After creating your financial plan, the next step is putting it into action. A major risk when using credit cards is the temptation to swipe them without considering your established budget. This makes it hard to track your remaining funds. One strategy that many people find helpful is to return to the 'old-fashioned' method of using cash. Physically seeing money leave your hands and instantly knowing how much you have left is an excellent way to stay focused on your spending.

Steps

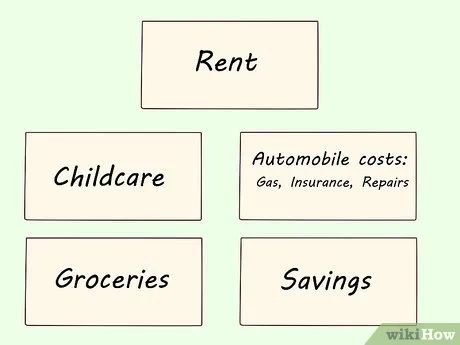

Budgeting. This means dividing your available money into different categories. Avoid creating a 'Miscellaneous' category, as you need to have a clear understanding of your spending. Here are some suggestions:

- Rent or mortgage payments

- Childcare costs

- Transportation: gas, insurance, repairs, etc.

- Groceries

- Club membership fees (or any other organizations): Gym, Girl Scouts, Yoga studio, etc.

- General service costs

- Taxes (if these aren't paid automatically or you need to pay them for any reason)

- Savings (which should be transferred to your bank account)

- Entertainment: dining out, concerts, movies, outings, etc.

Provide an envelope for each category. You will place the allocated money into these envelopes. You can use any envelope size that works best for you. The amount you'll be using outside should fit comfortably in an envelope that fits your wallet or purse. It is recommended to mark them with a marker for easy identification.

- Plastic envelopes are better for keeping in your purse or briefcase since paper envelopes tend to break down.

- Small, multi-pocket organizers for coupons or documents are also quite handy.

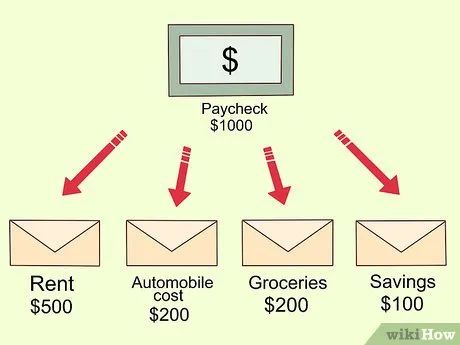

Divide your income and allocate it into separate envelopes. Every category where you need to spend incrementally (meaning not paying everything at once) should be paid in cash. You can leave your rent, mortgage, or any other one-time bills empty, or place a check inside the envelope, or you can completely exclude that envelope. However, the remaining envelopes should contain cash. For example, if your grocery budget is $500 (more than 10 million VND) until your next paycheck, place the $500 into the grocery envelope.

- Optional: Use a pencil to write the amount you’ve placed inside the envelope. This method will help you practice balancing your spending.

Withdraw from the envelope designated for a specific category whenever you need to spend. Track the remaining amount and write it on the back of the envelope for easy reference. If you run out of money for a particular category, you have two options:

- Once the money is gone, you cannot use any more from that category; you’ve spent all of it. This serves as a reminder that if you exhaust your entertainment fund, you will have no more money to spend.

- Use funds from another category. Of course, this means you’ll have less money available for that specific category.

Understand the Limitations of the Envelope Budgeting System. This is a great training tool, and for many, it’s highly effective. However, it also has some drawbacks:

- Not secure: If your purse or car is stolen, or if your roommate turns out to be a thief, storing cash is not safe. At least a debit card has a number, a PIN, and if it's stolen or used fraudulently, your account can be "frozen" to prevent further misuse. Cash doesn’t offer this protection.

- Lacks convenience: Using cash for everything means you can’t shop online. You can’t transfer money to your spouse in an emergency or make automatic online payments. If your car breaks down and you need urgent repairs, you won’t have the means to pay. This can become problematic.

- Creates Complex Financial Situations: This system works well for those with relatively simple financial situations. It’s quite effective for a 23-year-old single woman just learning how to budget. However, for more complex financial scenarios, this method isn’t as effective. A 62-year-old father owning a pet grooming business with a retirement savings account won’t be using much cash.

- It might not be a long-term solution. For many, this is the best way to manage their budget. However, the envelope system tends to work best as a temporary measure. Eventually, you’ll need to learn how to control your spending without relying on these envelopes.

Example

You receive your paycheck twice a month. Your salary is $1300 (more than 26 million VND). Here are the bills due before your next payday:

- Rent - $600 (more than 12 million VND)

- Utility bills, water, sanitation fees - $150 (more than 3 million VND)

- Electricity - $80 (more than 1.6 million VND)

- Student loan repayment - $100 (more than 2 million VND)

- Total: $930 (more than 18 million VND)

- Savings - $70 (more than 1.4 million VND), transfer to savings account

- Groceries (food, personal items, etc.) - $100 (more than 2 million VND), place cash in envelope

- Gas - $60 (more than 1.2 million VND), place cash in envelope

- Entertainment - $70 (more than 1.4 million VND), place cash in envelope

- Dining out - $70 (more than 1.4 million VND), place cash in envelope.

Advice

- If you’ve been setting aside money in an envelope for car expenses and have saved enough, consider continuing to save at least half of that amount for a new car or for general savings. Since you're used to this amount, it won’t slip your mind, and when it’s time to buy a new car, you won’t have to struggle with the cost. If you won’t need a new car for a while, consider putting the money into a savings account or a low-risk mutual fund.

- The envelope budgeting system is incredibly effective for tracking cash spending. Paying in cash, especially when you have a clear analysis of the money you’ve allocated, will help reduce your overall spending.

- Consider reusing old envelopes. You likely receive a lot of mail every month. If you open your mail neatly, you can reuse the envelopes that come with it.

- If you run short on cash in a category and think you might need more, you can borrow from another envelope. The last thing you want to do is use your credit or debit card.

- It’s wise to use larger denominations. Even if the total amount is the same, you’ll be less likely to spend it (especially in small portions) if you have to break larger bills to make purchases.

- Many people keep receipts for all their expenses and place them in the corresponding envelope. This helps you monitor your spending (and spot areas where you can cut back). It’s also quite useful during tax season.

- You might find it useful to have a dedicated envelope for your "bank" or "credit card". For example, if you want to buy a concert ticket online, you could use your bank card and replace the amount by taking the equivalent from the appropriate envelope and placing it into your "bank" envelope. The money stays there until the end of the month or your budgeting cycle, and you can then transfer it back to your account. This is a great method to avoid overspending, and you’ll feel better when you transfer the money back to your account!

- Never withdraw extra cash from your bank account or use your debit or credit card if you don’t want to exceed your budget. No budgeting system works unless you stick to the limits you’ve set. Sometimes, you’ll overspend, but the discomfort will motivate you to keep better track of your expenses in the future.

- Consider using digital tools to track the balance left in your envelopes. You can use apps like Envelopes 2 on iPhone or Envelopes (budget system) on Android.

- Save for yourself first. The goal of the budgeting system isn’t just to make sure you don’t overspend; it’s also a great way to save money. The best method is to save money before you even set your budget. This means depositing your paycheck into the bank and only withdrawing enough for the month or until the next paycheck arrives. Save the remaining money in the bank.

Items You Will Need

- Envelopes, any size that suits you

- Marker pens

- Cash

- Budget