A common pitfall when budgeting is overcomplicating things before you truly grasp your financial situation. If you focus on too many small details early on, you might quickly become overwhelmed and give up altogether.

Though I’m a strong advocate of the 50/20/30 budget, it can sometimes feel too rigid, especially for someone just starting out with creating and sticking to a monthly budget.

This is where a simpler approach, focusing on just two main categories, can be extremely useful. The 60/40 budget gained popularity thanks to Richard Jenkins, the former editor-in-chief of MSN Money, who referred to it as “the 60% solution.”

The idea is to allocate 60% of your budget toward your necessary and fixed expenses. (Jenkins suggests calculating this based on your gross income, but I recommend using your after-tax income if you’re new to budgeting.)

The remaining 40% should cover everything else.

Jenkins adds a bit of complexity by dividing that 40% into four categories: retirement savings, long-term savings, short-term savings, and discretionary spending. This breakdown helps you avoid spending the majority of your ‘everything else’ money on unnecessary items like Jolly Ranchers, while only saving a small fraction.

However, consider those subcategories a more advanced budgeting approach. For now, we're focusing on the basics at the 101 level.

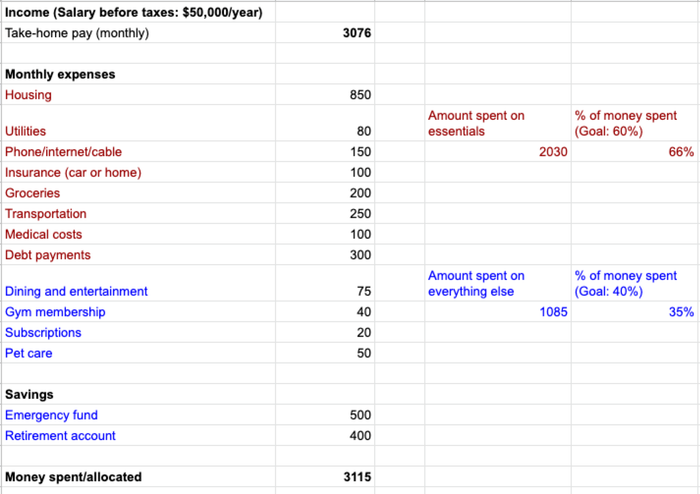

Now, let’s explore how the 60/40 budget works in practice by looking at the example I presented last week.

This hypothetical individual earns $50,000 annually before federal taxes and doesn’t pay any state income tax. They don’t make any pre-tax contributions to a 401(k) or similar benefit accounts, and their employer covers their healthcare premiums.

At first glance, things seem to be going well. This person is tackling their debt each month, saving regularly, and generally staying on track. However, they’re slightly over budget, with the percentage allocations adding up to 101% instead of the ideal 100%.

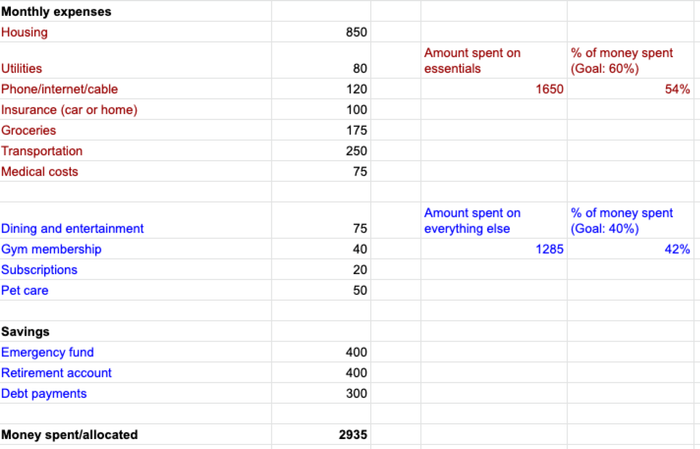

Time to make some adjustments. As seen in the previous budget example, our hypothetical person decided to trim some of their essential expenses to get the costs in line. During this process, they also moved their debt payment from essentials to ‘everything else’, since paying off debt now will help them focus more on savings in the future.

Now, we’re under budget, but the categories still feel a bit uneven—and they only add up to 96%. By cutting some expenses upfront, we’ve freed up some extra money to spend.

This is where you might notice that budgeting can actually give you more financial freedom, rather than restricting you. There’s an extra $141 each month, and this person is already saving well. Let’s allocate some of that extra for groceries, dining out, and entertainment.

And you know, while we’re at it, can we add “pet care” to the essentials list? I’m happy to cut back on my own spending when necessary, but I’m not about to skip feeding my cat.

The beauty of budgeting is that it’s ours to manage as we see fit. So, while we’re giving our hypothetical person some extra spending money, let’s make sure pet food is in the essentials category.

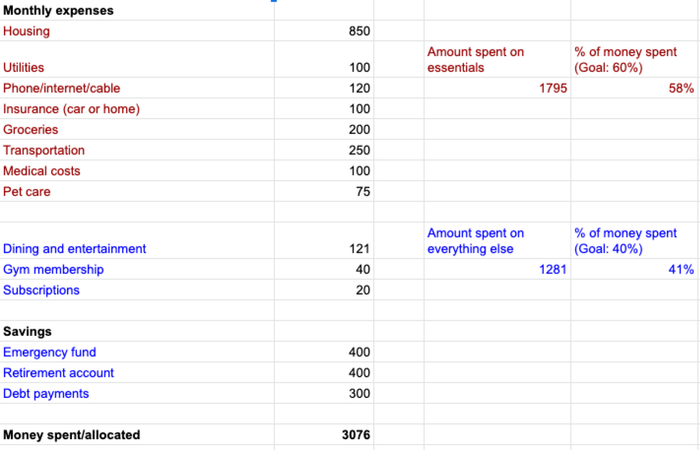

Look at that budget! The percentages are nearly perfect, and we managed to save a bit while still leaving room for fun and ensuring all the essentials are covered.

Let’s take one final look to refine it further. Jenkins suggests that the “fun stuff” should take up no more than 10% of the 40% bucket. Our $181 for dining, the gym, and subscriptions is just a bit over 14% of that 40%.

But let’s consider the bigger picture. Bills are paid, savings are on track, and it’s clear that this person isn’t living a lavish lifestyle. The numbers are looking solid to me.

What do you think? Do you prefer this 60/40 budgeting method over the 50/20/30 approach?