As oil prices drop, gas becomes cheaper, which is a relief for most people. Right now, the average price of gas in the U.S. is $2.05 per gallon, almost 15 cents less than it was a year ago. However, in the long run, low gas prices may not always be beneficial. They can significantly affect the economy and, ultimately, your finances.

High Oil Supply Is Behind the Low Prices

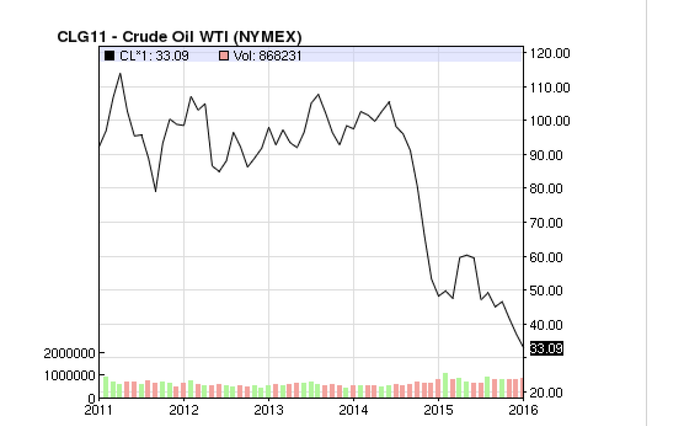

Since 2014, oil prices have taken a sharp dive, and you can clearly observe the decline here:

There are several complex political factors that contribute to this decline, but ultimately, it’s simple Economics: supply and demand.

Oil demand has slightly decreased—fewer people are driving, and fuel-efficient vehicles are more common—but the main reason is that there’s an overwhelming supply. The global overproduction of oil is a result of multiple factors happening simultaneously. As the New York Times explains:

U.S. oil production has nearly doubled in the past six years, pushing out oil imports that now need to find alternative markets. Oil from Saudi Arabia, Nigeria, and Algeria, once sold in the U.S., is now competing in Asian markets, forcing producers to lower prices. Meanwhile, oil production and exports from Canada and Iraq continue to increase year after year. Even Russia, despite its economic struggles, continues to pump oil.

OPEC (Organization of Petroleum Exporting Countries) plays a major role in controlling the downward trend of prices. The countries in this group produce about 40% of the world’s crude oil, according to the U.S. Energy Information Administration. Governments around the world have been encouraging OPEC to cut back on production to stabilize the market. Although there are many political factors at play, the bottom line is that OPEC isn’t doing that, which means the supply remains high, and prices continue to drop.

Extra Money in Your Wallet, For Now

For many of us, low oil prices have been a welcome relief. You’re spending less at the pump, you have more savings, and best of all—you can take that long road trip without breaking the bank.

From an economic standpoint and for everyday consumers, the primary benefit is clear: more disposable income while prices are low. According to AAA, consumers saved more than $115 billion on gas last year.

Economists also argue that cheap oil helps reduce inflation. Since nearly everything is tied to oil in some way, when oil prices drop, it theoretically keeps the cost of other goods and services down. This is fantastic for consumers, at least in the short run. Wall Street Journal national economics correspondent Josh Zumbrun explains:

The takeaway is that lower oil prices boost GDP [Gross Domestic Product] and consumer spending, while significantly lowering inflation.

If prices remain this low for the next year, it will provide a substantial benefit to consumers.

He notes that, over time, however, things tend to stabilize. We’ll adapt to lower prices and start spending more in other areas.

Interestingly, you might expect flight prices to decrease as airlines save on fuel. However, that hasn’t happened yet. Airlines argue that they haven’t lowered prices due to high demand, but some analysts suggest the airline industry has turned into an oligopoly. In other words, major players—Delta, Southwest, United, and American—simply won’t compete against each other.

The Danger of Deflation Destroying the Economy

Slow inflation isn’t always a positive thing. It can indicate a weak economy and, in the worst case, lead to deflation, which is considered the “nightmare scenario” for economists, according to NPR.

To grasp why, imagine you own a factory. To produce your goods, you first need to buy parts and raw materials. You promise your workers a fixed wage. You take out loans to expand your operations.

All these deals are based on the assumption that you'll be able to sell your products at a certain price. But what if those prices start to drop?

All of a sudden, you’re unable to pay back your loan or fulfill your commitments to your employees. You can’t afford the materials that are already sitting in your stockpile. You’re forced to sell products at a loss, while your competitors are also lowering their prices. This downward pressure triggers a vicious cycle, rapidly causing the value of businesses, homes, and other investments to plummet.

In short, falling prices mean businesses struggle, leading to job losses and reduced consumer spending. Eventually, we run out of money and start defaulting on loans and mortgages. Banks suffer, and the entire economy falls into a deep recession.

The bottom line is, too much inflation isn’t ideal, but neither is too little. Overall, the Federal Reserve, which aims to keep things stable, targets a steady 2% inflation rate. In 2014, the U.S. inflation rate was just 0.4%, and by the end of 2015, it had only risen to 0.5%.

Some fear that the drop in oil prices could eventually lead to deflation and trigger a recession. While predicting the future is always difficult, for now, that remains a concern.

Some economies, however, are struggling.

That’s not to say it’s all sunshine and rainbows, though. While many are reaping the benefits of lower prices, others are feeling the sting of cheap oil.

A perfect example of how cheap gas impacts the economy is my parents. My dad, who owns a small business in the energy sector, is bearing the brunt. Energy companies are making less profit, so they're cutting back on his services. On the other hand, my mom is enjoying the perks of filling up her car for under $40. Everyday consumers are saving, but those in the energy sector (which is a significant part of our economy) are taking a huge financial hit.

Oil-producing countries and states have been feeling the effects of this for quite some time. Jobs are disappearing, and wealth inequality is growing. Low oil prices are hurting countries across the globe. For instance, Nigeria, which heavily depends on oil to sustain its fragile economy, is now scrambling for solutions as prices continue to plummet. Christine Lagarde, Managing Director of the International Monetary Fund, recently stated in a speech:

The new reality of low oil prices and declining revenues has shifted the fiscal challenges for the Nigerian government. It's no longer about how to distribute the country’s oil wealth, but how to ensure that Nigeria can provide the essential public services its people deserve, including in education, healthcare, and infrastructure.

The New York Times reports that Persian Gulf nations are becoming less inclined to invest their wealth globally, and they may reduce financial assistance to other countries. Clearly, the consequences of lower oil prices are being felt on a global scale.

In the United States alone, there were 94,509 energy industry layoffs announced last year, which accounts for about 15% of all layoffs during that period. The drop in oil prices has weakened the energy sector, and this has had a knock-on effect on the broader economy.

Predicting the future is always uncertain, and right now, everyone is unsure of what will come next. However, the Energy Information Administration forecasts that oil prices will rise to $50 per barrel next year (currently at around $35). While this increase is modest, it could help prevent some of the negative consequences of cheap oil. For now, we can only enjoy the low fuel prices and hope for the best.

Artwork by Sam Woolley.