If you own multiple credit cards, it’s likely you’ve received invitations to shift a balance to one of your other cards—usually the one you use less frequently. In an attempt to not be left behind, that card extends an offer of zero interest for 12, 15, or even 18 months, giving you an opportunity to pay down your balance without interest slowly inflating the total.

Sounds like a great deal, doesn’t it? However, there’s always an element of caution to consider.

This catch isn’t necessarily hidden or tricky, as credit card providers are upfront about any fees they may charge for transferring your balance from one card to another.

Let’s walk through an example to illustrate.

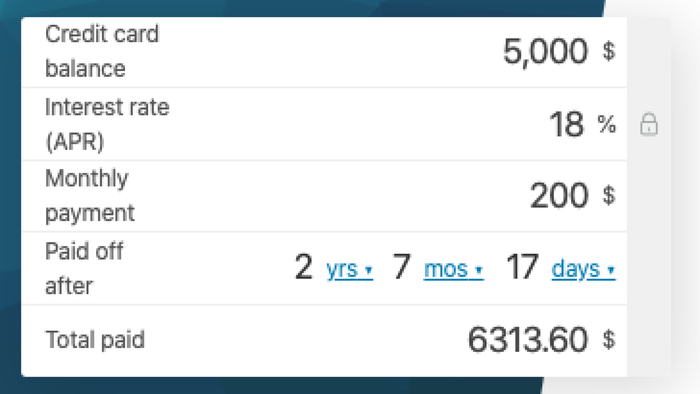

Imagine you have a credit card with a $5,000 balance and an 18% interest rate. You’re paying $200 monthly, but it feels like you’ll never escape the debt trap.

Now, suppose you receive an offer for a balance transfer to a card with zero interest for 15 months. If you accept, you’ll face a 5% upfront fee, which will be added to your overall balance.

Is it a smart move to accept?

How to compare credit card interest with balance transfer fees

A little bit of quick math is all it takes. And thanks to technology, it’s mostly automated, so you don’t even need to do it yourself. I recommend Omni Calculator’s debt payoff calculator, which helps you figure out how much you’ll end up paying when factoring in interest.

In our scenario, you’ll end up paying $1,313.60 in interest by the time you make your final credit card payment, almost three years down the line.

Now, back to your balance transfer offer. To figure out the fee, simply multiply your balance ($5,000) by the fee rate (5%, or 0.05). That gives you $250, which gets added to your balance immediately, bringing the total to $5,250.

It seems like a straightforward choice, right? If you stick with your current plan, you’ll pay over a thousand dollars in interest; if you transfer the balance, you’ll pay only a small portion of that.

Other factors to consider before transferring a balance

The math wasn’t too difficult, but there’s still more to think about.

Zero interest promotions aren’t permanent, and in our example, it lasts for 15 months.

If you continue paying your regular $200 per month, you won’t pay off your entire balance before the promo period ends. By then, you’ll have paid $3,000 of the $5,250 total. The remaining $2,250 will still accrue interest.

If your interest rate after the zero-interest period is higher than your current card, you might negate some of your savings. According to OmniCalculator, with a 25% interest rate on the remaining $2,250, and continuing with your $200 monthly payments, you’d pay $340.42 in interest.

In total, you’ll pay $590.42 in interest and balance transfer fees before becoming debt-free. That’s about half of what you’d pay if you kept the balance on your original card.

It’s still a significant savings, but unless you can speed up your debt repayment after the balance transfer, you’ll still face considerable interest charges. To pay off the full balance before the promotional period ends, you’d need to pay at least $350 per month.

Even if you can’t clear your entire balance during the promotional period, transferring your balance might still be worthwhile. The interest-free period could help you stabilize your finances or create a concrete plan for managing your debt. Just don’t expect the transfer to be a miracle solution—think of it as a temporary boost to make paying off your debt more manageable.