You likely have investments in a 401(k) or IRA, but may find it difficult to understand how to interpret your investment reports. These statements are full of complex numbers and terminology. Here's a straightforward guide to help you make sense of them.

Naturally, the format of your statements will differ based on the company managing your retirement account and the intricacy of your investments. The sections we highlight might be located in different areas of your statement or may have slightly different names. Nevertheless, they generally provide the same kind of information. To simplify things, we’ve divided the statement into summary, details, and performance sections.

Retirement Account Overview

Typically, your investment account summary provides a few key details:

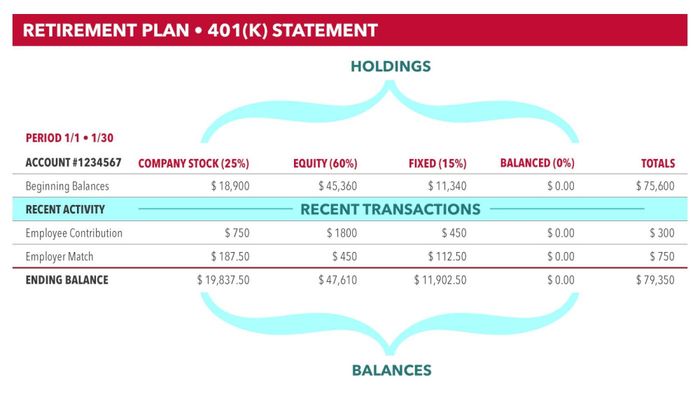

Your current account balances

The assets you’re invested in (referred to as 'holdings')

A snapshot of your recent transactions

The image above visually highlights these categories in blue. Let’s explore them further for a clearer understanding.

Account Balances: This is pretty simple. It shows the actual amount in your account after all transactions. Here are some additional terms and information that might appear related to your balance.

Return: This indicates how much your investments have gained or lost in value, typically shown as a percentage based on performance.

Beginning Balance: This reflects the starting balance for the statement cycle (often the first of the month). Depending on your transactions and return, your beginning and ending balances might differ. Sometimes, balances are shown over time in a chart, with the starting balance coinciding with the chart’s beginning date.

Taxable vs. Nontaxable Income: If your investments generate interest, it may be labeled as taxable or nontaxable income on your statement, depending on the type of account you have. For more details on how your investments are taxed, check out our post on the subject.

Recent Transactions: This section is quite straightforward. It provides a summary of any transactions that have taken place since your previous statement. In the following section, we'll discuss the typical types of transactions associated with an investment account. The summary may cover the basics such as:

Purchases: Any incoming funds to your account, such as contributions, employer contributions, or rollovers.

Withdrawals: Any money you've withdrawn from your account, like a loan withdrawal.

Your Investments, or Holdings: Your holdings are the specific assets you're invested in—stocks, bonds, company stock, mutual funds, and more. These holdings might be listed with their ticker symbols on your statement or presented as a general percentage. Here are a few terms related to your holdings.

Asset Class: These are the broad categories of investments you're holding. Some common ones include equities (stocks), fixed-income (bonds), and cash equivalents (money market). Your statement may show the percentage of your investment in each class.

Asset Mix/Asset Allocation: Your asset mix reflects the general types of investments you're holding. These may be represented as percentages or as a pie chart. If you're unsure how to allocate your assets, we offer a beginner's guide to get you started.

Account Details

After covering the basics, your statement should provide more in-depth information. Your account details will typically include the following:

A record of transactions since your last statement

A breakdown of your individual investments

The current value of those investments

Let's dive deeper into each of these sections to understand how this information may be presented in your statement.

Your Individual Investments and Their Value: While your statement's summary showed an overview of your holdings, the rest of the document should provide more precise details about what those holdings are, beyond just their category. Additionally, you should be able to see the value of each individual investment. Typically, this section will include:

Price: This represents the value of your particular investment type. Since prices fluctuate, your statement will show the price on a specific date.

Share: This refers to the unit of ownership. Your statement might list how many shares you own in each asset, as well as the number of shares involved in a transaction. It may also display the share price on specific transaction dates.

Price Change: This shows how much your investments have increased or decreased in value, typically based on the opening and closing dates of the statement.

Volume: Volume represents the number of shares traded in a transaction.

If you’re uncertain about the investments listed on your statement, a quick Google search using the ticker symbol will help you understand how your funds are being allocated, according to Mabel Nunez, founder of stock market education company Girl$ on the Money.

Additionally, remember that your investment brokerage is a valuable resource, especially if you're dealing with mutual funds rather than individual stocks. For example, if your statements come from Vanguard, be sure to use their platform for fund research, as many financial portals provide fund details, but the parent company of the fund offers the most accurate information.

Transaction History: Various transaction types may appear on your investment account. Here are a few of the most common:

Contributions: Money deposited into your account, potentially automatically withdrawn from your paycheck or contributed by your employer. Ideally, you have both.

Dividends: Occasionally, companies distribute a portion of their earnings back to shareholders in the form of dividends.

Gains and Losses: Similar to your return, this reflects how much a specific investment has gained or lost in value. This may be shown as a percentage. If you buy or sell the investment, it's classified as a 'realized' gain or loss.

Exchange In and Exchange Out: If your investment plan is managed by a firm, they may choose to exchange one fund for another. This transaction will be noted in your statement.

Account Fees: Your statement may highlight any fees linked to your account or specific funds. These fees may be explicitly labeled as fees or referred to as an expense ratio, or sometimes both. Either way, they reflect the costs associated with managing your portfolio. If this information isn't included in your statement, you can often find it by checking your account online or by contacting your investment broker.

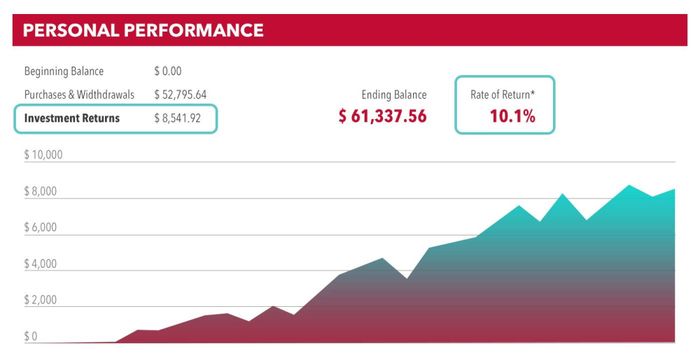

Portfolio Performance

Once your account details are presented, your statement may provide a basic analysis of your investment performance. While much of this information is included in the detailed section, some statements summarize it at the end to give you a clear picture of how you’re doing overall. Typically, your performance summary will cover:

Rate of Return: This indicates how much your investments have gained or lost in value, factoring in dividends, gains, and losses. It's usually shown as a percentage.

Investment Returns: This reflects the total amount you've earned from your investments, based on dividends, gains, and losses, displayed as a dollar amount.

Comparison: Sometimes, your portfolio's performance is compared to the market. The investment firm might show how your rate of return or stock style measures up against the broader market. (If your portfolio is underperforming, it might be worth reconsidering your investment allocation.)

It's crucial to stay on top of your investments, but avoid getting too caught up in the market's fluctuations when you're focused on long-term growth. 'Review, don’t react,' advises Molly Ward, a CFP and financial advisor at AXA Advisors. 'If the account value drops, remember that ups and downs are part of the process. If there's a sharp change from the previous month, that's normal. Stay calm if you notice a significant drop.'

Nunez concurs, recommending that investors assess their growth on a quarterly or yearly basis instead of monthly. 'Reviewing your statements every month doesn’t give you much insight, as it's a very brief period in terms of the stock market. Pay attention to long-term trends and how your investments have grown over the year,' she suggests.

These statements can be especially tricky due to the varying terminology and reporting methods used by different investment firms. However, the main goal is to understand what you're invested in, track the performance of those investments, and monitor how your balance evolves over time.