Are you considering purchasing a new home? Chances are, you're also thinking about securing a mortgage. Discover more real estate images.

Mytour

Are you considering purchasing a new home? Chances are, you're also thinking about securing a mortgage. Discover more real estate images.

MytourOwning a home represents the fulfillment of the American dream. But this wasn't always the case. Before the 1930s, only 40% of American families were homeowners, as most lacked the necessary funds to buy a home outright. Additionally, mortgages, as we know them today, didn't exist until after the 1930s, leaving families without a bank loan designed for home purchases.

In simple terms, a mortgage is a loan where your home serves as collateral. The bank or lender provides you with a large sum of money (usually covering 80% of the home's price), which you are required to repay, with interest, over a specified period. If you fail to meet your payment obligations, the lender may take possession of your property through a legal procedure known as foreclosure.

For many years, the only available mortgage type was a fixed-interest loan paid back over 30 years, offering the advantage of stable and relatively low monthly payments. In the 1980s, adjustable-rate mortgages (ARMs) emerged, featuring an initially lower interest rate that adjusts annually throughout the loan's duration. During the housing boom, lenders began offering 'creative' ARMs with shorter reset periods, enticingly low 'teaser' rates, and no caps on rate hikes.

When bad loans are combined with a struggling economy, it leads to widespread foreclosures. Since 2007, more than 250,000 Americans have faced foreclosure proceedings each month [source: Levy]. These foreclosures are now escalating into complete repossessions, which are expected to reach 1 million homes by 2010 [source: Veiga].

Looking back at the surge in foreclosures since the housing crash, it's evident that many borrowers were unaware of the full terms of their mortgages. One study revealed that 35 percent of ARM borrowers didn't know whether their interest rate had a cap on how much it could increase [source: Pence]. This underscores the importance of understanding your mortgage terms, especially when dealing with 'nontraditional' loans.

In this article, we'll explore the various types of mortgages, explain key terms like escrow and amortization, and uncover the hidden costs, taxes, and fees that can accumulate each month. We’ll start with the most fundamental question: What exactly is a mortgage?

What Are Mortgages?

Legally speaking, a mortgage is "the pledging of property to a creditor as security for the payment of a debt" [source: YourDictionary.com]. In simpler terms, a mortgage is just a loan. For most people, it’s the largest loan they’ll ever take out. With a regular loan, there’s no specific collateral. The lender assesses your credit history, income, and savings to decide if you’re a good risk. But with a mortgage, the house itself is the collateral. If you fail to repay the loan (including all associated fees and interest), the lender has the right to take your home.

Banks are the traditional sources for mortgages. You can apply for a mortgage at the bank where you hold your checking and savings accounts, or you can compare offers from other banks to find the best interest rates and terms. If you don’t have time to shop around, a mortgage broker can help by reviewing different lenders and negotiating the best deal for you. However, banks aren’t the only mortgage providers; Credit unions, certain pension funds, and various government agencies also offer mortgage options.

Like most loans, mortgages come with an interest rate, which can be either fixed or adjustable, and a loan term, which typically ranges from five to 30 years. What sets mortgages apart from other loans is the array of additional costs and fees. Some of these costs, like closing costs, are one-time charges, while others are added to your monthly mortgage payments.

History of Mortgages

You might assume mortgages have been in existence for centuries — after all, how could anyone afford a home without a loan? Surprisingly, mortgages only became commonplace in the 1930s. What’s even more surprising is that it wasn’t banks who pioneered this idea; insurance companies did. These insurance companies didn’t aim to profit from interest and fees, but rather sought to acquire properties if borrowers defaulted on their payments.

It wasn’t until 1934 that modern mortgages were introduced. The Federal Housing Administration (FHA) played a key role in this development. To help pull the nation out of the Great Depression, the FHA created a new mortgage type targeting individuals who couldn’t secure loans through existing programs. At the time, only four out of ten households owned their own home. Mortgage loans were limited to 50 percent of a property’s market value, with repayment plans stretching over three to five years, often culminating in a large balloon payment. A loan covering 80 percent of the home's price meant your down payment was still 80 percent — not the amount you financed! Given such terms, it’s easy to see why most Americans were renters back then.

The FHA introduced a program aimed at reducing down payment requirements, offering options with 80 percent loan-to-value (LTV), 90 percent LTV, and even higher. This move prompted commercial banks and lenders to follow suit, making it easier for ordinary Americans to achieve homeownership.

The FHA also set a new precedent by qualifying borrowers for loans based on their actual ability to repay, as opposed to the old practice of securing loans through personal connections. The FHA also extended loan terms, introducing 15-year options and eventually the 30-year loans that have become the norm today.

The FHA further improved the home loan process by setting quality standards that homes needed to meet in order to qualify for financing. This was a smart move, ensuring that loans wouldn’t outlive the homes they were intended to finance. This shift in approach later became a standard that commercial lenders adopted as well.

Before the FHA, traditional mortgage plans consisted of interest-only payments, followed by a balloon payment that covered the full principal of the loan. This structure contributed to frequent foreclosures. The FHA changed this by implementing amortization, allowing borrowers to gradually reduce their principal with each monthly payment, ensuring the loan would eventually be fully paid off.

In the next section, we will break down the elements that make up the modern monthly mortgage payment and discuss the crucial concept of amortization in greater detail.

The Mortgage Payment

A down payment is the initial lump sum you pay upfront that reduces the amount you need to borrow. While you can choose any amount for the down payment, the standard is typically 20 percent of the home's purchase price. However, some mortgage options require as little as 3 to 5 percent down. A larger down payment reduces the amount you need to finance, leading to lower monthly payments.

The monthly mortgage payment includes several components, collectively known by the acronym PITI:

- Principal - The total amount borrowed from the lender, excluding the down payment.

- Interest - The fee the lender charges you for borrowing the money, usually expressed as a percentage of the loan amount.

- Taxes - Property taxes are typically paid through an escrow account, where the money is stored until it is due to the local tax authority.

- Insurance - Most mortgage agreements require you to purchase hazard insurance to cover potential losses from incidents like fire, storms, theft, floods, and more. If your equity is below 20 percent, you may also be required to buy private mortgage insurance, which will be discussed in detail later.

With a fixed-rate mortgage, your monthly payment stays mostly the same throughout the life of the loan. However, the portion that goes toward paying down the principal and the interest portion of the payment shift over time. This process, where both the principal and interest are gradually paid off, is referred to as amortization.

When reviewing the amortization schedule of a standard 30-year mortgage, you'll notice that the borrower pays significantly more interest than principal during the initial years of the loan. For instance, on a $100,000 loan with a 6 percent interest rate, the monthly mortgage payment is $599. In the first year, approximately $500 of each payment goes toward interest, while only $99 is applied to the principal. It’s not until year 18 that the principal payment exceeds the interest.

Amortization allows you to gradually pay off the interest on your loan, instead of facing a large balloon payment at the end. However, the downside is that over 30 years, you’ll end up paying $215,838 for the initial $100,000 loan. Additionally, it takes a longer time to build equity in your home since the principal payments are minimal during the early years. Equity refers to the difference between your home’s value and the outstanding balance on your loan.

Despite the costs of long-term amortization, 30-year fixed-rate mortgages aren’t necessarily a bad deal. In fact, we’ll dive deeper into the benefits of these mortgages on the next page.

Fixed-rate Mortgages

Not too long ago, the 30-year fixed-rate mortgage was the only option available from lenders. A fixed-rate mortgage features an interest rate that remains unchanged throughout the life of the loan. This means that not only does your interest rate stay fixed, but your monthly mortgage payment will remain consistent for 15, 20, or 30 years, depending on the mortgage term. The only variables that could change are your property taxes and insurance payments, which may fluctuate and are included in your monthly bill.

The interest rates on fixed-rate mortgages fluctuate with the broader economy. When the economy is thriving, interest rates tend to be higher than during a recession. Within these broader trends, lenders determine rates based on a borrower's credit history and the duration of the loan. Here are the benefits of opting for a 30-year, 20-year, or 15-year mortgage term:

- 30-year fixed-rate -- As the longest term, this loan results in the most interest paid over time. While that may not sound ideal, it also allows for the highest tax deductions on interest payments. Additionally, this long-term loan offers the lowest monthly payments.

- 20-year fixed-rate -- These are less common, but the shorter term means you'll accumulate more equity in your home faster. Larger monthly payments typically result in a lower interest rate compared to the 30-year mortgage.

- 15-year fixed-rate -- Similar to the 20-year loan, this term offers quicker loan repayment, higher equity buildup, and a lower interest rate, but comes with even higher monthly payments.

Fixed-rate mortgages provide long-term stability, which appeals to borrowers planning to stay in their homes for at least a decade. On the other hand, some borrowers prioritize securing the lowest interest rate possible, which is why adjustable-rate mortgages (ARMs) are an attractive option, as we'll discuss next.

Adjustable-rate Mortgages

An adjustable-rate mortgage (ARM) has an interest rate that can change, usually on an annual basis, depending on market conditions. This fluctuating rate impacts the size of your monthly mortgage payment. ARMs are appealing to borrowers because the initial rate is typically much lower than that of a conventional 30-year fixed-rate mortgage. Even in 2010, when interest rates for 30-year fixed mortgages were at historic lows, the ARM rate was nearly a full percentage point lower [source: Haviv]. ARMs are particularly advantageous for borrowers who anticipate selling their home within a few years.

If you're thinking about an ARM, it's crucial to remember that plans don't always unfold as expected. Many borrowers who intended to sell their homes quickly during the real estate boom found themselves stuck with a "reset" mortgage they could no longer afford. A significant number of these borrowers didn't fully grasp the terms of their ARM agreement. Here are the essential details to check for:

- How often your interest rate adjusts -- Typically, a standard ARM adjusts every year. However, there are other options such as six-month ARMs, one-year ARMs, two-year ARMs, and more. A commonly used "hybrid" ARM is the 5/1 year ARM, which has a fixed rate for the first five years before adjusting annually for the rest of the loan. A 3/3 year ARM has a fixed rate for the first three years, then adjusts every three years.

- Additionally, there will be caps that limit how much your interest rate can increase during the loan's term and how much it can change with each adjustment. Interim or periodic caps set limits on how much the interest rate can rise with each adjustment, and lifetime caps dictate the maximum interest rate for the entire loan. Never commit to an ARM without caps!

- The interest rates for ARMs are typically based on one-year U.S. Treasury bills, certificates of deposit (CDs), the London Inter-Bank Offer Rate (LIBOR), or other market indexes. When mortgage lenders determine ARM rates, they reference the index and add a margin of 2 to 4 percentage points. Tied to these indexes, when interest rates increase, your ARM rate will follow suit. However, the catch is that if interest rates decrease, your ARM rate might not [source: Federal Reserve]. Make sure to read the fine print carefully.

Next, let's explore some of the less conventional mortgage options, including government-backed loans, balloon mortgages, and reverse mortgages.

Other Types of Mortgages

Let's begin with a high-risk mortgage known as a balloon mortgage. A balloon mortgage is a short-term loan (typically five to seven years) that is amortized as though it's a 30-year loan. The advantage here is that you make relatively low monthly payments for five years, but here's the catch. At the end of those five years, you still owe the bank the remaining balance on the principal, which is often close to the original loan amount. This "balloon" payment can be devastating. If you're unable to sell or refinance the home within five years, you're in trouble.

Reverse mortgages provide a unique benefit by paying you as long as you remain in your home. These loans are intended for homeowners aged 62 and above who require a cash flow, either as a monthly payment or through a line of credit. Essentially, the homeowner borrows against the equity in their home, but the loan does not need to be repaid unless the home is sold or the owner moves out. However, these loans often come with high closing costs, and homeowners are still required to pay taxes and mortgage insurance [source: Moore].

Three federal agencies collaborate with lenders to offer discounted rates and terms for eligible borrowers: the Federal Housing Administration (FHA), which is a part of the U.S. Department of Housing and Urban Development; the Veterans Administration (VA); and the Rural Housing Service (RHS), a division of the U.S. Department of Agriculture.

These agencies don't lend directly to borrowers. Instead, they insure loans issued by approved mortgage lenders. This also includes refinancing mortgages that are no longer affordable. Borrowers with poor credit may find it easier to secure a loan through an FHA-approved lender because the lender knows that if the borrower defaults, the government will cover the loss. FHA loans only require a 3% down payment, which can be gifted by a family member, employer, or charitable organization [source: HUD]. Commercial mortgages typically don't allow this.

Similar to FHA loans, loans backed by the Veterans Administration (VA) are not directly lent to borrowers but are guaranteed by the agency. VA-backed loans offer favorable terms and relaxed criteria for qualified veterans. Veterans can secure a loan with no down payment as long as the home's purchase price doesn't exceed the county's loan limits.

If you live in a rural area or a small town, you may be eligible for a low-interest loan through the Rural Housing Service (RHS). RHS provides both guaranteed loans through approved lenders and direct loans funded by the government, helping low-income families purchase homes.

Next, let's dive into the topic of interest. Have you ever wondered what all those percentages actually mean?

Understanding APR

One of the most puzzling aspects of mortgages and loans is understanding how interest is calculated. With factors like compounding, loan terms, and others in play, comparing different mortgages can feel like comparing apples to oranges—it's just not that straightforward.

For instance, how would you compare a 30-year fixed-rate mortgage at 7 percent with one point to a 15-year fixed-rate mortgage at 6 percent with one-and-a-half points? You need to consider not just the interest rates but also the associated fees and costs of each loan. How can you make an accurate comparison? Fortunately, the Federal Truth in Lending Act mandates that lenders disclose the effective percentage rate and total finance charge in dollars, so you're not left guessing.

The annual percentage rate (APR) is an essential tool to help you compare the true costs of loans. It represents the average annual finance charge, which includes fees and other costs, divided by the loan amount. The APR is always slightly higher than the interest rate because it factors in additional expenses, such as origination fees, points, and PMI premiums.

Here's a practical example to demonstrate how the APR works. Imagine you come across an ad offering a 30-year fixed-rate mortgage at 7 percent with one point, and another ad offering the same loan at the same rate but with no points. Seems like an easy choice, right? Actually, it's more complicated than that. Fortunately, the APR helps by factoring in all the details in the fine print.

Let’s say you need to borrow $100,000. In both cases, your monthly payment would be $665.30. If the point is 1 percent of the loan amount ($1,000), and you have additional fees — such as a $25 application fee, a $250 processing fee, and $750 in other closing costs — these fees total $2,025. So, the actual loan amount used to calculate the true cost is $97,975 ($100,000 - $2,025). To find the APR, you calculate the interest rate that would result in a monthly payment of $665.30 for a loan of $97,975. This interest rate turns out to be 7.2 percent.

So, the second lender might seem like the better option, right? Not so fast. Continue reading to discover how APR and origination fees are related.

The Origination Fee

The origination fee is how lenders earn money upfront on your mortgage. These fees are typically calculated as a percentage of the loan, usually ranging from 0.5 to 1 percent for U.S. mortgages [source: Investopedia]. Going back to our APR example, imagine the second lender charges a 3 percent origination fee, plus an application fee and other closing costs that total $3,820. This reduces the loan amount to $96,180, which results in an APR of 7.39 percent. So, even though the second lender advertised no points, its higher origination fee leads to a higher APR.

The key takeaway is straightforward: Don’t focus solely on the interest rate. Make sure to ask for the APR and compare it across different lenders. Additionally, be aware of which fees are factored into the APR. Commonly included fees are origination fees, points, buydown fees, prepaid mortgage interest, mortgage insurance premiums, application fees, and underwriting costs. However, certain fees, such as title insurance and appraisals, are typically charged by all lenders and cannot be negotiated.

Fortunately, you don’t have to calculate the APR yourself. The lender will provide it to you along with the Federal Truth in Lending Disclosure. All you need to do is understand its significance.

Here are a few additional factors to consider when evaluating the APR:

- The more you borrow, the less noticeable the impact of those fees will be on the APR, as the APR is calculated based on the overall loan amount.

- The amount of time you stay in the home before selling or refinancing has a direct effect on your effective interest rate. For instance, if you move or refinance after three years instead of the full 30 years, and you paid two points at the loan closing, your effective interest rate will be significantly higher than if you stayed for the entire loan term.

Qualifying for a Loan

Are you in the market for a new home? That likely means you'll also need a mortgage, complete with a variety of terms, extensive paperwork, and long-term payments. Here's how you can make your money go further.

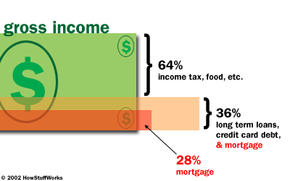

Are you in the market for a new home? That likely means you'll also need a mortgage, complete with a variety of terms, extensive paperwork, and long-term payments. Here's how you can make your money go further.Most lenders require a debt-to-income ratio of 28/36 to qualify for a mortgage (although this can vary depending on your down payment and loan type). This means no more than 28 percent of your gross monthly income can be allocated to housing costs, and no more than 36 percent can go toward your total monthly debt, which includes your mortgage. This debt includes long-term obligations such as car loans, student loans, credit cards, and other debts that take years to pay off.

Here’s an example to illustrate how the debt-to-income ratio works: Imagine you make $35,000 a year and you're considering a home with a $800 monthly mortgage. With the 28 percent housing limit, you could afford up to $816 in monthly payments, so the $800 mortgage is acceptable (it’s 27 percent of your gross income). However, if you also have a $200 car payment and a $115 student loan payment, you need to add those debts to the mortgage. This brings your total debt to $1,115, which is about 38 percent of your gross income. Your housing-to-debt ratio is now 27/38. Lenders usually use the lower figure (28 percent or $816), but you may need to put down a larger deposit or negotiate with the lender.

You must also consider what you can realistically afford. The lender will tell you what you qualify for based on your debt-to-income ratio, but this doesn’t account for your daily living expenses, such as food. What if you have an expensive hobby or financial goals that will require a lot of money in the future? The lender won’t know about this, so the $1,400 mortgage it says you qualify for today may not suit your actual budget in five years—especially if your income doesn’t increase much over time. Check out this calculator to get a better idea of how much house you can afford based on your current income.

In general, qualifying for a mortgage is more challenging today than it was during the housing boom, when nearly any motivated homebuyer could secure credit—even those who weren’t financially prepared. In the next section, we will explain the type of credit history and income capacity required to pass a lender's background check.

Mortgage Application

When applying for a loan, lenders will evaluate your employment and credit history to determine your ability to repay. They seek signs of stability, so any late payments within the last two years will be closely examined, particularly if they relate to rent or mortgage payments that were overdue by 30 days or more. They will also focus on any recent late credit card payments over the last six months.

Having a stable income is essential. Lenders typically prefer applicants who have been employed with the same employer for at least two years (or at least in the same industry). Additional sources of income such as part-time jobs, freelance work, overtime, bonuses, or self-employment earnings are also considered if they have been consistent for two years. If you don’t meet the required criteria, it doesn’t necessarily rule you out. It may just mean you need to talk to more lenders or accept a higher interest rate.

For several years now, the credit market has been restrictive. Mortgage lenders offer the best interest rates to those with high credit scores (ranging from 760 to 850) who can afford a substantial down payment (typically between 10 and 20 percent) [source: Esswein].

Here's a list of the typical documents you'll need when applying for a mortgage:

- Funds for the closing costs

- Completed sales contract signed by both the buyers and sellers

- Social Security numbers of all applicants

- Full address history for the past two years (including full name and address of landlords for the previous 24 months)

- Names, addresses, and income details from all employers over the past 24 months

- W-2 forms from the two years prior to your loan application

- Most recent pay stub showing year-to-date earnings

- Names, addresses, account numbers, monthly payments, and current balances for all loans and credit accounts

- Names, addresses, account numbers, and balances for all deposit accounts, such as checking, savings, stocks, and bonds

- The last three statements for deposit accounts, stocks, and bonds

- If you plan to include income from child support or alimony, provide copies of court records or canceled checks verifying receipt of payment.

For a more comprehensive list, visit here. Your lender and closing attorney will also inform you of the necessary paperwork and documents required at the loan closing. In the following section, we will explore the closing process in more detail.

What’s the distinction? Prequalification simply means you’ve shared your income, debt, and credit information with a lender, who then estimates how much you can afford to borrow.

Preapproval, on the other hand, takes it a step further by having the lender pull your credit report, assess your debt-to-income ratio, and perform a more thorough analysis of your financial situation.

In most cases, obtaining preapproval is more advantageous, as it prevents unexpected surprises when the lender checks your credit report – especially if you haven’t done so yourself beforehand.

What Are Closing Costs?

The full cost of a mortgage goes far beyond just the monthly payments. Once you’ve signed the sales contract, the closing process begins. This involves transferring the deed and title to the buyer, exchanging title insurance and financing documents, and submitting copies to the county recorder. Because the closing is a legal procedure, it typically involves an attorney or, at the very least, a third-party escrow holder. All of these steps and professionals incur fees, adding up to a significant sum known as the closing costs.

The amount you'll pay in closing costs can vary greatly depending on where you live. If you're in an area with higher taxes, for instance, your closing costs will likely be more expensive. Additionally, the fees charged by realtors, lenders, and attorneys differ based on the local market conditions. Generally, you can expect to pay between 3 and 6 percent of your total loan amount in closing costs. For example, if you have a $100,000 loan, your closing costs would be somewhere between $3,000 and $6,000.

It's always a good idea to shop around and negotiate your fees. According to the Real Estate Settlement Procedures Act, lenders are required to provide you with a good faith estimate of your closing costs within three days after receiving your application. As you'll see in the upcoming pages, there are numerous fees that may be negotiable, and you might be able to convince the lender to reduce or eliminate some of them. Additionally, you may also have the option to ask the seller to cover some of these closing costs.

Closing fees for a mortgage fall into three primary categories: the costs associated with obtaining the loan, the fees for transferring the property's ownership, and the taxes due to state and local governments.

In the following three pages, we'll break down every possible fee that could be included in the closing process when purchasing a home.

List of Closing Costs, Part I

Here are some of the significant fees that make up the closing costs:

- Processing fee -- This is the fee charged by the lender to cover the initial processing of the loan, including the application and credit report access. Typically, these charges range from $400 to $550. When comparing lenders, be mindful that sometimes the credit report fee may be listed separately from the processing fee.

- Appraisal fee -- The lender requires an appraisal to ensure the property's value matches the amount you're paying. This appraisal compares the property to similar homes in the same area. Independent appraisers typically charge $250 or more, depending on the property's price.

- Origination fee -- This fee is charged by the lender in addition to the application or processing fee, covering the additional work involved in preparing your mortgage. The origination fee could be either a flat rate or a percentage of the loan amount. If it's a percentage, it may function as a "discount point," which affects the tax implications and your overall costs. Be sure to confirm the details with your lender.

- Discount points -- By purchasing discount points, you reduce your mortgage's interest rate. One discount point equals 1% of the loan amount. You can pay for these points either when your loan is approved or at closing. Paying for points upfront could save you money in interest over the life of the loan. Some lenders may allow you to include the cost of points in your mortgage. These points may also be tax-deductible, so it's worth investigating.

- Document preparation fee -- This charge, which may be part of the application or attorney's fee, covers the preparation of all the necessary paperwork. It's typically a flat rate but can also be a percentage of the loan amount, usually under 1%.

List of Closing Costs, Part II

If you thought you were done with closing costs, think again:

- Attorney fees -- Both you and your lender will incur attorney fees. This fee covers the lawyer's work in drafting the necessary documents and preparing everything for closing. Your personal closing attorney represents your interests and may attend or facilitate the closing itself. The attorney collects all fees, transfers the deed, pays any outstanding taxes and utility bills, compensates themselves, covers other closing costs, and delivers the remaining funds to the seller. Fees for the attorney can range from $500 to $1,000 or more, depending on the property’s purchase price and the complexity of the sale.

- Home and pest inspections -- The lender will likely require a home inspection to ensure the property is structurally sound and free of pests like termites. If the property uses a well for water, you may also need a water test. In some areas, this test checks only the water quantity rather than its quality, but you may opt for your own water quality test if desired.

- Homeowner's and hazard insurance -- Most states require you to have these insurance policies in place, with the first year’s premium paid before closing. This insurance protects both your investment and the lender’s if the property is damaged or destroyed.

- Private mortgage insurance (PMI) -- If your down payment is less than 20% of the property value, PMI may be required. This insurance protects the lender if you default on your loan. The PMI premiums are typically added to your monthly mortgage payments and held in escrow along with taxes and homeowner's insurance. You'll continue paying PMI until your equity reaches 20% or 25%, or it may persist for the entire loan term. (See the next section for more details on PMI.)

- Surveys -- Many lenders will request an independent survey of the property to ensure that no changes, like new structures or encroachments, have been made since the last survey. These surveys generally cost between $250 and $500.

Can you believe there are still more closing costs to cover? You'll find them on the following page.

List of Closing Costs, Part III

Yes, there are still more costs to consider:

- Prepaid interest -- While your first payment is due in about six to eight weeks, interest starts accumulating as soon as you finalize the sale. The lender will calculate the interest owed for that partial month before your first official mortgage payment. A smart strategy is to close at the end of the month to minimize the prepaid interest.

- Deed recording fees -- Typically around $50, these fees are paid to the county clerk to record the deed and mortgage, as well as to update the property tax billing details.

- Title search fees -- A title search verifies the true ownership of the property. A title company meticulously reviews public records, including deeds, death records, court judgments, liens, contested wills, and other documents that might affect ownership rights. This is a critical step in closing your loan to ensure there are no claims against the property. The fees for title searches, which generally range from $300 to $600, are based on a percentage of the property's value.

- Title insurance -- If something is missed during the title search, title insurance will protect you from having to pay a mortgage on property you no longer legally own. Lenders often require title insurance to safeguard their investment, but you may want to purchase your own policy as well. This one-time premium covers the property for as long as you or your heirs own it, typically ranging from 0.2 to 0.5 percent of the loan amount for lender’s title insurance, and 0.3 to 0.6 percent for owner’s title insurance. Title insurance is one of the most affordable types of insurance. If the previous owner held the property for only a few years, you may be eligible for a discounted “re-issue” rate.

- Closing Taxes -- Depending on your state, you may be required to pay anywhere from three to eight months’ worth of taxes at closing, or you may place the funds in an escrow account for future payments. These taxes include prorated school taxes, municipal taxes, and other required taxes. In some cases, you might be able to split these taxes with the seller based on when they are due. For example, you would only pay taxes for the months following the closing date, while the seller would pay for the months before the closing.

Now that you've closed the sale, there may still be one more payment to make. Find out more on the next page.

Private Mortgage Insurance

Private mortgage insurance (PMI) is a useful tool for securing a mortgage when your down payment is less than 20 percent. This is especially beneficial for younger buyers who may not have had time to save up a large down payment but still want to enjoy the tax advantages and investment benefits of owning a home. PMI acts as insurance for the lender, covering the mortgage if you're unable to pay. Lenders consider PMI a necessary protection when the borrower has less equity in the home, as studies have shown a strong link between the borrower’s equity and the likelihood of default. The more equity in the home, the lower the chance of loan default.

Here’s an example of how it works: A couple with $10,000 in savings can buy a $50,000 home with a 20 percent down payment. Without the 20 percent down, that same $10,000 can serve as a 10 percent down payment on a $100,000 house or as a 5 percent down payment on a $200,000 home. However, if they choose the more expensive home, they'll need to pay for PMI. PMI costs are based on the loan amount. For a $100,000 loan with a 10 percent down payment, PMI could cost around $40 per month on average.

The Homeowners Protection Act of 1998 introduced rules for mortgages signed on or after July 29, 1999, mandating that PMI automatically ends once you reach 22 percent equity in the home, based on the original property value. Additionally, you can request PMI cancellation when your equity reaches 20 percent if the mortgage was signed after that date. However, if your mortgage was signed before that date, your lender is not required by law to cancel PMI once you hit the 20 percent equity mark, but you can still request it.

Certain exceptions may apply to this rule, such as if you've missed payments, if your loan is deemed high-risk, or if there are other liens on the property. Additionally, some states have laws that provide for earlier termination of PMI for mortgages signed before July 29, 1998.

Obtaining a mortgage has become significantly more difficult compared to the past. What has caused this change? We'll take a closer look at two prominent lenders and explore the factors that contributed to the housing crisis on the next page.

Fannie Mae and Freddie Mac

You might assume that mortgage lenders make most of their profits from interest, but that's not the case. Instead, they profit by selling mortgages on the secondary investment market. If lenders had to wait 30 years for full mortgage payments, they wouldn't have enough funds to continue issuing loans to new borrowers.

The largest buyers of mortgages in the secondary market are two government-backed entities: the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac). These organizations were created by Congress to help make home loans more accessible to individuals with low to moderate incomes.

For Freddie and Fannie (as they are commonly known) to purchase a mortgage, it must meet certain loan limits. For example, in 2010, the limit was set at $417,000 for a single-family home in standard areas, and up to $1.8 million in high-cost areas such as parts of Hawaii [source: Fannie Mae]. After acquiring these loans from lenders, Freddie and Fannie sell them as securities in the bond market, which provides lenders with the liquidity to offer more loans. Until 2006, the mortgage-backed securities (MBS) sold by Freddie and Fannie were considered solid investments. However, as mortgage defaults began to rise, the value of these securities plummeted. Due to heavy investments from major international banks in MBSs, the increasing default rates in the U.S. sent shockwaves through the global economy.

In 2008, Fannie Mae and Freddie Mac were taken over by the Federal Housing Finance Agency (FHFA), which became their "conservator" during this time of crisis. By June 2010, these mortgage giants had received a total of $145 billion in bailout funds from the U.S. Treasury to stabilize the credit market. Despite the government intervention, Fannie and Freddie remained publicly traded companies until their share prices fell below the necessary threshold, resulting in their removal from the New York Stock Exchange in 2010 [source: Reuters].

Despite their ongoing struggles, Fannie Mae and Freddie Mac continue to be the dominant buyers of mortgages in the secondary market and remain critical players in the U.S. credit system.

Next, we will delve into the topic of the "F" word -- foreclosure -- and explore how the government is stepping in to assist homeowners facing financial hardship and trying to prevent a credit disaster.

What Is Foreclosure?

Failure to make mortgage payments can result in the loss of your home. Foreclosure is the legal process through which a lender takes possession of a property and sells it to recover the outstanding debt.

The foreclosure crisis that began in 2008 was unprecedented in the U.S. That year alone, 2 million foreclosure cases were filed, and 1 million mortgage borrowers lost their homes [source: Palmeri]. Housing database experts at RealtyTrac predict that up to 4 million households could receive foreclosure notices in 2010 [source: Glink]. However, receiving a foreclosure notice does not automatically mean that you will lose your home.

To assist homeowners in avoiding the devastating effects of foreclosure, the federal government has implemented a variety of refinancing and loan modification programs. On the website MakingHomeAffordable.gov, borrowers can check their eligibility for one of four main programs:

- Home Affordable Refinancing -- This program allows homeowners whose properties are losing value rapidly to refinance their mortgages at lower rates. It's available to borrowers who have been up-to-date on payments.

- Home Affordable Modification -- If your monthly mortgage payments exceed 31 percent of your gross income and you've faced hardship such as job loss or medical expenses, the government can help you work out a new, affordable rate and payment plan with your lender.

- Second Lien Modification Program -- Many homeowners have second mortgages in addition to their first. This program offers incentives to lenders to forgive or reduce interest rates on second liens for qualifying borrowers.

- Home Affordable Foreclosure Alternatives -- If you don't qualify for refinancing or loan modification, you can still avoid the foreclosure mark on your credit. The government facilitates options like a short sale, where the home is sold for less than the mortgage, or a deed in lieu of foreclosure, where the borrower voluntarily transfers the property deed to the lender without owing the remaining mortgage balance. In both cases, the government provides up to $3,000 to help with relocation costs [source: MakingHomeAffordable.gov].

It's important to note that foreclosures are costly for lenders as well. The Mortgage Bankers Association reports that it costs more than $50,000 for lenders to process a single foreclosure claim [source: MBA]. Afterward, the bank must sell the property, often for much less than the original loan value.

A final word on foreclosures: in today's market, there's no need to pay for mortgage counseling or loan modification services. In fact, many of these services are fraudulent. The Department of Housing and Urban Development operates the HOPE Hotline (888-995-HOPE), a free resource for any homeowner seeking to avoid foreclosure.

If you're aiming to avoid foreclosure by lowering your mortgage payments, head over to the next page for valuable tips.

Ways to Save Money

Here are a few strategies that can help you save money on your mortgage:

- Negotiate -- The credit market is tough, but you still have the option to negotiate for better rates or even request fee waivers, especially for document preparation or attorney fees. Most other fees, aside from the essential loan costs like appraisal, title fees, processing, private mortgage insurance, credit report, and inspection fees, can be negotiated—particularly if you have a strong credit score.

- Choose the right mortgage type -- Picking the right type of mortgage can be challenging. A 30-year fixed-rate mortgage typically results in the highest total payments over time, but it's a popular choice due to its stability and security. Before deciding on an adjustable-rate mortgage or hybrid options like a 5/1 ARM, carefully calculate your ability to handle the rate reset in a year or five years. Also, consider that your income may not increase. The mortgage crisis taught us that a lower interest rate doesn’t always mean a better deal.

- Make additional payments -- Extra payments go directly towards your loan's principal, which reduces the loan balance faster compared to paying mostly interest. Making one extra payment each year could shorten the term of your mortgage by nearly 10 years. Use this calculator to find out how much you can save with extra payments.

- Biweekly payments -- Switching from monthly to biweekly payments helps shorten the life of your loan. This approach automatically adds an extra payment each year without it feeling like an additional burden. If you're paid every two weeks, this schedule aligns with your paychecks, allowing you to pay off a 30-year fixed mortgage in about 2 years.

- Avoid PMI -- Aim for at least a 20 percent down payment to avoid private mortgage insurance (PMI). If you're already paying PMI, keep track of your equity and eliminate PMI as soon as you reach 20 percent equity.

- Verify paying points will save you money -- In some cases, paying points may help you save, but it isn't always the best option. Quicken offers a points calculator that shows how points affect your interest rate and monthly payment. Ensure that the upfront cost of points will be recouped within the time frame you plan to stay in the home.