When you start budgeting, you're often advised to prioritize saving early and regularly.

You may have heard the advice, 'Treat your savings like a bill you must pay yourself.' If you rely on 'extra' funds or the end of the month to save, it's easy to forget or overlook. Instead, you'll probably find yourself ordering pizza or making other spontaneous decisions.

If saving off the top of your income feels like a challenge, the 80/20 budget might be a perfect fit. Known also as the 'pay yourself first' budget or the anti-budget, its approach simplifies things: focus solely on saving (20% of your income). The remaining 80% is for everything else—your essentials, fun spending, and any other expenses.

This budget method works well for certain groups of people. For instance, it’s ideal for those who may not earn a lot of money or are just beginning to save. Essentially, this approach says, 'Your expenses might not be perfect, but if saving is a priority, the rest will fall into place.'

It’s also great for individuals who feel secure with their income—perhaps a little too comfortable. Whether it’s your first job post-college, you’ve recently cleared significant debt, or received a major pay raise, it's easy to slip into the habit of indulging yourself, letting lifestyle inflation erode your non-essential funds.

Let’s dive into how this works in practice, shall we?

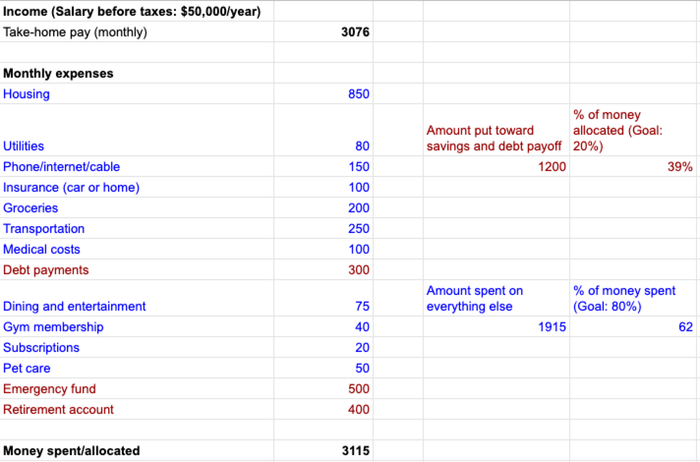

Using the same example from the previous budgeting methods (the 50/20/30 budget, the 60/40 budget, and the zero-based budget), imagine a person earning $50,000 annually before federal taxes and exempt from state income tax. They don’t contribute to a 401(k) or other retirement plan before taxes. Additionally, their healthcare premiums are fully covered by their employer.

Everything is looking pretty solid here. The main issue is that they’ve exceeded their budget by a few dollars, but it’s nothing that can’t be adjusted.

So Hypothetical Person renegotiates their phone bill, skips one half-gallon of ice cream at the store each month, and reduces their savings by four dollars, aligning the income and expenses perfectly.

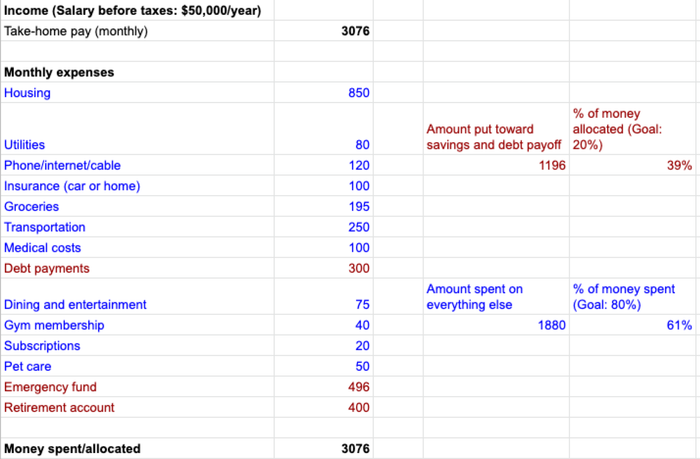

Now that we’re no longer spending beyond our means, you’re probably thinking, 'Lisa, this looks like a 60/40 budget.'

And, well, you’re not far off! But I want you to imagine the future for a moment.

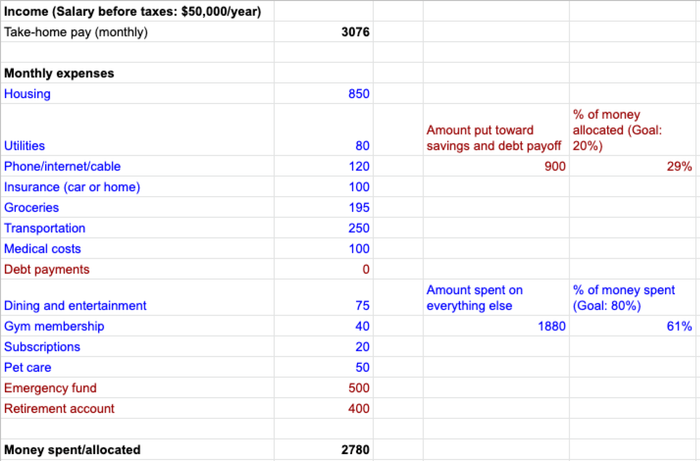

This person isn’t going to stay in debt forever, assuming things go their way. Let’s say our example pays off their debt, reducing the amount they put toward both savings and debt down to $900 per month, instead of around $1200. This brings their savings portion down to 29%.

As things progress, our Hypothetical Person may find themselves with a well-established emergency fund and decide to redirect those funds elsewhere—whether it’s into another savings plan or towards daily expenses.

In the future, our example might discover they want to save a large portion of their income. As a result, they may let go of the 80/20 rule and opt for a budgeting method that better aligns with their goals or way of life.

At the end of the day, it’s all about the journey. The ‘perfect’ budgeting method probably won’t come on your first attempt. However, if you stay open to testing different approaches, you’ll find one that suits your current needs—and know when it’s time to reassess and try something new.