There are many ways to approach budgeting, each offering a unique strategy to handle your finances. However, while most guides introduce these strategies or highlight the key areas to consider, they don’t always make it clear how your budget will actually take shape in practice.

This month, I’ll go over several popular budgeting methods you may already be familiar with and demonstrate how they actually work in real life (on a Google sheet, of course).

Let’s start with the 50/20/30 method. Here’s a breakdown of the main components:

50% of your monthly budget is allocated to essential expenses, such as housing, transportation, food, and utilities.

20% of your monthly budget is dedicated to savings, including debt repayments, since reducing debt contributes to building savings over time.

30% of your monthly budget is for discretionary spending, covering things like your gym membership, travel, dining, and gifts.

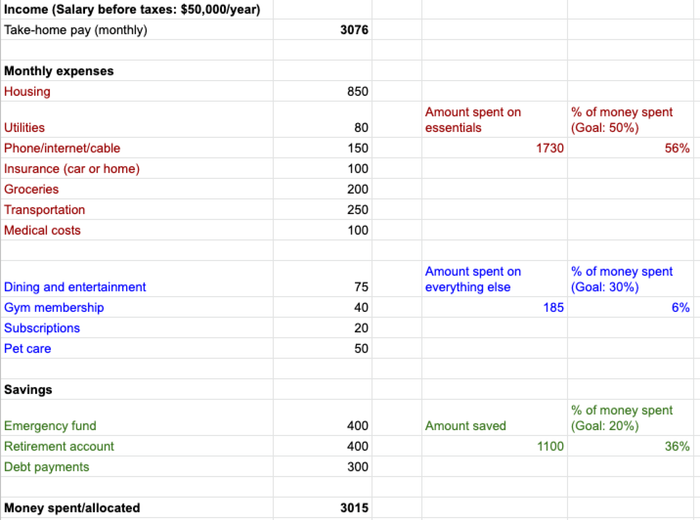

Let’s examine a sample budget to illustrate how the 50/20/30 rule looks when you first set it up. You can either use a simple spreadsheet or a budgeting app to track your percentages. I’ll be using the same salary and expenses in each example this month.

In this scenario, the individual earns $50,000 annually before federal taxes, without state income tax. They don’t make pre-tax contributions to retirement accounts like a 401(k), and their employer covers healthcare premiums. (Again, this is a simplified example for the sake of calculations.)

At first glance, it’s clear this budget doesn’t balance. You’ll notice the percentages don’t quite add up, and the expenses exceed the monthly take-home pay. Nearly 70% of the budget is allocated to essentials, leaving little room for discretionary spending unless they’re constantly at the gym.

It's time to make some adjustments.

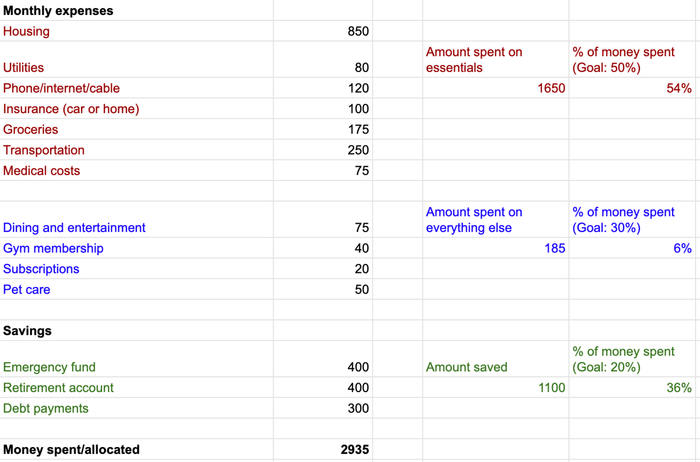

Your monthly debt payment is currently listed under “essentials,” but it actually belongs in the “savings” category. I know it might seem counterintuitive, but stay with me. The 20% savings portion is often considered “financial goals,” and reducing debt is a key part of that. The best way to build a strong savings cushion is by eliminating debt first, freeing up more of your income in the long run.

So, we'll reallocate that debt payment to the savings category and slightly lower the emergency fund contribution to keep the budget balanced. Once the debt is cleared, you can start increasing your savings again.

We’re in a better place now, but there are still some tweaks to make. You might be fine with sticking to a tight budget for “everything else” if it helps you save more and pay off debt faster. But perhaps adjusting your essentials can bring more balance to the whole budget.

You reach out to your internet provider for a discount. You use coupons and cashback apps to shave $25 off your grocery bill each month. You budget $100 for medical expenses but typically only spend $60 on prescriptions and copays, so you save a little there, confident in your emergency fund.

That’s $80 saved. What kind of impact does that have? Let’s find out.

Not bad at all. This person still follows a very tight budget but has managed to prioritize savings and debt repayment while trimming expenses slightly to stay closer to the 50% essentials target. The total doesn’t add up to 100% because they’re under budget. They have $141 left over each month that could go toward anything they like—maybe even a night out!

If you experiment with this budget method and don’t hit the 50/20/30 split exactly, don’t worry. It takes time to find the right balance that works for you. Depending on your location and income, like living in an expensive city where housing takes a large portion of your budget, the exact numbers might not always align. But by visualizing your expenses with this approach, you can better understand how to adjust your spending to fit your needs.

And remember—I’ll say this again and again—your budget is a living document. You’ll need to make changes as your life circumstances shift or unexpected costs come up. So, don’t just set it and forget it.

Do you use the 50/20/30 budget? How do you manage and track yours? Share your strategies and experiences in the comments.