After several years of nearly zero interest rates on certificates of deposit post-recession, recent times have seen substantial growth. This is partly due to the federal funds rate, which the Federal Reserve has increased nine times between December 2015 and December 2018.

The national average rate for one-year CDs surged from 0.33% APY in January 2017 to 1.01% in May 2019, as per Bankrate data. Even higher rates, typically ranging between 3% and 3.15%, are often available from major banks, as noted in Bankrate’s rate roundup, though these higher rates may sometimes be linked to deposit minimums. However, these elevated rates might not last long.

No rate hikes by the Federal Reserve are expected for 2019. Some analysts predict the Fed may even lower rates this year, according to the Wall Street Journal; however, the Fed's stance suggests that rate cuts are unlikely.

Is now the right moment to lock in a CD before these top rates disappear?

Let’s start with a quick refresher on CDs: a certificate of deposit is essentially a short-term loan you offer to a bank. In exchange for allowing the bank to hold your money for a set period, whether that’s six months, a year, or longer, they pay you interest. There are also no-penalty CDs that let you withdraw your funds at any time, but these often come with varying interest rates and minimum deposit requirements.

CDs are often recommended for short-term savings objectives. If you’re saving for a large purchase a few years down the line, parking your money in an FDIC-insured CD can help prevent spending temptations while earning a bit of interest.

If earning a little extra money from interest sounds appealing, and a CD was already on your list of potential options, now might be a great time to secure one. However, if you’d prefer to keep your cash on hand, you’ll likely still find decent rates available over the next year or so.

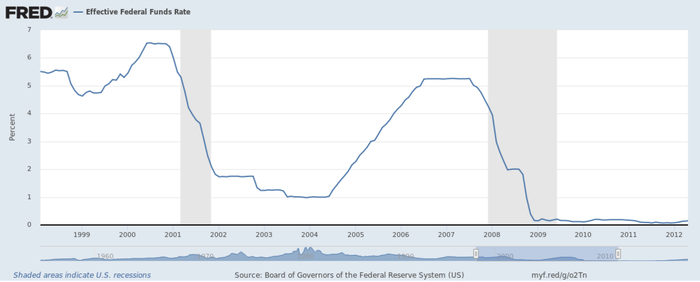

Look at the last two instances when the federal funds rate dropped significantly (2000-1 and 2007-8), and you'll notice the reductions occurred gradually, not all at once. While some declines were more pronounced (such as from December 2007 to May 2008), unless something drastic happens, we won’t see a drop from 3% interest to 0.25% on CDs in just one month.

If you're looking to keep your money out of sight and mind for a few months, a CD is a reliable choice at this moment. But there’s no need to rush into signing up just out of fear that these rates might disappear soon.