It's often said, 'spend less than you earn, save up, and—poof!—your financial issues disappear.' If only it were so simple. Being financially tight is tough enough, but then there are additional hurdles that make it even harder for those with less money to reach financial stability. For instance, here are some expenses that actually hit low-income individuals harder.

Essential Household Items: Toilet Paper and Beyond

You might not be familiar with the term 'the toilet paper effect,' but you're certainly aware of how it works.

A study from the University of Michigan tracked the toilet paper purchasing habits of over 100,000 American households for a period of seven years. Researchers found that households with higher incomes bought toilet paper on sale 39% of the time, compared to just 28% for those with lower incomes. Additionally, they purchased more rolls on average. The study concluded that low-income households end up paying about 6% more per sheet, and here’s what the researchers discovered:

Being unable to buy in bulk prevents low-income households from timing their purchases to take advantage of sales. Additionally, not being able to accelerate purchase timing to buy during sales makes bulk buying harder. The researchers found that the financial losses resulting from underutilizing these strategies can amount to as much as half of the savings gained by purchasing cheaper brands.

In essence, as the study’s title suggests, Frugality is Hard to Afford. We've gone in-depth about this issue before. It’s not just about toilet paper. When you're struggling financially, buying in bulk or investing in durable, high-quality items becomes difficult. There are many subtle and systematic ways in which low-income individuals end up paying more, and some of these expenses are even more obvious.

Car Insurance

Car insurance premiums can be complicated, and there are some unexpected factors that can cause you to pay more for car insurance—such as renting your home or not having a college degree, for instance.

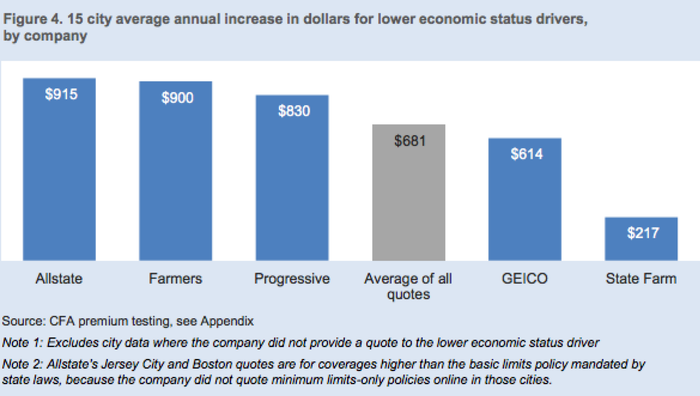

Recent research (PDF) from the Consumer Federation of America (CFA) revealed that individuals with lower incomes tend to pay more for their insurance, and it’s not due to poor driving habits. Specifically, the study found that responsible drivers are paying an extra $681 per year on average, simply because of personal traits linked to their lower economic status.

The CFA gathered quotes from five of the largest insurance companies in the United States. They compared policies for two men and two women who had identical cars, addresses, and driving records. The only differences were in their socio-economic backgrounds, and they discovered that insurers were charging anywhere from 40% to 90% more:

Sure, one might argue that car insurance premiums are higher for a reason, but the undeniable truth is: they are generally steeper for those with lower incomes, even when these individuals are good drivers.

A College Education

This expense might catch you off guard. The common belief is that the poorer you are, the more grants and scholarships you qualify for.

That may hold true in some cases, but many colleges, particularly private institutions, employ a tactic called 'gapping' to extract more money from lower-income students—or even push them away from enrolling altogether. Essentially, these colleges offer prospective low-income students financial aid packages that don’t fully cover their needs. They intentionally underfund these students and reserve the aid for wealthier ones who can afford to pay the full tuition. A recent report from the New American Foundation detailed this issue:

...colleges are increasingly using their own institutional aid dollars as a “recruiting tool,” rather than as a means of meeting a student’s financial need...

In practice, this means that the most accomplished students, often from wealthy families, are given the most substantial financial aid packages from their institutions.

In simple terms, this system makes college more expensive for lower-income students. They may receive aid, but it’s insufficient. Meanwhile, wealthier students receive more financial help than they actually need. Consequently, poorer students are forced to take out larger loans to cover the shortfall, graduating with much higher debt.

Banking and Other Financial Services

Bank fees make it unnecessarily expensive just to keep your money in an account, which is absurd. However, they’re relatively easy to avoid—if you have the funds to do so.

For instance, Bank of America’s standard checking account charges a $14 monthly maintenance fee. This fee is waived if you maintain a minimum daily balance of $1,500 or more, which can be tough for low-income individuals. You can also avoid it by signing up for their credit card and meeting certain criteria. This option works if you have good credit. Some banks offer fee waivers if you have a direct deposit of a specified amount, which could be a viable option if you have a job that pays enough and offers direct deposit.

The reality is: while solutions exist, they often don’t work well for those who are struggling financially. Studies show that lower-income individuals have fewer financial service options, which forces them to rely on costly alternatives: payday loans and other forms of debt traps.

For instance, a study from the National Poverty Center revealed that 17% of the unbanked reported being denied when attempting to open a bank account. Many others have had their existing accounts closed due to falling below the minimum balance requirement. Whatever the reason, lacking access to these accounts makes it even more difficult to save, work toward financial stability, or build a financial cushion. The basic, reasonable services that many of us take for granted are far less accessible to low-income households, which results in them paying much higher costs for alternatives.

Anyone who has ever struggled with poverty knows how extremely expensive it is to be poor. -James Baldwin

It’s easy to criticize others' decisions and offer simple solutions—just avoid falling into a debt trap, right? You’d be foolish to take out a payday loan. The reality is, though, that many people face limited alternatives. If you're struggling financially, it's not to say there's no way to improve your situation, but it does require overcoming extra barriers that many people don’t see. When you're aware of these barriers, you’re in a better place to find solutions.

Illustration by Sam Woolley