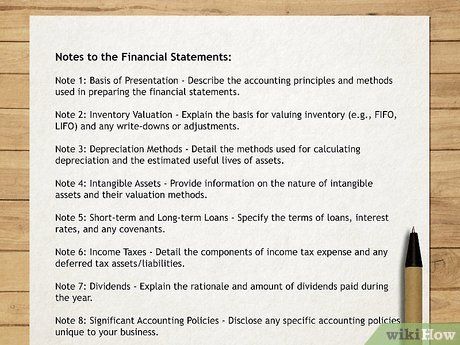

Include important notes or explanations. The financial report often includes a section titled “Notes to Financial Statements”. This section contains important information about the company. You should consider adding the most useful supplementary financial details here.

- The notes may cover the company’s history, future plans, or industry-specific information. This is an opportunity to explain to investors the significance of the report and what it shows, or does not show. It helps potential investors see the company through your perspective.

- For example, the notes may also include an explanation of the accounting practices used, along with the headings in the balance sheet.

- This section often details tax status, pension plans, and stock options offered by the company.

Advice

- To prepare financial statements, you can refer to the Vietnamese Accounting Standards (VAS). VAS sets the standards for the accounting and financial practices for all businesses and industries.

- Be sure to use specific titles for each section of the balance sheet and income statement. The information should be easy for readers to understand, especially for those who are unfamiliar with your company's specific characteristics.

- If you have trouble preparing the financial statements, you can refer to the financial reports of other companies in the same industry. This might give you insights on how to structure your own report. The State Securities Commission website provides financial reports for many companies.

Warning

- The professional regulations governing financial reporting and explanations are extensive. You may want to consider seeking advice from a Certified Public Accountant (CPA) or other financial consulting services to ensure your reports are accurately prepared and compliant with the law.