A home equity loan could be just what you need to fund a new nursery. Check out more images related to investing.

Photo courtesy stock.xchng

A home equity loan could be just what you need to fund a new nursery. Check out more images related to investing.

Photo courtesy stock.xchngImagine you and your partner are expecting a baby. You weren’t planning to start a family this soon, and your current home reflects that. The two-bedroom, one-bath bungalow was a perfect first home for two people, but now it feels cramped for a third. You love this house, so you want to make it work. The lot is big enough to add a new room - the nursery. You could tear down the back bedroom wall and build from there. Or, perhaps you could expand the kitchen, add a half bath, and the nursery at the same time. That would be ideal. But the question remains: how will you finance the renovation?

In this article, we’ll explore what it means to borrow against your home’s equity, the different types of home equity loans, and when it might be the right decision for you.

In the upcoming section, we’ll review some of the fundamental concepts.

Fundamentals of Home Equity Borrowing

Wondering how to finance a bathroom renovation? A second mortgage might be just what you need.

Photo courtesy stock.xchng

Wondering how to finance a bathroom renovation? A second mortgage might be just what you need.

Photo courtesy stock.xchngThere are several types of loans that let you use the equity in your home as collateral. The most traditional of these is the home equity loan, or second mortgage. With a second mortgage, you borrow a lump sum of money from the bank. You’ll be required to repay the loan within a set period at a fixed interest rate. For a project like a renovation, where you've received an estimate from your contractor and know the amount needed, a second mortgage is an excellent option.

Now that you’re familiar with the basics, let’s dive deeper into understanding equity.

Understanding Equity

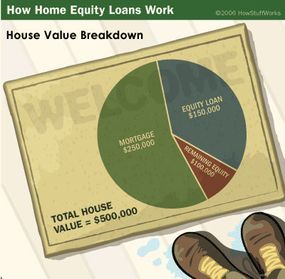

As previously mentioned, borrowers have multiple options when borrowing against their home’s equity: a home equity loan (also known as a second mortgage), a home equity line of credit (HELOC), and a reverse mortgage. A home equity loan or second mortgage is based on equity, or the value you hold in your property. Since homes generally increase in value over time, equity is determined by subtracting what you owe on your original mortgage from your home’s current market value. For instance, if you purchased your house for $350,000 and have paid off $175,000 of a $300,000 mortgage, and a recent appraisal values your home at $500,000, your equity would be calculated as follows:

$500,000 - $125,000 = $375,000

The $125,000 represents the remaining balance on your mortgage. As your home’s value appreciates—similar to how a stock or rare antique might increase in value—so does your home equity. Often, homeowners can use this equity to secure another loan. Just like with your primary mortgage, your house acts as the collateral for the loan. If you’re unable to repay the second mortgage, you might have to sell your home, or the bank could repossess it.

The duration of a second mortgage is often shorter than that of the first, typically ranging from five to 30 years. However, second mortgages are usually intended for smaller amounts, such as consolidating debts, financing a home addition, or covering expenses like a child’s college tuition. In some cases, homeowners may choose to borrow against the rising equity in their homes to gain financial flexibility.

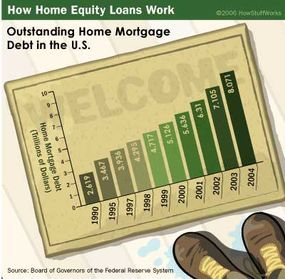

As homeownership has increased in the United States, so has the amount of mortgage debt.

As homeownership has increased in the United States, so has the amount of mortgage debt.Exploring Home Equity Loans and Reverse Mortgages

A home equity line of credit can be a valuable tool for funding your children's college education.

Photo courtesy stock.xchng

A home equity line of credit can be a valuable tool for funding your children's college education.

Photo courtesy stock.xchngA home equity loan is ideal when you need a specific sum of money for a project or investment. As discussed earlier, this loan allows you to borrow against the equity in your home. The loan is provided as a lump sum and repaid over a fixed period, which is why it's often called a second mortgage. Typically, the repayment schedule involves equal payments that, over time, pay off the entire loan amount.

Like other types of equity-based loans, the interest on a home equity loan may be tax-deductible up to $100,000.

Similar to a home equity loan, a Home Equity Credit Line (HELOC) uses your home as collateral. Essentially, a HELOC operates like a credit card. The lender assesses factors such as income, credit history, expenses, and existing debts to set a credit limit based on a percentage of your home’s equity.

A HELOC has a set time frame, but it works somewhat differently than a home equity loan. The first phase, often five years, is the period when the borrower can access funds through checks, electronic transfers, or a special credit card. Each plan may have different rules, and in some cases, a minimum withdrawal is required. Similar to a credit card, there is a borrowing limit. Once the borrower hits that limit, they must pay off some of the debt before borrowing more money.

The second phase starts after the borrowing period ends. Some plans offer an option to renew the credit line, while others require repayment of the debt, typically over another set period. In some cases, the remaining debt can be converted into a traditional loan after the draw period ends.

Since home equity lines of credit vary, it’s crucial to find one that suits your needs. When selecting a plan, consider the annual percentage rate (APR) and other associated costs. Like many other loans, home equity lines can come with various fees, though some lenders may waive some or all of them. These fees may include an application fee, property appraisal, initial charges like points (which reduce your credit limit), attorney’s fees, title search, mortgage preparation and filing fees, property and title insurance, taxes, maintenance or membership fees, and even transaction fees when accessing the line of credit.

Carefully consider the structure of the draw and repayment periods. Is the repayment period too short? Will you be able to make payments on the interest during the draw period? These are just some of the questions to ask when evaluating a home equity line of credit. Additionally, if you’re concerned that the ability to borrow funds almost at will may lead to overspending, then this might not be the right loan for you. However, if you need funds in installments — perhaps to pay a contractor for multiple projects or cover tuition fees — a home equity line of credit can be an excellent option.

Reverse Mortgages

A reverse mortgage may appear to be a contradiction. It’s money that the bank provides you, with the possibility of never having to pay it back during your lifetime. Plus, you don’t even need to have an income to qualify for it.

Of course, there are certain conditions that apply to a reverse mortgage. For starters, you must be at least 62 years old and live in the home for more than half the year. You also need to own the property. In some instances, if there’s only a small balance left on your mortgage, you could receive a cash advance from the reverse mortgage to pay off the remaining debt.

The idea of a loan that you never need to repay can be misleading. If you sell your home or move out permanently, you must repay the loan. If you remain in the home and hold the reverse mortgage until your passing, the loan will generally be settled using the home’s value. However, if your heirs want to retain the property, they will need to pay off the loan. Otherwise, the property may become the lender’s, or if the home’s value exceeds the debt, your heirs could sell the house, pay the loan, and keep the surplus.

Unlike a traditional mortgage, a reverse mortgage results in growing debt and shrinking equity. Your debt increases as your equity diminishes.

A reverse mortgage could help you buy that boat you’ve been wanting since retirement, but it’s crucial to remember that eventually, someone will need to repay the loan.

Photo courtesy stock.xchng

A reverse mortgage could help you buy that boat you’ve been wanting since retirement, but it’s crucial to remember that eventually, someone will need to repay the loan.

Photo courtesy stock.xchngAmong the various reverse mortgage options, the Home Equity Conversion Mortgage (HECM) stands out as the only one that is federally insured. The HECM program sets limits on loan costs and specifies how much the lender can offer. This makes it a potentially more affordable choice compared to other reverse mortgages. Typically, only reverse mortgages provided by state and local governments are less expensive than an HECM, but these often come with restrictions, such as being designated for specific purposes, and are primarily available to individuals with lower incomes. If you want to know how much you can get through a HECM or a Home Keeper Mortgage from Fannie Mae, try using this mortgage calculator.

Before taking out a reverse mortgage, it's crucial to assess whether it’s really the right option. Many individuals, when confronted with debt or significant expenses during retirement, are reluctant to sell their homes due to sentimental reasons or the hassle of moving. However, it’s wise to calculate the potential amount from selling your home and compare it to the costs of purchasing or renting a new property. In some cases, moving to a smaller or more manageable home could be more financially beneficial in the long run, helping your retirement income and sparing you the need for a reverse mortgage. This extra capital could also ease your financial burden and later benefit your heirs. For more on housing options, check out the AARP – there might be more alternatives than you think.

Read the Fine Print

Taking out a home equity loan puts your home at risk. It’s essential to ensure that you can meet the loan’s terms and conditions before committing to an agreement.

Taking out a home equity loan puts your home at risk. It’s essential to ensure that you can meet the loan’s terms and conditions before committing to an agreement.To safeguard consumers from entering into unfair loan contracts, the U.S. Congress passed the Consumer Credit Protection Act, also known as the Truth in Lending Act, in 1968. The Act requires lenders to clearly disclose key terms, costs, APR, payment schedules, variable rate information, and any other fees associated with home equity plans. Additionally, it allows consumers to cancel the agreement within three business days from the opening of the account. If the borrower decides to cancel, they must notify the lender in writing, and the lender must revoke the security interest in the borrower’s home and refund all application and loan fees.

The Consumer Credit Protection Act holds significant importance, particularly considering that individuals seeking second mortgages may find themselves in financially challenging, or even desperate, situations. In these circumstances, dishonest lenders might exploit their vulnerabilities, offering unaffordable loan terms or making undisclosed alterations to the agreement.

If the three-business day window to cancel has passed and you feel you have been taken advantage of, you should report the lender to the Federal Trade Commission. You can also reach out to consumer protection organizations, housing counseling services, or your state bar association for legal assistance.

Differences and Similarities

One advantage of a home equity loan is its fixed interest rate, allowing you to predict your monthly payments. In contrast, a home equity line of credit generally has a variable interest rate tied to a public index. Although this introduces uncertainty about your payments, it provides flexibility, typically offering the option to pay interest only or to pay both interest and a portion of the principal.

Interest rates for these types of loans are often based on indexes such as the prime rate, available in newspapers, or the U.S. Treasury Bill (“T-Bill”) rate. A variable rate will fluctuate as these rates change, but a variable-rate plan typically includes a cap on how high the rate can go over the term of the loan. Some plans also set limits on how low the rate can go. These changes align with adjustments made by the Federal Reserve. Additionally, many lenders add a margin to the interest rates, which is often expressed in points. For example, if the prime rate is 4.5 percent and the lender’s rate includes a one-point margin, your interest rate will be 5.5 percent.

Some lenders offer the option to switch from a variable interest rate to a fixed-rate within a home equity plan, or to convert part or all of your debt into a fixed-term installment plan. However, other lenders may restrict you from withdrawing funds once your interest rate hits the predetermined cap.

Repayment and Some Tips

Repaying a home equity loan or home equity line of credit depends on the specifics of the plan. Some plans may only require interest payments during the loan period, with the full principal balance due at the end of the term.

If your payment schedule results in an outstanding balance at the end of the loan, be prepared for a balloon payment. This payment can be made with available funds, by refinancing the loan, or by borrowing from another lender. Failing to make the balloon payment could put your home at risk.

Typically, your payment options will be flexible, giving you the ability to pay more than the minimum required. Many home equity borrowers choose to make extra payments toward the principal to avoid a large balance when the loan term ends. If you decide to sell your home before the loan term concludes, you will likely need to repay the full loan balance.

Equity Plan Guidance

Before applying for a home equity loan or HELOC, take a moment to reflect on whether you can handle additional debt. Is your job situation secure, and will you be able to repay the loan over time? If you’re facing financial difficulties, it may be worthwhile to consult a credit counseling agency. For mortgage-related issues, the Department of Housing and Urban Development can provide a list of approved housing counseling agencies. Generally, it’s recommended to take out a home equity loan only if you have a defined purpose for it. Although a home equity line of credit offers more flexibility compared to a home equity loan (second mortgage), using it casually, like a credit card, can lead to financial trouble later on.

Once you’ve made the decision to pursue a home equity loan, it’s essential to explore various lenders. Ensure that the lenders you approach are reputable and trustworthy. Predatory lenders often target vulnerable individuals, such as the elderly or those with low income or poor credit, attempting to deceive them into accepting unfavorable loans. Ask your friends and family about their experiences with banks, and thoroughly research potential lenders to ensure they are acting in good faith.

Given the numerous fees involved in loans and the complexities of variable interest rates, it can be challenging to determine what sets one lender apart from another. Consider using this worksheet from the FDIC to compare loan offers. It will guide you with important questions to ask and help you organize information about each lender.

Don’t shy away from negotiating with potential lenders. Treat it like shopping for a car. Inform them that you are comparing offers from different lenders and ask them to lower the various rates, fees, and points. Encourage them to improve their terms to beat those offered by other lenders.

After choosing a lender, make sure to request a “good faith estimate” for all associated charges. By law, the lender is required to provide this estimate within three days of your application. Take the time to review the forms you receive, and most importantly, don’t hesitate to ask questions! A week or two before the closing, confirm with your lender whether any terms have changed from the initial good faith estimate.

If you know someone experienced in loans, such as an accountant or tax attorney, ask them to review the estimate, loan documents, and contract. Once again, make sure to ask any questions you may have. Don’t feel rushed into signing any contract if you're unsure about something or if the language in the agreement is unclear. Never sign forms that have blank spaces. If a lender insists the fields should remain blank, draw a line through the space and initial it.

Above all, avoid borrowing more than you need or agreeing to terms you can’t afford. Even if the lender assures you that the terms are favorable, taking on a high loan-to-value ratio could make repayment difficult and risk your home ownership. The loan-to-value ratio is the proportion of the amount owed on your house compared to its total value. Lenders generally aim to keep your loan-to-value ratio under 80 percent. For instance, if you owe $250,000 on a house valued at $500,000, your loan-to-value ratio would be 50 percent. For a second mortgage, lenders typically won’t offer more than $150,000, which would bring your total loans to $400,000, resulting in a loan-to-value ratio of 80 percent ($400,000 divided by $500,000).

Be careful not to get overwhelmed by excessive mortgage debt.

Aim to maintain a loan-to-value ratio of less than 80 percent.

Certain lenders may offer loans that exceed 80 percent of your home’s value or even provide you with a loan greater than the actual worth of your property. These types of loans should generally be avoided as they often come with higher interest rates, the requirement for mortgage insurance, and could create financial difficulties if you need to sell your home.

For additional details regarding home equity loans and related subjects, please refer to the links on the following page.