Accounting, the meticulous recording of financial transactions, is a vital process for the success of businesses, both large and small. While larger companies often have large accounting departments with multiple staff members (and may even hire independent auditing firms), smaller businesses might only have one accountant. In a one-person company, the business owner may be responsible for managing accounting tasks alone. Whether you're interested in managing your finances independently or applying for an accounting position at another company, learning the basics of accounting is a valuable starting point.

Steps

Strengthen your accounting skills

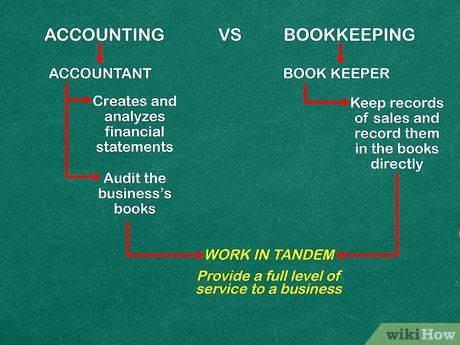

Understand the difference between bookkeeping and accounting. Bookkeeping and accounting are two terms that are often used interchangeably. However, there are key differences in the skills and responsibilities involved. A bookkeeper records sales transactions and directly enters them into financial records. Their daily tasks ensure that all of the business’s income and expenditures are properly documented. An accountant, on the other hand, creates and analyzes financial reports and may also audit the company’s records to ensure the accuracy and validity of the reports.

- Bookkeepers and accountants may work together to provide the highest level of service for a company.

- In many cases, the distinction between these two roles is formalized through certifications, degrees, or industry organizations.

Get familiar with creating spreadsheets. Microsoft Excel and other spreadsheet programs are invaluable for accountants: they allow you to track data in charts and perform calculations to create financial spreadsheets. Even if you have mastered the basic knowledge, you can still improve and learn intermediate and advanced skills for creating spreadsheets, charts, and graphs.

Read accounting books. You can visit your local library to find books about accounting or buy books from your favorite bookstore. Look for books on accounting written by authors with experience in the field, such as those offering well-researched information.

- Introduction to Accounting by Pru Marriott, JR Edwards, and Howard J Mellett is a widely-used textbook for introductory accounting courses and is considered an excellent starting point for anyone interested in accounting and related fields.

- College Accounting: A Career Approach by Cathy J. Scott is a widely used college textbook for accounting and financial management courses. You can also buy it with a CD-ROM for QuickBooks Accounting software: this could be an invaluable asset for passionate accountants.

- Financial Statements: A Step-by-Step Guide to Understanding and Creating Financial Reports by Thomas R. Ittelson is a bestselling introduction to financial reporting and could be the perfect starting point for entering the world of accounting.

Take an accounting course. You can find accounting courses at local community colleges or take free online accounting courses. Try visiting sites like Coursera or any other online educational platforms and search for free courses taught by top experts in the field of accounting.

Practice basic accounting operations

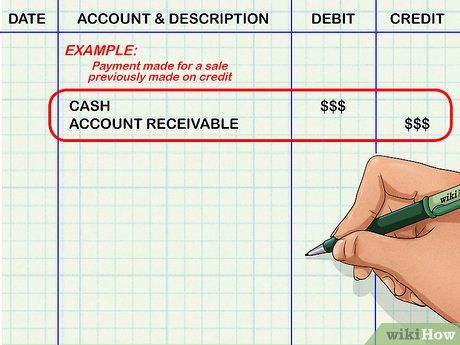

Understand double-entry bookkeeping. Accountants perform at least two journal entries for every transaction recorded by the business. This involves an increase in one or more accounts and a corresponding decrease in one or more other accounts. For example, when a business receives payment for a previous credit sale, the cash account will increase, and the accounts receivable (money owed by customers who have yet to pay for their purchases) will decrease. The amounts increased and decreased in these accounts are equal (and match the value of the order).

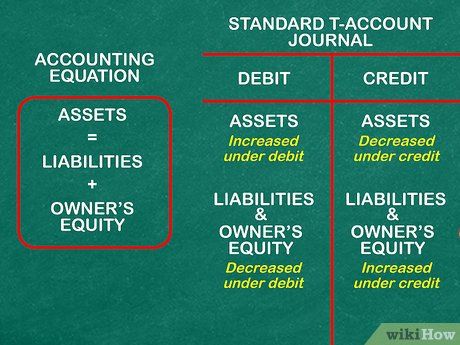

Recording Debits and Credits. Double-entry bookkeeping is done by recording debits and credits. Debits and credits reflect the increase or decrease in specific accounts when a transaction occurs. Once you understand the two points below, you’ll realize that debits and credits are interconnected:

- Debits are entries made on the left side of a T-account, while credits are recorded on the right side. We are referring to the standard T-account journal used to track changes on both sides of the vertical part of the 'T'.

- Assets = Liabilities + Equity. This is the most important accounting equation. Memorize it, as it serves as a guide for your debits and credits. On the left side of the '=', debits increase the account balance, while credits decrease it. On the right side, debits decrease the account balance, and credits increase it.

- When you debit asset accounts like cash, the account increases. However, debiting liability accounts, such as accounts payable, will decrease these accounts.

- Start by recording common transactions, such as paying electricity bills or receiving cash payments from customers.

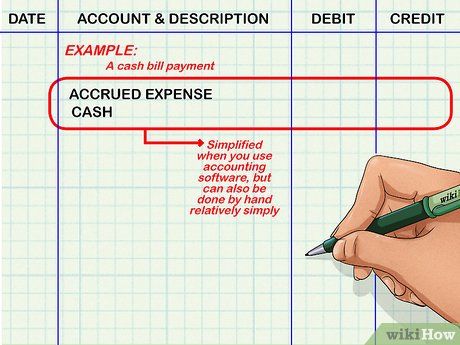

Creating and Maintaining the General Ledger. The general ledger is where the double-entry bookkeeping entries are recorded. Each transaction (which may include multiple debits and credits within a single event) is recorded in the appropriate account in the ledger. For example, if you pay a bill in cash, an entry will be made in the cash account and another in the accrued expenses account. While accounting software makes this process much easier, manual entry is not overly complicated.

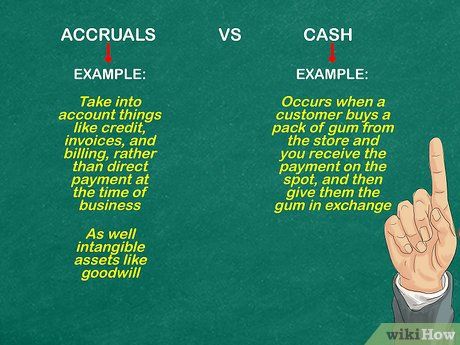

Distinguishing Between Cash and Accrual Payments. A cash transaction occurs when a customer buys a candy bar at a store, pays for it on the spot, and receives the candy immediately. Accrual transactions, on the other hand, involve things like credit purchases, invoicing, and billings, where payment is not made immediately at the time of the transaction. They also take into account intangible assets such as goodwill.

Learning About Financial Statements

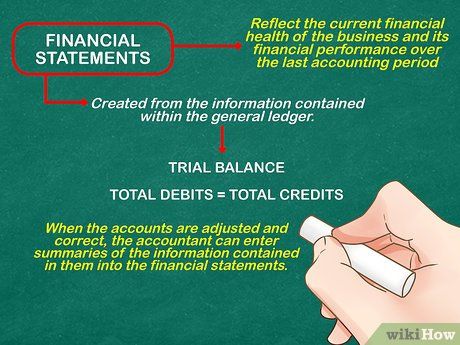

Understanding How to Prepare Financial Statements. Financial statements reflect the current financial health of a business and its financial performance during the most recent accounting period. They are created from the information contained in the general ledger. At the end of the accounting period, all accounts are totaled to create a trial balance. The total debits and credits for all accounts must match. If they don't, the accountant must check each account’s trial balance and make adjustments or corrections as necessary.

- Once the accounts have been adjusted and verified, the accountant can summarize the information from those accounts into the financial statement.

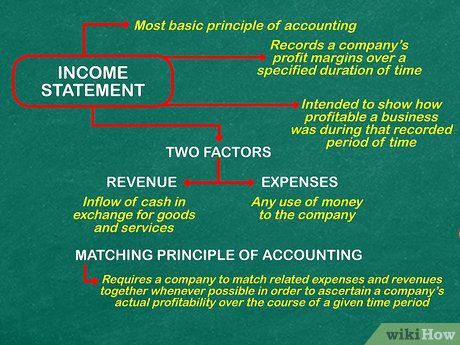

Learn how to prepare financial reports. The income statement is one of the most fundamental components in accounting. It records a company's profit margins over a defined period, which could range from a week to a year. The income statement is determined by two factors: revenue and the expenses of the business.

- Revenue refers to the inflow of cash over time that the business receives from providing goods and services. However, money doesn't necessarily have to be received within the same accounting period. Revenue may include both immediate transactions and accruals. When accruals are included in the income statement, the revenue for that week or month will reflect invoices sent out during that period, even if the money isn’t collected until the next reporting cycle. Therefore, the purpose of the income statement is to show how profitable a business is during the recorded period, not necessarily the actual cash flow during that time.

- Expenses are the total amount of money a company spends, whether it's for raw materials, labor, or other costs. Like revenue, expenses are reported in the period they are incurred, not necessarily when the company actually pays them.

- The matching principle of accounting dictates that businesses must record revenues and expenses together when possible to determine the true profitability of the business during the designated period. When a business is profitable, it typically follows a cause-and-effect relationship where an increase in sales will correspond with higher revenue and operational costs: demand for products for the store and sales commissions, if applicable, will also rise.

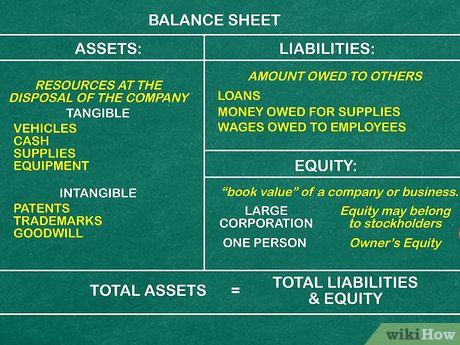

Prepare a balance sheet. While the income statement provides key financial details about a company's business performance over a set period, the balance sheet serves as a snapshot of the company's entire financial status at a specific moment in time. The balance sheet contains three important components: assets, liabilities, and shareholders' equity at a given point in time. You can think of it as an equation with assets on one side, and liabilities plus equity on the other. In other words, what you own always includes both what belongs to you and what is temporarily held on your behalf.

- Assets are everything the company owns or has control over. These can include tangible assets like buildings, cash, inventory, and equipment, as well as intangible assets like patents, trademarks, and goodwill.

- Liabilities are all the obligations the company owes at the time the balance sheet is prepared. This can include debts, unpaid goods, or wages that have not yet been settled.

- Equity is the difference between assets and liabilities. Sometimes, shareholders' equity is referred to as the 'book value' of a company. In the case of a large corporation, equity could be owned by shareholders. When a company is owned by an individual, it represents the owner’s equity.

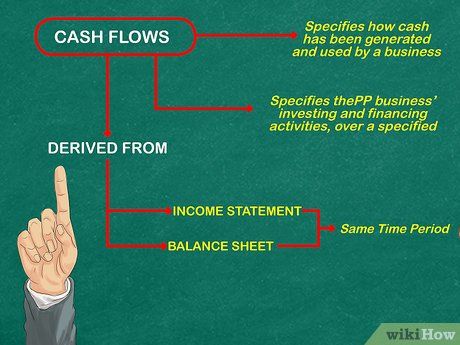

Create a cash flow statement. Essentially, a cash flow statement highlights how cash is generated and used by a business, as well as their investment and financing activities over a specific period. The cash flow statement is largely derived from the balance sheet and the income statement for the same period.

Learn accounting principles

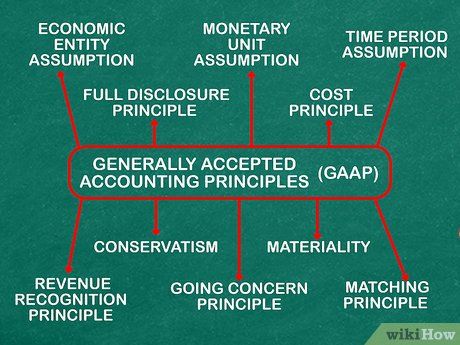

Adhering to Generally Accepted Accounting Principles (GAAP). These fundamental principles guide accounting practices through a framework of rules and assumptions designed to ensure transparency and integrity in all transactions.

- The Entity Assumption: Accountants working for a private company (owned by an individual) must maintain separate ledgers for the business’s transactions, excluding personal expenses or activities of the owner.

- The Currency Assumption stipulates that economic activities, at least in the U.S., will be measured in U.S. Dollars, and only those transactions convertible to USD will be recorded.

- The Time Period Assumption dictates that all financial transactions must be presented over specific periods, which are accurately documented. These periods tend to be short-term, with at least annual reports required. However, in many companies, reports are prepared weekly. The reports must clearly state the start and end dates of the period they cover. Simply stating the report date is not sufficient; it must specify whether it refers to a week, month, quarter, or fiscal year.

- The Cost Principle requires that transactions be recorded at the time they occur, excluding any adjustments for inflation.

- The Full Disclosure Principle mandates that accountants disclose all relevant financial information to all stakeholders, particularly investors and creditors. This information must be presented in the body or notes of the financial statements.

- The Going Concern Assumption assumes that a company will continue to operate for the foreseeable future and requires accountants to disclose any information suggesting that the company may face imminent financial distress or failure. In other words, if a company’s bankruptcy seems imminent, accountants must disclose this information to investors and all concerned parties.

- The Matching Principle requires that expenses must correspond to the revenues they help generate within the same financial report.

- The Revenue Recognition Principle asserts that revenue should be recorded when a transaction is complete, rather than when payment is received.

- The Materiality Principle allows accountants to use professional judgment to determine whether a specific amount is significant enough to be included in financial reporting. However, this principle does not justify inaccurate reporting, such as rounding numbers in financial transactions.

- The Conservatism Principle advises that accountants can report potential losses for a business, but cannot report potential gains until they are realized, preventing an inaccurate portrayal of the company's financial position to investors.

Complying with the Standards and Principles of the Financial Accounting Standards Board (FASB). FASB has established a broad set of principles and standards to ensure that stakeholders receive accurate and reliable information, that accountants maintain ethical conduct, and that financial reports are prepared with honesty. For a detailed outline of FASB’s conceptual framework, visit their website.

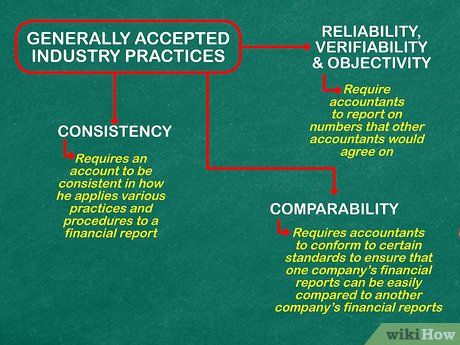

Adhering to Accepted Practices in the Industry. These are the expectations shared within the accounting profession that help guide the industry. They include:

- The Principle of Verifiability and Objectivity requires that the reported accounting figures be verifiable by other accountants. This relates not only to the accountant’s professional integrity but also ensures that future transactions are fair and truthful.

- The Consistency Principle demands that accountants apply consistent reporting practices and procedures. For instance, if there is a change in the cost flow assumptions of a business, the accountant is obligated to report the change.

- The Comparability Principle requires accountants to follow specific standards, such as GAAP, to ensure that financial reports can be easily compared across companies.

Advice

- To become a licensed Certified Public Accountant (CPA), you need to have a degree in accounting or related fields and pass the CPA exam along with the Ethics Exam.