REITs provide the advantage of owning real estate without the responsibilities of being a landlord. Image courtesy of Manusapon kasosod / Getty Images

REITs provide the advantage of owning real estate without the responsibilities of being a landlord. Image courtesy of Manusapon kasosod / Getty ImagesInvesting in properties that generate passive income can significantly enhance your wealth. However, for many, particularly in the case of commercial properties, entering the real estate market can be financially prohibitive. But what if you could join forces with other small investors to collectively invest in large commercial properties? REITs (pronounced 'treats') make this possible.

REIT stands for real estate investment trust, sometimes referred to as "real estate stock." Essentially, REITs are companies that own and manage portfolios of real estate properties and mortgages. Anyone can purchase shares in a publicly listed REIT. They offer all the benefits of property ownership without the hassle or cost of being a landlord.

Investing in certain types of REITs also offers the key benefits of liquidity and diversification. Unlike owning physical real estate, these shares can be sold quickly and easily. Plus, by investing in a variety of properties instead of just one, you reduce your financial risk.

REITs were introduced in 1960 when Congress decided that small investors should have the opportunity to invest in large-scale, income-generating real estate. They concluded that the best way to achieve this was by adopting the investment model used in other industries — equity investment.

To qualify as a REIT, a company must distribute at least 90 percent of its taxable income to its shareholders each year. Most REITs distribute 100 percent of their taxable income. To maintain its status as a pass-through entity, a REIT deducts these dividends from its corporate taxable income. A pass-through entity doesn't pay corporate federal or state income tax — it passes on the tax responsibility to its shareholders. However, REITs cannot pass tax losses to investors.

From the 1880s to the 1930s, a similar rule existed that allowed investors to avoid double taxation — being taxed both at the corporate and individual levels — because trusts weren’t taxed at the corporate level if the income was distributed to beneficiaries. This was reversed in the 1930s, when passive investments were taxed at both the corporate level and as part of individual income tax. For 30 years, REIT supporters struggled to overturn this decision. Due to high demand for real estate funds, President Eisenhower signed the 1960 real estate investment trust tax provision, establishing REITs as pass-through entities.

A corporation must meet several additional criteria to qualify as a REIT and achieve pass-through entity status. These requirements include:

- Must be organized as a corporation, business trust, or similar entity

- Must be overseen by a board of directors or trustees

- Must offer shares that are fully transferable

- Must have a minimum of 100 shareholders

- Must pay out at least 90 percent of the REIT's taxable income in dividends

- Must ensure no more than 50 percent of shares are held by five or fewer individuals during the second half of each taxable year

- Must hold at least 75 percent of total investment assets in real estate

- Must limit its taxable REIT subsidiaries to no more than 20 percent of its total assets

- Must generate at least 75 percent of gross income from rent or mortgage interest

A REIT must ensure that at least 95 percent of its gross income comes from financial investments, meeting the 95-percent income test. These investments include rents, dividends, interest, and capital gains. Furthermore, at least 75 percent of its income must come from qualifying real estate sources, as defined by the 75-percent income test, such as rents from properties, profits from property sales, and income and gains from foreclosures.

Next, we will explore the different types of REITs.

Special thanks to Jason Caudill for his valuable assistance with this article.

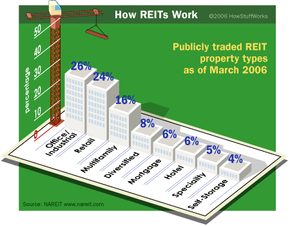

Categories of REITs

REITs belong to a highly diverse sector. There are various types of REITs, each consisting of different property categories and classifications.

Let's begin by looking at the three main categories of REITs: equity, mortgage, and hybrid.

Equity REITs (EREITs) invest in, own, and manage income-generating real estate such as residential complexes, shopping malls, and office spaces. Unlike traditional real estate developers, Equity REITs acquire or develop properties to maintain them as part of their portfolio rather than for resale. They are typically seen as a better long-term investment option due to their ability to generate income from both rental yields and capital gains through property sales.

Instead of acquiring properties, Mortgage REITs (MREITs) focus on lending money for mortgages to property owners or buying existing mortgages and mortgage-backed securities. Their primary income comes from the interest earned on these mortgage loans. Mortgage REITs are more sensitive to interest rate fluctuations compared to equity REITs since their earnings are driven by interest payments. Currently, nearly 40 mortgage REITs exist, with around 25 investing in residential-mortgage securities and the remainder in commercial mortgages. These REITs are considered a viable speculative investment when interest rates are expected to fall.

As the name suggests, Hybrid REITs combine elements of both equity and mortgage REITs. They own real estate properties and also provide loans to property owners and operators. Hybrid REITs generate revenue through a mix of rental income and interest earnings.

Certain REITs are set up for a single real estate project and have a defined lifespan. Once the term expires, the REIT is liquidated, and the returns are distributed to its shareholders.

There are also classifications based on whether a REIT is allowed to issue more shares. A Closed-end REIT can only issue shares to the public once, and it can issue additional shares — which may dilute the stock — only if current shareholders approve. In contrast, Open-ended REITs can issue new shares and redeem them at any point.

While some REITs take a broad approach by investing in a diverse range of property types across various locations, many others narrow their focus, either geographically or by property type. A REIT might focus on properties in a specific city, state, or region, or it could invest in a variety of locations but concentrate on specific types of properties, such as healthcare centers, residential complexes, or industrial sites.

The National Association of Real Estate Investment Trusts (NAREIT) categorizes REITs into three types based on how they are bought: private, publicly traded, and non-exchange traded.

Private REITs are not registered or listed with the Securities and Exchange Commission (SEC) and raise capital from individuals, trusts, or other entities that meet federal securities law requirements. Private REITs are typically subject to fewer regulations, apart from the guidelines needed to maintain their REIT status. There are nearly 800 private REITs operating in the United States.

There are approximately 200 publicly traded REITs that are registered with the SEC and listed on major stock exchanges like the New York Stock Exchange, NASDAQ, and the American Stock Exchange. These REITs are easy for investors to buy and sell, offering high liquidity due to their daily trading on the exchange. The total assets of these publicly traded REITs exceed $400 billion.

Around 20 non-exchange traded REITs are registered with the SEC, but they are not listed on public exchanges. Instead, they are marketed to investors by private sponsors, often targeting individuals who have experienced market losses and are seeking relative stability. In return for limited liquidity, these REIT sponsors emphasize the advantage of not needing to 'time the market.' They often highlight non-exchange traded REITs as being a stable option, providing returns that are better than bonds, certificates of deposit, money market funds, and similar financial instruments.

Now, let's explore how REITs operate.

REITs face restrictions on the types of services they can offer to tenants. Any additional services, such as housekeeping, must be provided through a Taxable REIT Subsidiary (TRS), a separate corporation in which the REIT holds an interest. TRSs are subject to standard corporate tax rates on their taxable income. The dividends the REIT receives from the TRS are included in the 95-percent income test. Additional rules for TRSs include limits on the amount of interest and rent they can pay to the parent REIT.

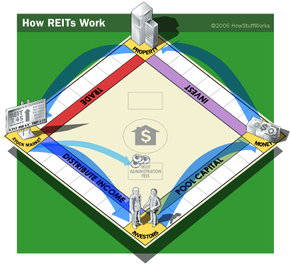

How REITs Operate

Due to the requirement that REITs distribute 90 percent of their taxable income to investors, they rely heavily on external funding as their primary capital source. Similar to other stock offerings, publicly traded REITs raise funds through an initial public offering (IPO). These funds are then used to purchase, develop, and manage real estate assets. The IPO operates like any other securities offering, except that instead of acquiring stock in a single company, the buyer owns a share of a managed portfolio of real estate. The income is generated from renting, leasing, or selling properties, and the proceeds are distributed regularly to REIT holders as a portion of the taxable income paid out.

A REIT's board of directors is chosen by its shareholders. These directors are typically respected real estate professionals and are responsible for selecting the REIT's investments and hiring the management team, which handles the day-to-day operations.

REITs generate income from renting space or selling property. The standard method of evaluating REIT earnings is called funds from operations (FFO). The National Association of Real Estate Investment Trusts (NAREIT) defines FFO as:

In simple terms, REITs adjust their net income (which is calculated based on generally accepted accounting principles [GAAP]) by adding or subtracting gains or losses related to depreciation, property sales, and unconsolidated partnerships and joint ventures. Essentially, FFO measures a REIT's operating cash flow generated by its properties, after accounting for administrative and financing expenses.

Under generally accepted accounting principles (GAAP), net income typically assumes that assets depreciate over time in a predictable manner. However, real estate often retains or even increases in value. Under GAAP, land remains at its historical cost, and buildings depreciate over time, ultimately reaching zero. Since a REIT's core business involves real estate, depreciation charges distort the company's true profitability. To address this issue, FFO was introduced to exclude depreciation costs from net income calculations.

While FFO provides a useful metric, it is not foolproof. Not all REITs calculate it strictly according to the NAREIT definition, and it does not account for expenses like maintenance, repairs, and other recurring capital expenditures. To get an accurate FFO, investors often need to review a company's quarterly reports and any supplemental disclosures.

Now, let's explore the essential factors to consider before investing in a REIT.

Similar to REITs, a tenant-in-common arrangement allows multiple investors to pool their resources for real estate investments. TICs are limited to investing in a single property and can have no more than 35 investors. According to tm1031exchange.com, "As a TIC owner, investors hold an undivided fractional interest in a property and share in the property's net income, tax shelters, and appreciation. Each TIC owner is given a separate property deed and title insurance for their share, which grants them the same rights of ownership as a sole owner."

Investing in REITs

Since many REITs are publicly listed, they provide investors with a powerful means for portfolio diversification and balancing. They also offer ongoing dividend income, while presenting the potential for long-term capital gains through appreciation in share price.

REITs hold an edge over other stock types due to their pass-through taxation. This structure enables REITs to generate higher profits to distribute as dividends compared to similarly sized corporations. As long as a REIT retains its tax-qualified status by distributing 90 percent of its net income to common shareholders, it remains exempt from federal income taxes. This tax advantage allows shareholders to receive a larger portion of the REIT’s earnings.

REIT investors benefit from dividend income and the potential for share value growth. Since REIT income often stems from commercial properties with long-term leases, these investments tend to offer a stable revenue stream. Additionally, REITs are somewhat shielded from inflation. Unlike bonds with fixed interest rates that lose value during inflationary periods, REITs with rental incomes can adjust in accordance with the rising cost of living, making them less susceptible to inflation-driven value loss.

Another advantage is the possibility of receiving a nontaxable return of capital. Depending on the REIT’s distribution policy and annual earnings, a portion of the dividend may qualify as a nontaxable return of capital. This means the investor doesn't owe taxes on that portion of the dividend when it is paid out, and it isn’t taxable until the stock is sold. As a result, taxes are deferred, and an investor's taxable income is reduced while holding the REIT stock, thus enhancing the after-tax dividend yield.

REITs do come with some drawbacks. Since their dividends bypass corporate taxation, they are not eligible for the 15 percent dividend tax rate established in 2003. As a result, investors generally pay taxes at their higher ordinary income tax rates, which can reach up to 35 percent. Furthermore, nontaxable distributions are taxed as capital gains (currently 15 percent for shares held longer than a year) when the shares are eventually sold.

Unfortunately, predicting which category of income a REIT will distribute in a given year (whether dividends or return of capital) is challenging for investors. However, according to NAREIT, the share of distributions that qualify for the lower tax rate has increased each year since 1998.

So, how should you choose a REIT? Even though REITs are inherently diversified, it's crucial to assess whether a specific REIT focuses on a single type of commercial property or a particular geographic region that might make it vulnerable to economic downturns. For this reason, many investors diversify by holding multiple REITs. Consider demographic factors like population growth, employment trends, and overall economic activity in the area or industry, as these will influence rent levels and occupancy rates, which in turn impact cash flow and dividends.

While it is commonly known that past performance is not a reliable indicator of future results, with REITs, you should pay attention to historical dividend payouts. Be cautious of unusually high yields. If there have been significant capital gain distributions, this could signal that income is being generated from nonrecurring events and may not persist. Ensure that the REIT isn’t selling properties to generate income, as this will reduce future rental income.

Evaluate your personal investment goals. REITs can offer both immediate income and long-term growth. Depending on your objectives, examine how the REIT's management and trustees are compensated. If their compensation is tied to the value of the REIT’s assets, management is typically focused on acquiring more properties for capital appreciation. If compensation is based on dividends or current earnings, the management may prioritize increasing the dividend yield, possibly at the expense of long-term growth.

Examine the REIT’s management team. Before investing, ensure that the management has a personal financial interest in the company, which should be disclosed in their most recent prospectus. Many 401(k) plans offer a REIT option.