Up to this point, we’ve discussed the frameworks for two budgeting strategies that concentrate on broad categories and adjusting your distribution to each: The 50/20/30 budget and the 60/40 budget.

While these approaches allow flexibility to fine-tune your expenses and savings, they might not work for everyone depending on individual financial situations. For example, if you live in an area with high living costs, keeping your housing and essentials within a 50-60% range could be unrealistic. Or, if you're living paycheck-to-paycheck, saving a considerable portion of your income might not be feasible just yet.

To learn more about managing debt, check out the video below:

This is where the zero-based budget comes into play. Your objective is to align your income and expenses perfectly each month, leaving you with zero dollars remaining.

This doesn’t mean you spend everything—it simply means you assign every dollar a specific purpose. By knowing that every dollar is being directed toward a category with intention, you can stay on track to achieve your financial goals, whether your income is limited or more generous.

It also doesn’t require you to deplete your bank account to zero each month. You may decide to use a portion of your emergency savings to maintain a $100-200 buffer in your checking account, or perhaps your bill due dates naturally prevent you from running your balance too low. Customize this aspect to suit your needs—the key is ensuring that your money is precisely allocated, not that it leaves your account on a specific schedule.

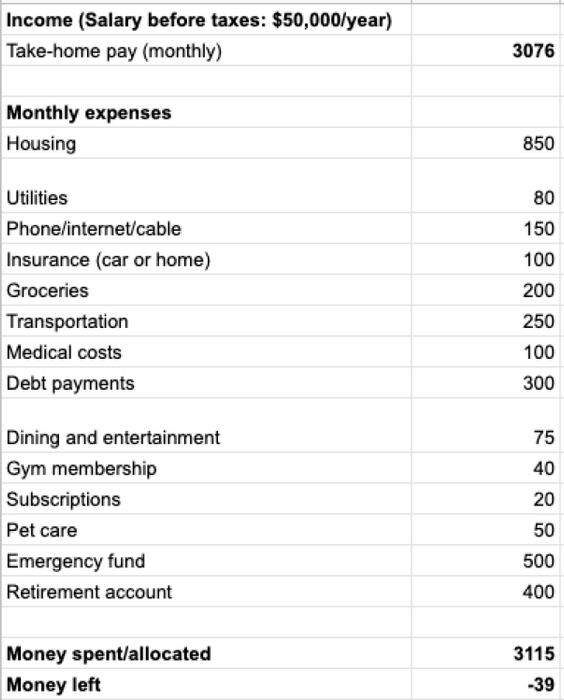

Let’s take a closer look at how this budget works in practice. Using the same example from the two previous budgeting methods, let’s say this hypothetical person earns $50,000 annually before federal taxes and isn’t subject to state income tax. They don’t contribute to a 401(k) or other pre-tax benefit accounts. Their employer covers their healthcare premiums.

Take a look at how straightforward this breakdown is. The key figure here is the one at the bottom: The remaining amount after all expenses (including debt payments and savings goals). As shown, we're exceeding our budget and are short by $39 for the month. It’s time to make adjustments.

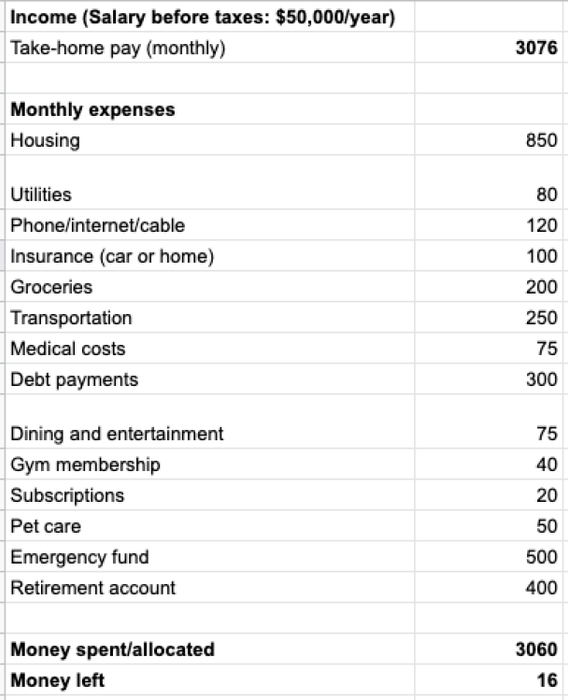

Following the same steps as before, you contact your internet provider to lower your rate and decide to set aside less for prescriptions and copays since you typically don’t spend the full amount each month.

Not bad! We have $16 remaining. But even though it’s tempting to keep that small surplus at the bottom of the sheet, we need to bring everything to exactly $0.

That $16 could be placed back into the 'medical costs' category with the idea of rolling it into savings if it’s not spent by the end of the month. Alternatively, you could set that $16 aside for savings. I’ll have our Hypothetical Person apply it toward their monthly debt payment.

Ta-da! There’s that perfect zero. It feels great to have everything squared away, right?

Naturally, this 'final' budget is far from final. Your expenses can vary each month, which means you may need to adjust how much you contribute to savings—or how much you take out. You may also find that your categories need to be rearranged as your priorities change.

And that’s perfectly fine. The key takeaway when using a zero-based budget is to assign every dollar a purpose and ensure it’s working for you.