Saving money is often easier said than done. While most people acknowledge that saving is a wise decision, many struggle with putting it into action. Saving money isn't just about cutting back on spending; it can also be seen as a challenge. A smart saver carefully considers how to spend money and looks for ways to maximize their income. Keep reading the article below to learn more.

Steps

Saving Money Responsibly

Pay yourself first. The simplest way to save money instead of spending it is by making sure you don’t give yourself the chance to spend money in the first place. Set aside a portion of your salary directly into a savings or retirement account, so you don't have to worry about how much you need to save each month. Essentially, this is automatic saving, and you can use the savings when needed. Over time, the small amounts saved each month will grow (especially with an interest-bearing account), so start as early as possible to maximize the returns.

- To set up automatic transfers, you can talk to your payroll officer (or, if you’re a contractor, work with your intermediary payroll service). If you can provide a separate savings account apart from your regular salary account, you can set up an automatic deposit program with no issues.

- If, for any reason, you can’t set up automatic deposits for each paycheck (like when freelancing or receiving cash payments), decide on a fixed amount to deposit into the bank each month and make sure to stick to the plan.

Avoid accumulating new debt. Some debts are unavoidable. For example, wealthy individuals may have enough money to buy a house outright, but millions of people can only afford a mortgage. Therefore, it's important to avoid borrowing money whenever possible. Paying upfront is always more cost-effective than making installment payments due to accumulating interest over time.

- If borrowing is unavoidable, try to pay as much as you can upfront. The larger the down payment, the faster you can pay off the loan and the less interest you will pay.

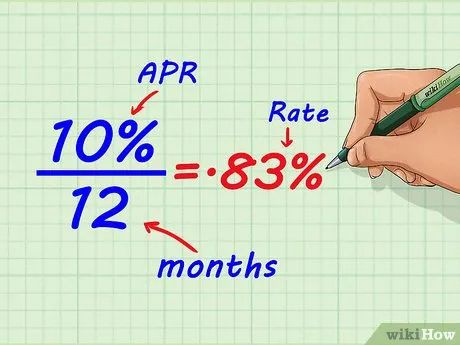

- While financial situations vary for each individual, banks generally recommend paying off debt at a rate equivalent to 10% of your pre-tax income or keeping it below 20%. A 36% debt-to-income ratio is considered the "upper limit" for debt.

Set realistic savings goals. Having a goal to save makes the process much easier. Set practical goals to motivate yourself; making decisions can be difficult, but it is necessary for responsible saving. Large goals, such as buying a house or retiring, may take many years or even decades to achieve. In such cases, regular monitoring of your progress is essential. Only by tracking your overall progress can you get a clear picture of how far you've come and how long it will take to reach your goal.

- Big goals, like saving for retirement, take a long time to achieve. During that time, financial markets will fluctuate. You might want to spend some time researching future financial market predictions before setting your goal. For instance, if you're earning well at the moment, financial commentators suggest saving at least 60-85% of your annual income to maintain your current lifestyle in retirement.

Create a timeline for your goal. Setting an ambitious (but realistic) timeline for achieving your goal can be a great motivator. For example, if you aim to buy a house in two years, you’ll need to research the average price of your dream home and begin saving for it (legally, you must pay at least 20% of the home’s value upfront).

- For example, if the house costs 600 million VND, you'll need to pay at least 600,000,000 x 20% = 120 million VND. Depending on your income level, evaluate whether this goal is feasible.

- Creating a timeline is crucial for short-term goals. If you want to buy a car but don't have enough money yet, you need to start saving for it as soon as possible to ensure you have transportation to work. A realistic but ambitious timeline can help you achieve your goal.

Tighten your budget. Setting a savings goal is easy, but if you don't track your spending, achieving your goal becomes difficult. To monitor your expenses, try creating a spending plan at the start of each month. Breaking down each expense can help you save money, especially if you want to save a portion of your salary as soon as possible.

- For example, if your monthly income is 8 million VND, your spending breakdown could look like this:

- Housing/utilities: 3 million VND

- Student loan: 500 thousand VND

- Groceries: 1 million VND

- Internet: 300 thousand VND

- Gas: 200 thousand VND

- Savings: 1.5 million VND

- Miscellaneous: 500 thousand VND

- Shopping: 1 million VND

Track your spending. Tightening your budget is essential for saving money, and without tracking your spending, you'll struggle to meet your goals. Monitoring your expenses in various categories each month can help you identify "problem areas" and adjust your spending habits to stay within your budget. However, tracking spending requires attention to detail. It's easy to track large expenses like buying a house or repaying loans, but you also need to focus on small expenses based on your financial situation.

- You can keep a notebook to track your spending. Develop a habit of recording each expense and keeping receipts (especially for large purchases). If possible, transfer this information into a larger notebook or spreadsheet program for long-term storage.

- There are now several smartphone apps available to help you track your spending (some apps are completely free).

- If your spending problem becomes serious, don’t hesitate to keep all receipts. At the end of the month, categorize your receipts and summarize them. You may be shocked by how much you’ve overspent on shopping.

Carefully check all your payments. Always ask for a receipt when shopping, and always print out the list of items purchased online. Make sure they haven’t overcharged you or sold you unnecessary items—this happens more often than you might think.

- For example, if you go out for drinks with friends and one of them orders a smoothie for the whole group, don’t feel obligated to pay for the entire group. Thinking that 'I’ll pay today, someone else will pay tomorrow' may seem fair, but this can create a significant financial gap for you.

- Don’t share payments just for convenience. If your meal costs one-third of the total bill, you shouldn’t pay half of the total.

- Consider downloading an app to help you calculate tips accurately.

Start saving as early as possible. Money saved in a savings account earns interest over time. The longer you save, the more interest you’ll accumulate. Therefore, starting early gives you a better advantage. Even if you only save a small amount each month in your twenties, don’t hesitate. The small amount saved in a high-interest savings account can accumulate significantly over time.

- For example, when you’re 20 and working a low-income job, you save 10 million VND and deposit it in a high-interest savings account with an annual interest rate of 4%. After five years, the interest earned will be around 2 million VND. However, if you start saving a year earlier, the interest would increase by 500,000 VND.

Consider contributing to a retirement account. When you’re young, healthy, and full of energy, retirement may seem like a distant concern. But as you age and lose your strength, it will become all you can think about. Unless you're one of the lucky few who inherit vast wealth, saving for retirement is something you’ll eventually need to think about once you have a stable career. As mentioned earlier, everyone’s financial situation is different, so saving 60-85% of your annual income to sustain your lifestyle in old age is a wise decision.

- If you haven't started saving for retirement yet, talk to your employer about opening a 401(k) account. This retirement account automatically deducts a portion of your salary, making saving easier. Additionally, the money saved in a 401(k) account is not taxed like your salary. Many employers offer matching programs, where they match a percentage of your salary contributions.

- In 2014, the maximum amount that could be contributed to a 401(k) account each year was 350 million VND.

Invest cautiously in the stock market. If you’re saving money and have a small surplus, the stock market may present an attractive (but risky) opportunity to make more money. Before investing, you need to understand that you could lose your investment, especially if you act impulsively. This method should not be used for long-term savings. Instead, treat the stock market as an opportunity to grow your wealth. In general, many people don’t need to invest in the stock market to save for retirement.

- For smart investment tips, you can refer to articles online.

Don’t get discouraged. When faced with challenges in saving money, it’s easy to become disheartened. Your situation may seem hopeless, and achieving long-term savings goals may feel impossible. However, even with small beginnings, you can always start saving. The earlier you begin, the sooner you’ll be on the path to financial security.

- If you feel discouraged about your financial situation, consider speaking to a financial advisor. Many advisory services offer free or low-cost consultations and can help you save money to achieve your goals. The National Foundation for Credit Counseling (NFCC) is a non-profit organization that’s a great place to start.

Cutting Expenses

Eliminate luxury expenses from your budget. If you’re struggling to save, start by cutting back on unnecessary expenditures. We often spend on things we don’t really need, so reducing these luxury expenses is a great first step to improving your financial situation. This won’t have a significant impact on your quality of life or work performance. It may be a bit tough without a scooter or cable TV, but you’ll get used to it. Here are a few simple ways to minimize luxury spending:

- Cancel unnecessary TV subscriptions and internet packages.

- Switch to a cheaper mobile plan.

- Trade in your expensive car for a more fuel-efficient, budget-friendly option.

- Sell unused electronics.

- Buy clothes and home furnishings at discount stores.

Find a cheaper place to live. For many people, housing costs are the largest expense in their budget. Saving money on rent can free up significant funds for important activities, like retirement savings. While it’s difficult to change your living situation, it’s worth seriously considering if you want to balance your budget.

- If you’re renting, try negotiating with your landlord for a lower rent. Landlords often prefer to keep existing tenants and may be open to discussions. You could even offer to work for reduced rent, like doing gardening.

- If you’re paying a mortgage, talk to your lender about refinancing options. You might be able to negotiate a better deal. When refinancing, aim to shorten the loan term as much as possible.

- You could also move to a more affordable housing market. According to recent studies, the most affordable housing markets in the U.S. are in Detroit, Michigan; Lake County, Michigan; Cleveland, Ohio; Palm Bay, Florida; and Toledo, Ohio.

Eat on a budget. Many people spend more on food than necessary. While dining at your favorite restaurant may feel like a treat, food-related spending can quickly add up and become unmanageable. Generally, buying in bulk is cheaper than purchasing daily, so get a membership card at your local supermarket or retail chain for discounts. Dining out is the most expensive option, so consider cooking at home to save money.

- Choose affordable, nutritious foods. Instead of buying pre-packaged foods, opt for fresh produce from grocery stores. You’ll be surprised at how affordable healthy foods can be! For instance, brown rice is nutritious and inexpensive.

- Take advantage of discounts and promotions. Many grocery stores (especially large chains) offer coupons and discounts at checkout. Make sure to use them!

- If you often eat out, stop now! Cooking at home is much cheaper than dining out. Plus, cooking regularly builds useful skills when hosting friends, family, or a date.

- Don’t hesitate to take advantage of free food resources in urgent situations. Food banks, soup kitchens, and shelters can provide free meals if necessary. If you need assistance, contact your local Department of Social Services for more information.

Reduce energy consumption. Many people accept their monthly utility bills without complaint. In reality, you can significantly reduce your energy usage with a few simple steps. These tips are easy to implement, and there’s no reason not to follow them if you want to save money. Additionally, cutting energy usage helps reduce pollution and lessens your environmental impact.

- Turn off lights when not in use. There’s no reason to leave lights on if no one is in the room (or the house). Turn them off when leaving. Put reminder notes on the door if you often forget.

- Avoid using heating or air conditioning when unnecessary. To lower the temperature, open windows or use fans. To stay warmer, dress in layers, use blankets, or use a space heater in one room.

- Invest in better insulation materials. If you can afford to upgrade your home, replacing old, inefficient insulation with more effective options can help you save money in the long run by reducing heat loss.

- Consider installing solar panels if possible. This is a long-term investment in both your future and the planet’s future. While the initial cost is high, solar energy can significantly lower your bills.

Choose cheaper modes of transportation. Owning, maintaining, and using a car takes a significant chunk of your income. Depending on how much you use your vehicle, fuel costs alone can be several million VND each month, not to mention expenses like a driver's license and maintenance fees. Instead of driving, consider more affordable transport options. This not only saves you money but also gives you more time for exercise, reducing stress after work.

- Look into public transportation near you. Depending on where you live, you might have access to various affordable public transportation options. Larger cities typically offer subways, trains, and trams for both urban and suburban travel, while smaller towns have buses and trains.

- Consider walking or cycling to work. If you don’t live too far from your workplace, these options are great for getting some exercise while breathing fresh air.

- If driving is necessary, carpooling is a great alternative. By sharing a ride, you can split fuel and maintenance costs with others, and you’ll also have someone to chat with.

Enjoy affordable (or free) entertainment. Reducing personal expenses doesn’t necessarily mean you have to give up fun. Changing your entertainment habits can help you strike a balance between enjoyment and responsibility. You’ll be amazed at how little you can spend to have a good time when you know where to look!

- Take advantage of community events. Nowadays, cities and towns post local event schedules online. Events hosted by local governments or community organizations tend to be inexpensive or even free. For instance, in a small town, you might find free exhibitions, outdoor movies in parks, or sponsored events.

- Read books. Compared to movies, video games, or other forms of entertainment, books are the least expensive (especially secondhand ones). A good book can captivate you, allowing you to experience life through fascinating characters or learn something you may never have encountered otherwise.

- Enjoy budget-friendly activities with friends. There are plenty of things you can do with friends that cost little or nothing at all. Examples include hiking, playing games, watching an old movie, exploring the city, or playing sports.

Avoid expensive addictions. Some bad habits can seriously undermine your efforts to save money. In the worst cases, these habits can turn into dangerous addictions that are hard to break. Worse still, many of these addictions can pose long-term health risks. Protect your wallet (and your health) by steering clear of them from the start.

- Avoid smoking. Everyone knows the harmful effects of smoking. Lung cancer, heart disease, stroke, and many other dangerous conditions are caused by tobacco use. Additionally, cigarettes are costly, with prices varying depending on the location.

- Don’t overindulge in alcohol. Having 1-2 drinks with friends is harmless, but regular heavy drinking can cause serious long-term issues like liver disease, nerve damage, weight gain, delirium, and even death. Alcohol addiction also becomes a financial burden.

- Stay away from drugs. Substances like heroin, cocaine, and methamphetamine are highly addictive and severely harm your health. They are much more expensive than cigarettes and alcohol. For example, country musician Waylon Jennings spent $1,500 a day (approximately 30 million VND) on cocaine.

- If you need help overcoming addiction, don’t hesitate to reach out to helplines. You can find more information at: here.

Smart Spending

Prioritize essential spending. Focus your money on necessary expenses first. Things like food, water, housing, and clothing should be your top financial priorities. This is clear—without a home or food, you won’t be able to achieve your financial goals. So, make sure you have enough to cover these basic needs before spending on anything else.

- However, just because essentials like food, water, and housing are necessary, it doesn’t mean you should overspend. For instance, cutting down on dining out is one of the easiest ways to reduce food expenses. Additionally, moving to a more affordable area or renting/buying a less expensive property can help lower housing costs.

- Depending on where you live, housing can consume a significant portion of your income. Experts suggest that you should never rent a place that costs more than one-third of your total income.

Start building your emergency fund. If you don’t yet have an emergency fund with enough money to cover living expenses in case you lose your income, it’s time to start saving. A modest amount in a secure account helps you maintain your lifestyle even if you lose your job. Once you’ve covered essential expenses, allocate some of your money towards your emergency fund until you’ve saved enough to cover living costs for 3-6 months.

- Keep in mind that living expenses depend entirely on where you live. You could get by for a few months on $1,500 in Detroit or Phoenix, but with that same amount, you might not be able to pay rent for even a month in New York. If you live in a high-cost area, your emergency fund will need to be larger.

- Besides helping you stay afloat during tough times, an emergency fund can also yield long-term benefits. Without an emergency fund, you may be forced to accept any job, even with a low salary. On the other hand, if you can afford to live without working for a while, you’ll have more options and might secure a higher-paying job.

Next, focus on paying off debt. Outstanding debts can hinder your efforts to save money. If you pay off small amounts at a time, you’ll end up paying more in the long run compared to tackling the debt head-on. To save money in the long term, dedicate a portion of your income to clearing debt as quickly as possible. Typically, it’s most effective to pay off the high-interest loans first.

- Once you’ve taken care of essentials and built a reasonable emergency fund, you can allocate most of your income to paying off debt. On the other hand, if you don’t have an emergency fund, you’ll need to split your income—one part for monthly debt payments and the other for your emergency fund.

- If you’re overwhelmed by multiple debts, consider consolidating them. You can combine several debts into one loan with a lower interest rate. Keep in mind, however, that the repayment term for the consolidated loan might be longer than the original debt.

- You might also want to try negotiating with lenders to lower your interest rates. If you file for bankruptcy, lenders won’t benefit, so they might be willing to reduce your rates to help you pay off your debt.

- For more information on how to pay off debt, refer to additional resources.

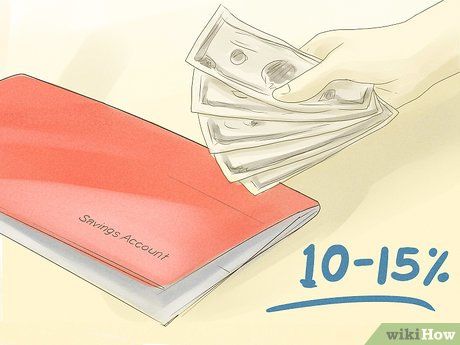

Start saving money. After setting up your emergency fund and paying off most (or all) of your debt, it’s time to begin saving in a savings account. Saving this way differs from an emergency fund, as you only dip into your emergency fund when absolutely necessary. Savings should be reserved for larger, important expenses like car repairs. However, try to avoid using your savings too frequently, allowing them to grow over time. Aim to save at least 10-15% of your monthly income in your twenties; experts agree this is a great target.

- When you receive your paycheck, you might feel tempted to spend right away. To avoid this, deposit money into your savings account immediately when you get paid. For instance, if you save 10% of your income and your paycheck is 8 million VND, transfer 10% (800,000 VND) straight to your savings account. This habit helps you avoid unnecessary spending and accumulate a decent amount over the years.

- An even better idea is to automate the saving process as much as possible, so you never even touch the money. For example, you can set up an automatic savings plan through your employer or a third-party app. This way, a portion of your salary or a fixed percentage can be transferred to your savings account without any effort on your part.

Spend smartly on non-essential items. If you’ve saved a portion of your income each month and still have extra money, consider investing in non-essential items that can improve your productivity, earning potential, and long-term quality of life. While these purchases are not as essential as food, water, or housing, they are wise long-term investments that could save you money in the future.

- For example, purchasing a comfortable chair for work may not seem necessary, but it’s a smart long-term choice because it boosts your productivity and prevents back pain (which could end up costing more in medical bills). Another example is replacing an old, worn-out water heater. While the old one could last a while longer, buying a new one will save you from future repair costs, which is a long-term saving.

- Other examples include spending on ways to travel more affordably, such as buying a monthly or yearly public transportation pass, or purchasing tools that help you work more efficiently, like headphones if your job requires hands-free tasks, or items that make work easier, like shoe lifts.

Spend on luxuries last. Saving money doesn’t mean living miserably. Once you’ve paid off your debts and built an emergency fund, making smart purchases that offer long-term benefits means you can absolutely treat yourself. Spending on luxuries responsibly is a way to reward yourself after hard work, so don’t hesitate to indulge in a luxury item to celebrate your improved financial situation.

- Luxuries include all non-essential items and services that don’t offer long-term benefits. These might be dining at fancy restaurants, going on vacations, buying a new car, cable TV, expensive utilities, and so on.

Tip

- If you receive unexpected money, save all of it but continue to set aside your usual savings. This way, you’ll reach your goal faster.

- Anyone can save something regardless of income. Starting with small savings helps you build a habit. Even saving just 100,000 VND a month shows that you don’t need to spend as much money.

- Always estimate your expenses as higher and income as lower than expected.

- Take care of your personal belongings so you don’t need to replace them frequently. Don’t throw things away until they are truly unusable. For instance, if your electric toothbrush breaks, you can still use it like a regular toothbrush. Continue using it until you buy a new one, or check if it's still under warranty.

- Shop with cash, and save your small change. Use a piggy bank or glass jar to collect coins. You might think small change isn’t worth much, but it adds up over time. Some banks even offer coin-counting machines. When you exchange coins, ask for a check so you’re not tempted to spend it.

- If you have a stable income, setting up a budget is easier. But if your income varies, predicting expenses becomes harder since you don’t know when you’ll get paid. List your budget to prioritize important goals first. Be cautious with spending, as it could be a while before your next paycheck.

- Spend wisely on hobbies. A key habit for saving is setting limits for yourself even when it comes to entertainment. If you’re into collecting model airplanes, scrapbooking, cycling, diving, etc., make firm rules that even when you allow yourself to spend on a hobby, you must still save appropriately. For example, if you buy a 1 million VND pair of gloves for cycling, make sure to save another 1 million VND at the same time.

- Serious about saving? Try doubling your savings! This plan does two things: it helps you save money regularly and quickly, while also showing you how much you spend on hobbies, and when your fun costs you double your money.

- If you’re able to share what you have, from food and living space to household items, do it. You can find a roommate or close friend to share costs, which can save money for both of you.

Warning

- If things go off track, don’t give up. Try to do better next time when you get paid.

- Don’t spend like you’re "throwing money out the window." It’s easy to get tempted when you receive your salary, but only buy what you’ve already planned for.

- After a long workweek, you might feel like treating yourself to something luxurious and tell yourself, "I deserve this." Remember that what you’re buying isn’t a gift for yourself—it’s a trade, exchanging money for a product. Of course, you deserve to reward yourself, but can you truly afford it? If not, you’re still valuable and deserve to achieve your savings goals!

- Unless your financial situation is truly dire, don’t cut costs when it comes to health-related expenses. Preventive care for yourself, family, and pets might cost 1 million VND for a doctor’s visit or 600,000 VND for heartworm medicine, but skipping these steps can lead to serious consequences and potentially cost you even more in the long run.

- If you’re saving money with friends, be prepared with a reason to explain why you can’t go out with them.