A common reason people avoid investing is because it feels overwhelming. However, investing now is one of the simplest ways to start building wealth, and it's something anyone can do. Follow these basic steps to create a straightforward investment portfolio that earns money for you effortlessly.

Investing Made Simple: Set It and (Mostly) Forget It

Many people associate investing with the daunting task of picking individual stocks, closely monitoring their daily fluctuations, and constantly buying and selling. But this is not the only way to invest.

While it may make for exciting television, and sure, you could hire a financial adviser to handle it for you, the reality is that most financial advisers fail to outperform the market.

So why spend a fortune on a financial adviser for something you can manage yourself? (Of course, if you're dealing with an exceptionally large sum and feel out of your depth, seeking help from a competent financial adviser can be a smart move.)

Most savvy investors aim to mirror the market, which historically tends to improve over time. Although past performance isn’t a guarantee of future results, it’s the best indicator we have—and on average, the stock market sees around a 7% annual return, which is pretty solid!

All you need to do is select a few funds that track the overall market's performance, then—generally speaking—leave them undisturbed for 20 or 30 years. It’s straightforward, and it’s something anyone can and should do. In fact, it’s one of the most effective ways to build wealth effortlessly in the long run.

This strategy is often referred to as 'buy and hold' or 'set it and forget it' investing because it demands little effort and you don’t have to constantly monitor your portfolio. You’ll want to check in once a year or so, but that requires minimal work. You can largely leave it alone—which is ideal for the average investor.

Step One: Open an Investment Account

If you don’t have access to an employer-sponsored 401(k), you’ll need to set up your own investment account to get started. For your first account, an Individual Retirement Account (IRA) is a great choice. Here's what you need to know:

Choose between a traditional IRA or a Roth IRA. If you're self-employed, a SEP-IRA might be right for you. Learn about the differences here.

Pick a reputable investment firm that offers IRA accounts, such as Vanguard or Fidelity. Many banks provide these accounts as well.

Set up your account. If you have an old 401(k), make sure you roll it over correctly into the new account.

Link your checking or savings account to the investment account and start purchasing index funds.

Once your account is set up, it's time to decide where to invest.

Step Two: Determine Your Asset Allocation

The market is more than just stocks. A well-rounded portfolio typically includes a variety of investment types. At a minimum, you’ll want a combination of stocks and bonds, with options both from the U.S. and international markets for each.

The right balance depends on factors like your age, risk tolerance, and investment objectives. A common guideline is:

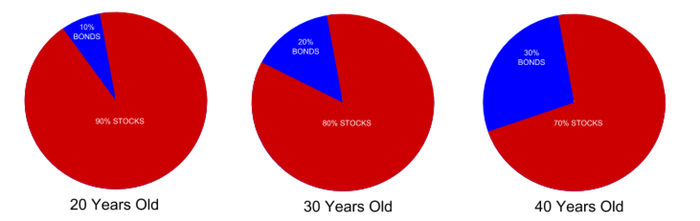

110 minus your age = the percentage of your portfolio that should be allocated to stocks

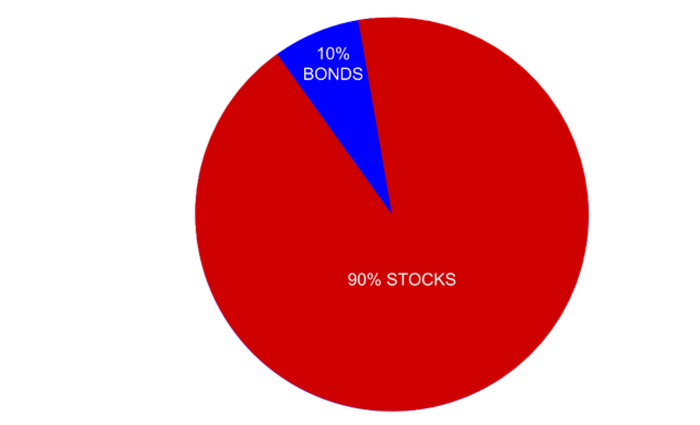

For example, if you’re 30, you’d allocate 80% of your portfolio to stocks (110 - 30 = 80), and the remaining 20% to lower-risk bonds. If you're more risk-averse, you might prefer putting 30% into bonds. This is a solid starting point, but feel free to adjust it based on your preferences.

As you age, it’s important to adjust your asset allocation. If you follow the 110 rule mentioned earlier, by the time you turn 40, you’ll want to shift towards more bonds—specifically, 20% in bonds instead of 10%. The goal is to reduce the volatility of your portfolio as you approach retirement.

If you’re struggling with deciding on your asset allocation, there are resources to assist you. Bankrate offers an asset allocation calculator, or you could use a comprehensive tool like Personal Capital.

While stocks and bonds are not the only types of assets you can hold, we’ll start with these for simplicity.

Step Two: Select Your Index Funds

A great way to begin investing is by choosing a few index funds. An index fund pools together stocks or bonds, aiming to reflect a specific segment of the market.

Index funds are ideal because they typically have very low fees (or expense ratios). Combined with their goal of tracking the market, they tend to offer better long-term returns. If you’re curious about index funds and how they compare to other types of funds, you can dive deeper into this article.

With so many index funds available, it’s important to understand how to choose the right ones for your needs.

The Perfect Approach: Choose a 'Lazy Portfolio'

You could build a complex portfolio with multiple funds, but you really only need two or three to begin. There's no need to start from scratch and pick funds randomly either—one of the simplest ways to begin is by using a 'lazy portfolio.'

Consider it a 'starter pack' for index funds: a few basic funds that will provide you with a simple, well-rounded portfolio that tracks the market across different sectors.

Let’s go over some simple options.

In an IRA or a regular investment account, you can choose from any index funds you prefer. So, let's discuss this ideal setup. (If you’re working with a 401(k) that offers limited options, don’t worry, we’ll cover that later.)

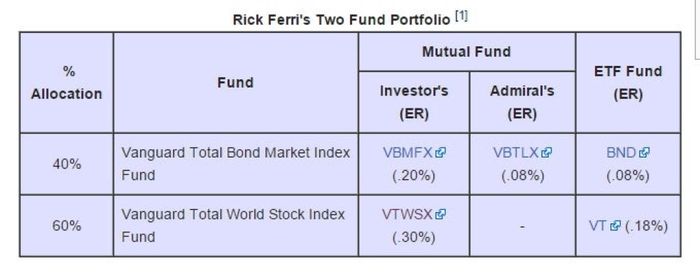

Let’s say you’re aiming for an asset allocation of 90% stocks and 10% bonds. The simplest portfolio would be Rick Ferri's two-fund portfolio, which uses two popular Vanguard funds:

The total world stock index fund is designed to replicate the performance of the global stock market with a single fund. The bond fund does the same thing. Naturally, you’d adjust the ratio of bonds to stocks to suit your asset allocation (for example, 90% stocks and 10% bonds).

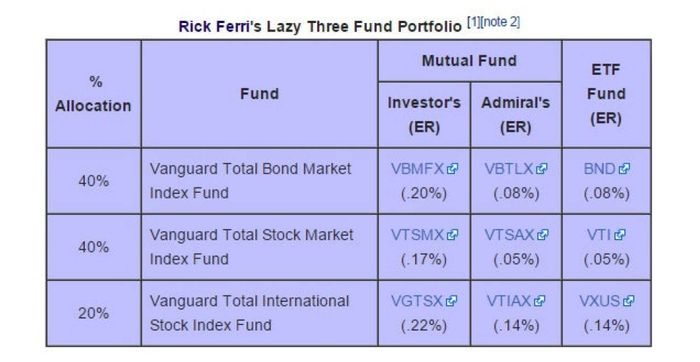

The total world stock index fund is made up of approximately 50% U.S. stocks and 50% international stocks. If you’d like to modify this balance—say, investing less than 50% in international stocks—you could opt for a three-fund portfolio like this one:

Once again, adjust the proportions to match your desired allocation. (For instance, this portfolio is made up of 60% stocks and 40% bonds).

Remember, some index funds may have minimum investment requirements. This means you may need to invest at least $3,000 to purchase any shares of the fund, for example.

As you contribute more to your account, you may qualify for funds with lower expense ratios, such as Vanguard’s Admiral Shares or Fidelity’s Advantage Class.

That’s all you need to get started. Pick two or three funds with low expense ratios (preferably under 0.25%, though the lower, the better) and ensure they align with your desired asset allocation. While there are other investment options—such as real estate or precious metals—you don’t need a flawless portfolio at the outset. The key is to take action, and this is a solid foundation.

The less-than-ideal scenario: If you have a limiting 401(k)

The previous option works great for a basic investment account or an IRA, where you have a wide range of options. However, if you have a 401(k) through your employer or a similar retirement plan like a 403(b), your fund choices may be more restricted. Some may be fine, while others might not be ideal—but in any case, your 401(k) is still worth using for the tax advantages.

Let’s imagine you have a 401(k) with some good choices, but none that are as straightforward as the total stock and bond market funds we discussed. For instance, you may have the total bond fund, but lack the total stock market fund.

You can replicate the total stock market by using other available options. For example, you could combine these funds:

An S&P 500 fund (which includes 500 of the largest companies in the U.S.)

A mid-cap index fund (which covers medium-sized companies, making up for those not found in the S&P 500)

A small-cap index fund (which includes smaller companies, filling in the gap for the smaller companies excluded from the S&P 500)

Naturally, this strategy works only if your 401(k) provides those fund options. It doesn’t need to be an exact match; the key is hitting the right proportions.

If you're fortunate, your 401(k) might offer enough options to help you get close to your ideal asset allocation this way. Just don’t forget to check each fund’s net expense ratio to ensure it’s not too high!

The crappy scenario: If your 401(k) has a bad selection of expensive funds

Now, imagine your 401(k) doesn’t offer the right mix of funds to complete your ideal asset allocation. Or, even worse, what if your plan only offers funds with expense ratios over 1%? What are your options then?

As we’ve discussed before, there are many benefits to having both a 401(k) and an IRA, and this approach is particularly helpful if your 401(k) lacks flexibility. If you choose to have both, here’s the optimal way to invest in each:

Contribute just enough to your 401(k) to capture your employer's match.

Direct any extra savings to an IRA, which offers greater flexibility.

If you still have funds left after reaching the IRA contribution limit (check the limits here), feel free to add the rest to your 401(k).

If you manage to max out both your 401(k) and IRA (impressive!), you can then open a standard taxable investment account. These accounts are also useful for medium-term goals, as retirement accounts restrict withdrawals until later in life.

You can do this regardless of how good or bad your 401(k) options are. However, if your 401(k) is lacking, here’s the trick: Use it for the lowest-cost fund(s) with solid performance over the past decade or so, and then use your IRA to fill in the gaps with the low-cost index funds that complete your ideal asset allocation. Just be sure that the total investments match the allocation percentages you determined in step one.

Step three: Contribute consistently and rebalance each year

Now that you've selected your funds and nailed down your asset allocation—great job! The next step is to set up automatic contributions, ideally tied to when you receive your monthly paycheck, so that money is always flowing into your investment account. If you have a 401(k), this is even more crucial, as those contributions are tax-deferred! This approach will help your wealth grow steadily over time. Treat your savings like an ongoing expense, and you’ll avoid overspending.

After that, forget about it.

Seriously. Just walk away. Don’t check your investments every few days, don’t stress over market fluctuations, and definitely don’t micromanage. Remember, you're in this for the long haul—market dips and peaks are less important than the overall growth over the years.

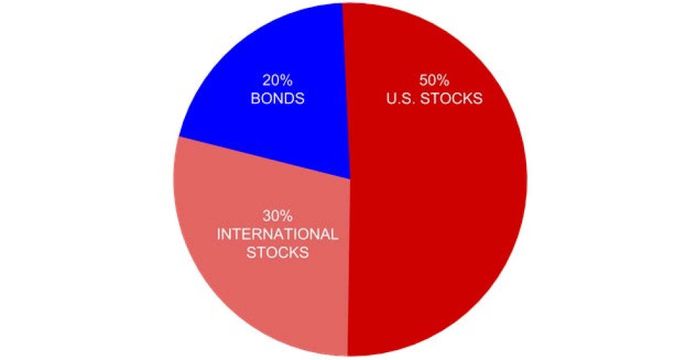

However, you’ll want to review your portfolio once a year or so and ‘rebalance.’ What does this mean? Let’s assume you're holding 20% bonds, 50% U.S. stocks, and 30% international stocks, like this:

Now, imagine that international markets perform exceptionally well one year, while U.S. stocks dip slightly. This means you’ll have made more gains in your international stocks than in the other areas, and by the end of the year, your portfolio might look something like this:

To get your portfolio back in line with your initial asset allocation, you’ll need to rebalance. Stop contributing to the international stock fund(s) and redirect that money into the bond and U.S. stock fund(s). After a few months, things should even out, and you can resume your original contribution amounts. (Alternatively, you could sell some of your international stocks and invest that money into bonds and U.S. stocks, though this may incur extra fees).

A much simpler alternative to all of the above: Target-date funds

If all of this feels a bit overwhelming, there’s an easier option: Invest everything into a target-date fund.

Target-date funds, sometimes known as lifecycle funds, are designed to simplify the process by dividing your money across stocks, bonds, and other assets. It adjusts and rebalances automatically over time, shifting more toward bonds as you approach retirement. Sounds convenient, right?

The best part? You just pick the fund with the target year that matches your retirement plans, deposit all your money into it, and let it grow. If you’re planning to retire in 2055, go with the 2055 target-date fund from Vanguard, Fidelity, or your chosen provider. If 2050 is your target, choose that one instead.

You can also select a different target date fund based on your risk tolerance. If you want to take a more cautious approach, you might opt for one with an earlier retirement date, which will allocate more to bonds sooner. Conversely, if you're willing to take on more risk, you could choose one with a later date. Just make sure to read the prospectus of the target-date fund to understand how its asset allocation evolves over time. Some may be more aggressive or conservative than you anticipate.

Similarly, if you’re setting up an IRA or a taxable investment account, consider using a robo-advisor, which will manage your investments for you based on your specific goals.

Why go through the hassle of picking your own index funds when convenient options like target-date funds are available? While target-date funds are fantastic, they do tend to come with slightly higher fees. The fees vary between funds, so it's a good idea to use an expense-ratio calculator like this one to determine how it will affect your long-term returns.

For instance, let’s say you’ve assembled your own portfolio with Vanguard funds that have an average expense ratio of 0.05%. In comparison, Vanguard’s target-date fund charges 0.18%. While still low by many standards, that’s 0.13% higher than the self-managed approach.

If you consistently max out your 401(k) for 30 years, that 0.13% difference could result in $50,000 more in your account—just for putting in a bit more effort with the DIY route. That’s a decent sum for minimal work. And since Vanguard’s target-date funds are relatively inexpensive, this is a best-case scenario. If your 401(k) isn’t ideal, the difference could be much more than $50,000.

We’re not here to knock target-date funds. They’re great for individuals who don’t want to put in much effort and might otherwise skip investing altogether. If that sounds like you, go ahead and invest all your money in a target-date fund and let it grow! However, building your own portfolio gives you more control and can lead to lower fees, which can add up over time—provided you put in the effort to do your research.

It might seem overwhelming at first, but once you push past the initial learning curve, you’ll have a simple, set-it-and-forget-it portfolio that will start working for you. There are certainly other investment strategies out there, but this is one of the most popular approaches and is a great starting point for beginners. And when it comes to investing, the most important thing is to start now.