Ah, money. It's supposed to be a constant, right? As long as we have enough, we can buy the essentials—food, services, security...you know the drill.

Sadly, many governments treat money like an endless resource, as though they can simply print more whenever they need it. But as we’ll explore, the cycle of replacing poor money with even worse money can ultimately drain a nation’s wealth.

Here are ten instances when official currency met its untimely demise.

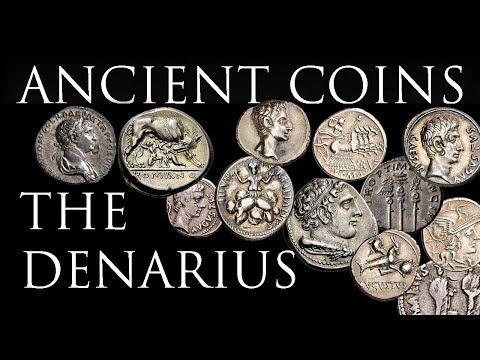

10. The Roman Denarius

A symbol of patriotic resistance during Rome's struggle against Hannibal in the Second Punic War, the denarius was introduced in the late third century BC. This coin was made of nearly pure silver and weighed 4.2 grams.

Its peak came after Rome’s victorious conquest of Macedonia in the mid-second century BC, which provided abundant silver deposits, boosting the money supply tenfold. The denarius became so widespread that, by the middle of the first century BC, the word 'Roma' was removed from the coin as it had become so universally recognized. Roman mints churned out millions of denarii each year, which circulated freely not just within the Empire but anywhere Romans traded.

Unlike modern currencies, the denarius wasn’t just backed by precious metals—it was a precious metal. Each denarius contained a specific amount of silver, giving citizens a tangible sense of its value.

However, as costs mounted—particularly military expenses—Roman leaders gradually reduced the silver content of the denarius. By the third century AD, as Rome’s power dwindled and territories were lost along with tax revenues, maintaining military outposts became more labor-intensive, while the treasury lightened. As the silver content of the denarius plummeted to just 5%, people started hoarding older coins with higher silver content, a clear indication that faith in the currency was fading.

In the end, the Roman government lost confidence in its own currency, mandating that taxes be paid in gold or kind. Citizens flooded the market with denarii, causing inflation and hastening the coin's downfall.

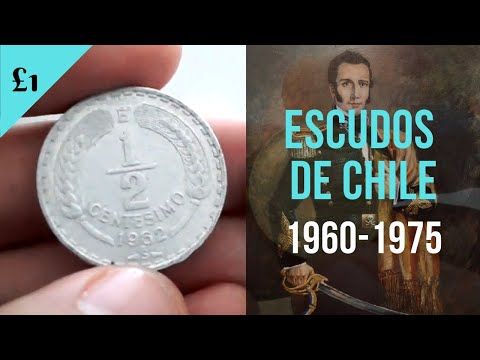

9. The Chilean Escudo

The escudo was a brief and fleeting currency, introduced in 1960 to bridge two different iterations of the peso. Its creation aimed, in part, to restore confidence in Chile’s currency system. At the start, one escudo was worth 1,000 pesos.

Things were going smoothly until the rise of socialism. After failing three times before, the Marxist Salvador Allende finally became Chile’s president in 1970. The leader of the Socialist Party wasted no time in nationalizing industries and ramping up social spending to redistribute wealth to the lower classes.

Initially, Allende’s aggressive monetary policies fostered some economic growth, but, as often happens, this also stoked inflation. Soaring prices were worsened by widespread labor strikes, which led to severe declines in production and exports. Furthermore, price controls introduced to combat inflation triggered a rise in black market trading, severely hurting tax revenues.

By late 1972, inflation had reached a staggering 600%, and by the following year, it doubled to 1200%. Unable to meet its financial obligations, Chile defaulted on foreign debts, including payments to international banks. Allende’s government was toppled, and he ultimately took his own life—another chapter in the volatile history of South America.

The escudo's story came full circle when it was replaced by the New Peso in 1985, with a conversion rate of 1,000 to 1. In just a short time, Chile transformed into a democratic, economically liberal nation, with such a dramatic turnaround that economist Milton Friedman famously called it the 'Miracle of Chile.'

8. The Peruvian Inti

In the same year that Chile introduced the New Peso and began its economic recovery, its northern neighbor Peru was spiraling into financial disaster, debuting a currency that would last even less time.

Once a prime target for foreign investment, in the 1980s Peru embarked on an expansion of public spending...without a plan for managing the mounting debt (yes, United States, we’re looking at you). Paradoxically, it was Peru’s push for societal and economic liberalization that crippled both its finances and two successive currencies, including the Inti’s brief six-year existence.

The backdrop: In 1980, Peru saw its first democratically elected government in 12 years. President Fernando Belaúnde’s administration significantly liberalized the country’s trade policies. While such policies generally boost competition and innovation by easing restrictions on goods and services, they can also spook foreign investors, who value stability over an unpredictable market environment.

Investment dried up, and as inflation spiraled out of control, Peru's currency—the sol—was rebranded as the inti, with a conversion rate of 1,000 to 1. But for Peru, it was the same story with a different currency. By the end of 1990, inflation had hit 400% per month, prompting the creation of a 10,000,000 inti banknote to keep up with hyperinflated prices.

It didn’t work. Forgive the pun, but the sun rose again: In 1991, the inti was replaced by the nuevo sol, at a jaw-dropping conversion rate of one million to one.

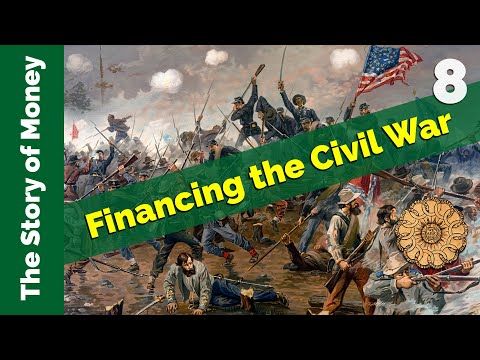

7. The U.S. Greenback

Wars are expensive. As the Civil War escalated, the U.S. government issued a special emergency currency. Known as greenbacks due to the signature green ink that remains a hallmark of modern American bills, these notes differed from traditional currency in that they were not backed by precious metal reserves.

The greenback traces its origins to the Panic of 1857, the first major financial crisis in American history. The aftermath forced President James Buchanan’s administration to take on significant debt. When the Southern states seceded four years later, the loss of federal tax revenue only deepened the financial woes.

Originally, greenbacks known as Demand Notes were backed by gold. However, as the war stretched on and costs piled up, the U.S. issued $450 million in U.S. Bank Notes that were not backed by anything. This flood of unbacked currency led to a steady decline in its value compared to gold.

Greenbacks were both a blessing and a curse: While they covered 15% of the war’s costs, their unstable value led to rising prices for everyday goods. Consequently, inflation hit 14% in 1862, and 25% in 1863 and 1864. Nevertheless, the greenback managed to recover after the war.

Ironically, the greenback’s eventual phase-out is rooted in its very foundation: the idea that money doesn’t need to be backed by precious metals. The final remnants of America’s gold standard were dismantled in the early 1970s, as the economy was considered strong enough to move beyond it. Federal Reserve notes became the new norm, and, half a century later, America now faces a somewhat unmanageable $30 TRILLION debt—roughly $90,000 per citizen. Time to invest in gold stocks.

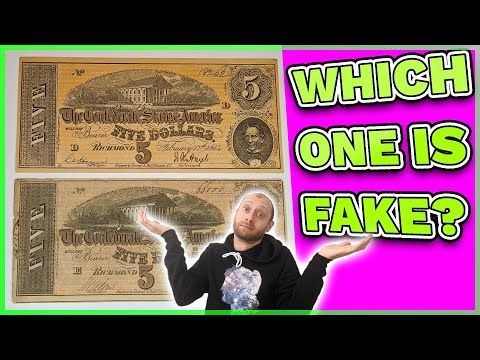

6. The Confederate Dollar

The greenback’s Confederate counterpart was the greyback, the currency of the Confederate States of America. Jefferson Davis, the nation’s first and only president, appeared on the $50 note, while Vice President Alexander Stephens graced the $20. Rebel leader John C. Calhoun appeared on the $100 note, alongside a portrayal of enslaved African Americans. How chivalrous.

Much like the greenback, the Confederate dollar was a speculative gamble, though with even less chance of success. A Confederate note was essentially a promise to pay the bearer after the war—if the South achieved independence. This led to a volatile currency that fluctuated based on daily developments. For example, when news broke of the South’s defeat at Gettysburg in July 1863, the greyback plummeted by 20%, prompting the government to urge businesses to lower their prices to offset the depreciation.

In October 1863, Confederate Senator Louis Wigfall of Texas lamented that a soldier’s monthly pay of $11 had, by then, the same value as one Confederate dollar at the start of the war. Eventually, even that meager purchasing power vanished, as many merchants ceased accepting the Confederate dollar, predicting the collapse of the young nation.

As the Confederacy’s prospects continued to fade, its currency followed suit. By the end of 1864, the Confederate dollar had lost so much value that a turkey cost $155, and a ham was priced at $300. When Richmond fell and Lee surrendered in mid-1865, the currency became worthless.

5. Ex-Soviet Siblings: The Belarusian Ruble & Yugoslavian Dinar

Neither Belarus nor Yugoslavia navigated the collapse of the Soviet Union particularly well. Both of these Mother Russia orphans faced their own brand of separation anxiety, which quickly transformed into financial panic.

In Belarus, the government shifted from authoritarian to... well, still authoritarian. The country’s first president, Alexander Lukashenko, who assumed office in 1994, is currently Europe’s longest-serving “president,” a term that increasingly reflects the reality of being a “dictator” in Eastern Europe. Over the decade following Belarus' independence from the USSR, Lukashenko enacted a potent mix of aggressive currency printing, price controls, and industry nationalization that stifled productivity.

To cope with rampant inflation, the Belarusian Ruble soon had three zeros added to all its bills—an accounting maneuver designed to disguise the country's economic turmoil. It has since hit an all-time low against the U.S. dollar, partly due to its growing diplomatic isolation.

From 1992 to 1995, the states that once made up the Socialist Federal Republic of Yugoslavia went through multiple iterations of the dinar, as they tried—and failed—to stabilize their economies. At the peak of hyperinflation, prices were doubling every single day, and in just two years, the dinar lost an astronomical value—jumping by more than a QUADRILLION percent (that’s a 1 followed by 15 zeros).

Eventually, each newly independent nation charted its own financial course. Serbia introduced a new dinar in 1997, while Montenegro initially used the German Deutsche Mark from 1995, before switching to the Euro in 2002.

4. The Weimar Papiermark

It’s one thing for a rebellious breakaway republic like the Confederacy to risk everything on the outcome of a war. It’s another entirely for a fully established nation to gamble its future in the same way.

To fund World War I, Germany abandoned its gold standard and resorted to borrowing. After four years of bloody stalemate, resulting in millions of lives lost but little to show for it, the Weimar Republic found itself drowning in war debt—amounting to hundreds of billions. The country’s infrastructure and economy were devastated, yet it still owed reparations to equally devastated nations, notably France, to the tune of 132 billion marks—equivalent to about $269 billion in today’s currency.

The reparations came with harsh terms. Germany’s first payment of 50 billion marks was due in mid-1921, but there was a catch: the payment had to be secured with hard assets, meaning it couldn’t be made with the rapidly plummeting mark. The rush to buy foreign currency only accelerated the mark’s devaluation.

In the following year, Germany’s cost of living skyrocketed by 17 times within just six months. Caught in a vicious loop of printing more and more worthless currency to purchase foreign assets to settle its war debt, Germany eventually defaulted on a payment. This led to the occupation of its chief industrial region, the Ruhr Valley, by France and Belgium.

This situation created the perfect conditions for a populist uprising and, ultimately, another World War. As for Germany’s World War I debt, it was finally settled…after a staggering ninety-two years. The final payment of 70 million euros was made in 2010.

3. The Zimbabwe Dollar

The crown for the most inflated currency in history goes to... Zimbabwe.

Ruined by ongoing racial conflicts and an economically uninformed government, Zimbabwe began to massively print money during the 1990s. This spree continued into the early 2000s, and in 2006, the country made international news when its inflation rate hit a shocking 1,000%.

However, that was just the start. In a move that has repeatedly failed throughout history, Zimbabwe printed increasingly larger denominations to keep up with soaring prices. By mid-2008, the first billion-dollar notes were issued. Within months, inflation surged to an unbelievable 500 QUINTILLION PERCENT. To visualize this figure: 500,000,000,000,000,000,000.

In response, the government passed a law that removed ten zeros from all notes and prices. Did this bring an end to the crisis?

Not exactly. The following year, Zimbabwe stopped issuing its own currency and briefly permitted the use of foreign currencies. In the mid-2010s, it switched entirely to the U.S. dollar before reintroducing a new version of the Zimbabwean dollar in 2019. How's it faring now? By July 2020, inflation had soared to nearly 750%, and in October of that year, the country's largest business organization warned of the Zimbabwe dollar's potential collapse.

2. OneCoin

Another infamous failed cryptocurrency crashed... because it never even existed.

In 2014, the self-styled 'CryptoQueen' Ruja Ignatova launched OneCoin. Advertising it as a 'Bitcoin Killer,' she drew attention and attracted investors by organizing lavish events across the globe, including one at London's Wembley Arena.

Ignatova claimed that around 120 billion OneCoins were available through the dubious process of crypto mining. These coins could then be used like any other digital currency through a dedicated OneCoin e-wallet.

A key element of OneCoin's early fundraising strategy involved the sale of educational resources, including courses on cryptocurrency, trading, and investing. These courses were part of a multi-level marketing operation—also known as a pyramid scheme—where participants could earn rewards by recruiting new members. Buyers of these 'course packages' were promised tokens that could be used to mine OneCoins.

OneCoin's currency exchange platform was called xcoinx. However, only members who purchased higher-tier education packages were granted access to it. Eventually, selling limits were imposed on accounts based on the level of the educational package bought. As the scheme drew attention, national authorities began taking action, and in 2016, both Norway and Hungary officially labeled OneCoin a scam.

By the time OneCoin was shut down in 2017, millions of investors had fallen victim to what became a $4 billion Ponzi scheme. As for Ignatova, she has become a modern-day cyber Carmen Sandiego. On the run since 2017, she remains unapprehended despite being on international wanted lists.

1. Dogecoin

OK, Dogecoin isn’t completely dead. But it's hanging by a thread, and the vet is ready with the final shot.

In 2013, the cryptocurrency Dogecoin was introduced with little fanfare. In fact, it was one of the first digital currencies created as more of a joke than a serious financial endeavor. The coin's virtual emblem features Doge, a Shiba Inu dog whose confused yet adorable expression had become an Internet meme sensation.

Dogecoin’s website humorously declared its mission to 'take over the world.' The playful tone quickly gained traction, and before long, people were saying 'Oh, hi Doggy' faster than Tommy Wiseau. Dogecoin raised $8 in just two weeks, and by May 2021, it boasted a market cap of $85 billion. Just two months later, it made its way onto a list of Memes That Changed History on a quirky website called Mytour.

However, the laughter stopped for Dogecoin’s investors. In late June 2021, Forbes published an article with the title “Downward Facing Dogecoin,” spotlighting the plummeting market of several cryptocurrencies. Around that time, many Bitcoin alternatives began to tank.

By early January 2022, Dogecoin's value dropped to a mere 8 cents, and experts were warning that it might collapse entirely. When a currency is born out of humor, the punchline often lands hardest on its investors.