No matter the amount of money one possesses, it often feels insufficient. We are ensnared in a cycle of spending and consumption. While a few individuals manage to escape this system and lead fulfilling lives with minimal resources, for most, this remains an unattainable dream. This list explores the currency we rely on for our daily purchases and also touches on related forms of money from similar historical contexts.

10. In God We Trust

Benjamin Franklin designed the continental dollar coin in 1776, featuring thirteen stars to symbolize the original colonies. Known for his wit, Franklin also inscribed the phrase “Time flies, so mind your business” on the coins. The phrase “In God We Trust” wasn’t legally permitted on U.S. currency until 1865, although earlier versions included “God and our right.” The inclusion of “In God We Trust” sparked considerable debate and occasionally fell out of favor. However, in 1908, it became mandatory to include the phrase on all coins and notes that had previously displayed it (though not on denominations that never had). Finally, in 1956, President Eisenhower signed legislation requiring the phrase on all U.S. currency.

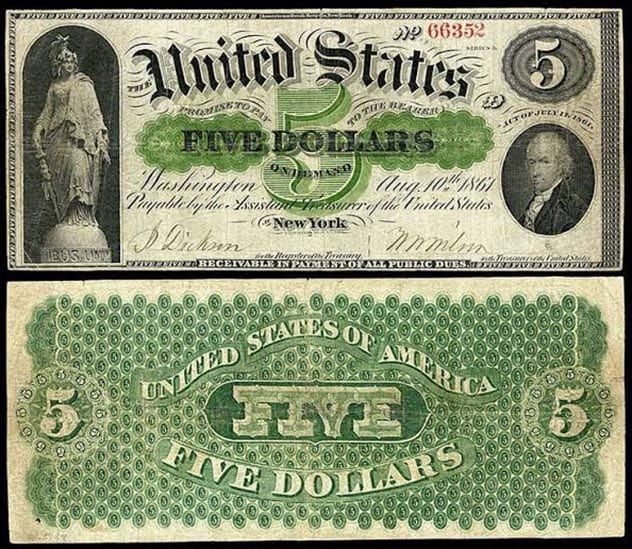

9. US Dollars Aren’t Greenbacks

Modern US dollars are not greenbacks. Greenbacks were a form of currency introduced by President Abraham Lincoln during the 1860s. These were created urgently as the Union faced a financial crisis to fund the Civil War. In 1861, Congress authorized the printing of 50 million “demand notes,” which featured green ink on the back, earning them their iconic name. However, these notes proved insufficient, prompting Lincoln to issue full legal tender US dollars, also printed in green. Although no longer in circulation, these notes, along with others from US financial history, remain valid currency. However, their historical value often exceeds their face value, making them prized collectibles.

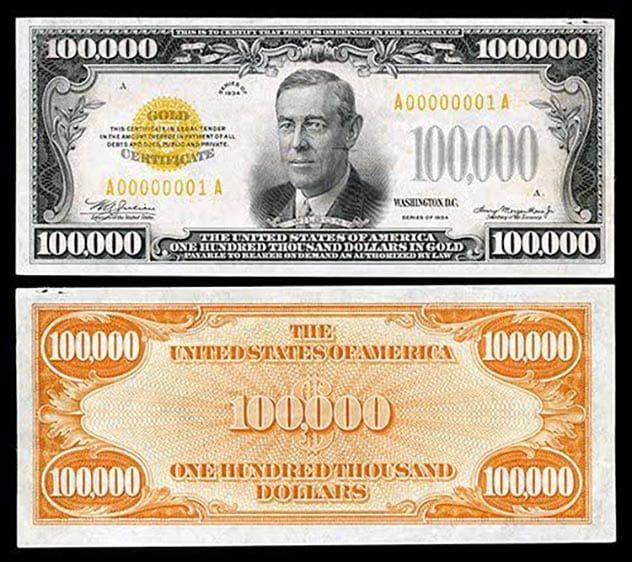

8. Rare Bills

Some US currency denominations are extremely rare or no longer in circulation. While the $2 bill is now widely recognized, making it less effective for pranks, the $100,000 bill from the 1930s is far more obscure. These were used exclusively for transactions between banks following the ban on private gold ownership and remain illegal for private possession. Other rare notes, such as the $500, $1,000, $5,000, and $10,000 bills, are still legal tender but are more valuable to collectors than their nominal worth, so they are best preserved rather than spent.

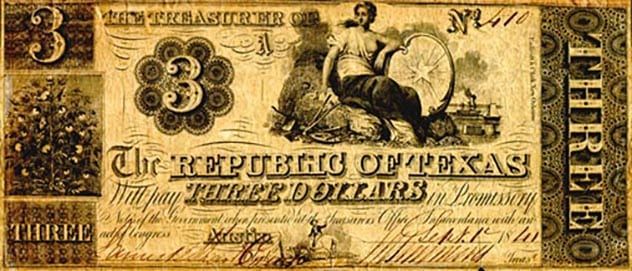

7. Graybacks and Redbacks

While greenbacks are well-known, graybacks and redbacks are far less familiar. Graybacks were the currency of the Confederate States of America, with 1 million issued just before the Civil War. Their value was tied to the Confederacy’s promise to pay if they won the war or negotiated a treaty. Their worth fluctuated drastically with the outcomes of battles, plummeting by 20% after the loss at Gettysburg.

The redback is another historical currency, serving as the official money of the Republic of Texas in 1839 and 1840. It was introduced to address the national debt and came in denominations of $5, $10, $20, $50, $100, and $500. The name “redback” originated from the distinctive red ink used in printing these bills.

6. Dollar Coins

The origins of the dollar trace back to the Spanish dollar, also known as the “piece of eight” (Real de a ocho or peso). This coin was widely circulated in pre-revolutionary America and globally, earning it the status of the first international currency. It remained legal tender in the US until 1857. The term “dollar” derives from “taler,” a 16th-century coin named after Joachimsthal, the source of its silver. The $ symbol’s origin remains debated, with theories suggesting it evolved from the letters P and S in Spanish Pesos or represents a stylized number 8, referencing the “pieces of eight.” Today, the silver dollar has transitioned into a gold dollar, similar to coins in other countries. Despite being issued as change by systems like the New York metro, the US dollar coin is rarely seen in circulation.

5. Money vs Currency

Before proceeding, it’s essential to clarify the distinction: money and currency are not the same. Here’s a concise explanation of what money truly represents:

Medium of Exchange: It is universally accepted for transactions. Portable: It can be easily transported and exchanged. Durable: It withstands repeated use without deterioration. Fungible: Each unit holds the same value as another. Divisible: It can be broken down into smaller units of value. Store of Value: It retains its purchasing power over time.

Gold is a classic example of money, fulfilling all the criteria mentioned above. However, the cash in your pocket does not qualify as a store of value, as you’ll understand further. The cash you carry is currency, acting as a substitute for real money. It serves a practical purpose, provided governments maintain its supply stability—though they often fail to do so.

Historically, the gold standard ensured a fixed amount of money to which currency could be tied. However, in 1971, Nixon disrupted this system by allowing the US dollar to float, promising a stable money supply. This move eliminated the need for the US to exchange currency for physical gold. The issue arose as increased government spending led to excessive money printing. This practice, known as inflation, devalues existing currency. If the government doubled the currency supply overnight, the cash in your pocket would lose half its value, effectively acting as a hidden tax.

The 2008 quantitative easing initiative drastically inflated the US dollar supply. This excess currency flowed into the stock market, resulting in irrational stock valuations—companies with zero profits boasting sky-high stock prices. This unsustainable trend raises concerns for the future.

4. No One Knows Who Owns The Private Banks

The Federal Reserve, a privately owned institution, is responsible for printing US currency. Contrary to popular belief, the Fed is not a government entity. It is owned by a network of state federal reserve banks, whose ultimate ownership remains a mystery. The control of the US dollar lies largely in the hands of an undisclosed group. The current Federal Reserve was established on December 23, 1913, with most Democrats supporting its creation and most Republicans opposing it.

This marks the third central bank in US history. The first was established in 1791 under George Washington, influenced by Alexander Hamilton, but its charter expired in 1811. In 1816, James Madison revived it as the second central bank, which operated until 1837. Following this, the US had no central bank until the current Federal Reserve was formed. Notably, during this period, Andrew Jackson became the only president to completely eliminate the national debt.

3. The End Is Nigh

Recall the Fed’s ownership of treasuries? Here’s a chilling fact: in 2008, the economy nearly collapsed as the housing market crumbled, dragging the banking sector down with it. In response, the government, alongside bank executives and the Federal Reserve, devised quantitative easing. Simply put, the Fed would purchase all the bad mortgages. This strategy became a go-to solution for future economic instability. If a company’s failure threatened the economy, the Fed could intervene by buying stocks, effectively bailing them out.

This approach eliminates risk from the free market, encouraging reckless behavior. What we have today isn’t true capitalism; it’s a pseudo-capitalist system driven by central banks. Companies succeed not through profits but because unknown bankers inject money into them. The Occupy Wall Street movement largely opposed this system. Distracting the public with trivial issues serves the banks’ interests, keeping the truth hidden behind the curtain.

President Trump often highlights the economy’s strength, aiming to boost consumer confidence. However, his optimism is misplaced. We are teetering on the brink of a severe depression, as the Federal Reserve prints money and purchases failing stocks to mask the impending crisis. In 2008, the Fed delayed the inevitable, but by 2019, we are approaching the end of that delay.

2. You Pay Tax Because Of It

This concept is difficult to grasp. The interest on treasuries must be paid, but since the currency originates from the Fed, where does the money for the interest come from? Taxes. In 1913, the Federal Reserve system was established, and the Federal government introduced income taxes. These taxes partially fund the interest payments owed to the private bank for the treasuries it holds. This system resembles a legal Ponzi scheme: the treasury creates currency from nothing to pay interest on currency it also created from nothing. As with all Ponzi schemes, this is unsustainable.

This raises a critical question: Why doesn’t the treasury simply print currency, as it did historically, to eliminate the interest burden? Abraham Lincoln did this. Garfield, who despised central banking, famously stated that controlling a nation’s money equates to controlling the nation itself, dominating all industry and commerce. McKinley opposed fiat currency, and JFK reportedly planned to restore the distinction between money and currency. These leaders shared more than just a disdain for central banks—they also shared a common fate.

1. It Is Made From Thin Air

Here’s a simplified breakdown of how currency is created: The US Treasury issues Treasury Bonds (t-bonds), which are promises to repay the face value plus interest over time, typically 30 years. The Federal Reserve then creates digital entries in its system, representing currency without physical form, and uses this to purchase the bonds from the Treasury. With these funds, the Treasury prints cash and mints coins. Essentially, currency is born from a promise of repayment with interest. Every dollar in circulation today represents a debt owed by the Treasury to bondholders, including the Federal Reserve and the public. The Fed alone holds $2.5 trillion in US Treasuries, accounting for about one-sixth of the nation’s debt held outside the government.

+ Root Of All Evil

A bonus fact, not exclusive to the US: “Money is the root of all evil!” This phrase suggests that Judeo-Christian teachings despise wealth. It’s often misinterpreted, as the Bible doesn’t condemn money itself. In 1 Timothy 6:10, it states: “For the love of money is the root of all kinds of evil. Some people, eager for money, have wandered from the faith and pierced themselves with many griefs.” The issue lies not in money but in the greed and moral corruption it can inspire.

The saying about a camel passing through the eye of a needle being easier than a rich person entering heaven is a metaphor. It highlights the challenges of maintaining virtue amidst wealth, reinforcing the idea that money can lead to moral struggles. So, if you’re wealthy, enjoy it—but use your resources to do good and help others along the way.