Since the advent of the Internet, companies have utilized this global platform to market their goods to an ever-growing segment of the world's population. Many of us have purchased products online using credit cards or bank accounts. However, developers have long sought to create a unique currency designed specifically for the digital world. They achieved this goal in 2009 with the launch of Bitcoin.

10. The First Bitcoin Purchase Was For Pizza

On May 18, 2010, Laszlo Hanyecz made a post on a Bitcoin forum called Bitcoin Talk. At that time, Bitcoin was still in its early stages. It was highly volatile, and each Bitcoin was worth just a few cents. Hanyecz’s post offered 10,000 bitcoins in exchange for two Papa John’s pizzas. This transaction went down in history as the first-ever purchase made with Bitcoins.

On May 22, Hanyecz shared that someone had taken up his offer. At that point, he found it interesting that he could get a pizza in exchange for virtually nothing. Hanyecz continued to purchase pizza with Bitcoins until the summer, when he ran out of the cryptocurrency. He didn't give it much thought because, like many others at the time, he believed Bitcoin would never really gain traction as a currency on the Internet.

For the next few years, it appeared that everyone’s skepticism about Bitcoin was well-founded. However, in 2013, the cryptocurrency attracted the attention of investors and speculators, leading to large-scale trading. The value of Bitcoin surged dramatically, reaching up to $1,200 before settling between $500 and $700. If Hanyecz had used his 10,000 Bitcoins in mid-2014 to buy two pizzas, those Bitcoins would have been worth approximately $5 million today.

9. Bitcoin’s First Major Use Was On The Silk Road

For those who are unfamiliar with the Silk Road, it was a marketplace that allowed anonymous buyers on the Internet to purchase illegal drugs. Its name was inspired by the historical trade route linking Europe with the Orient. It operated in secrecy from the beginning until it was shut down in 2013 after a thorough investigation by multiple government agencies. One key factor contributing to the success of the Silk Road was its use of Bitcoin, a fully anonymous form of payment.

The Silk Road's operations required access through the Tor anonymizing network. Once users entered the Silk Road, they could buy anything from cocaine to LSD, as well as other illicit items like fake IDs, stolen credit card information, and hacking tools.

Law enforcement had trouble infiltrating the Silk Road due to the expertise of its users. The Tor network concealed digital identities, and the use of Bitcoin only revealed IP addresses that offered little to no useful information. To finally dismantle the seemingly untouchable Silk Road, a multi-agency task force, named 'Marco Polo' after the famous explorer, was formed. It included cooperation from the FBI, DHS, IRS, DEA, US Postal Service, and the Department of Alcohol, Firearms, and Tobacco.

The task force’s main target was the enigmatic Dread Pirate Roberts, the founder and operator of the Silk Road. This marked the first time that government agencies dealt with such sophisticated digital technology, leaving them largely uncertain about how to proceed with tackling the Silk Road.

The investigation began with the arrest of various sellers, slowly gathering pieces of information about the inner workings of the organization. It wasn’t until 2013 that the Dread Pirate Roberts, also known as Ross Ulbricht, was caught. This case provided a crucial lesson in how easily anonymous illegal operations could be run using digital tools like Bitcoin.

8. Bitcoins Have Created An Entire ‘Mining’ Industry

Bitcoin 'mines' are specialized facilities where intricate algorithms are solved, resulting in the generation of new Bitcoins. The majority of these mines are located in China, where they are often secretive operations that function outside the bounds of the law. As of now, the Chinese government has not issued a clear stance on Bitcoin, which has allowed miners to accumulate substantial fortunes.

One such facility, Bitbank, operated by entrepreneur Chandler Guo, generates $8 million annually and is considered one of the largest mining operations in the country. Workers at this facility solve complex cryptographic puzzles on computers to verify transactions globally. Each puzzle solved adds a 'block' to the 'blockchain,' and miners who solve these problems are rewarded with Bitcoins.

At the Bitbank facility, around 50 Bitcoins are mined daily by workers who run operations 24 hours a day. At one point, China controlled roughly 40 percent of the world's Bitcoin mines. However, by 2016, it dominated the global mining industry, accounting for nearly 70 percent of all Bitcoin mines located within the country.

Not everyone within the Bitcoin community is thrilled with this. Bitcoin enthusiast Michael Hearn argues that China's slow Internet infrastructure could stifle Bitcoin's popularity and potentially cause the currency to fail.

7. Bitcoins Are Incredibly Easy To Steal

In 2014, Mt. Gox, the world’s largest Bitcoin exchange at the time, declared bankruptcy after reporting that around 850,000 Bitcoins were stolen by hackers. The stolen Bitcoins were valued at $450 million. Mt. Gox’s CEO, Mark Karpeles, also reported that $27 million in cash was taken. This incident sent shockwaves through the Bitcoin community, as it revealed just how easy it was to steal Bitcoins with minimal effort.

With a solid grasp of hacking, it's easy to breach Bitcoin exchanges, and that’s exactly what the unknown culprits did. Mt. Gox had been a frequent target for hackers, who had previously stolen 80,000 Bitcoins before Karpeles took charge of the company in 2011.

Although Karpeles was known to have embezzled $2.7 million from the company, 650,000 Bitcoins (worth approximately $300 million) are still missing. This isn’t just limited to exchanges getting hacked either.

Sheep Marketplace, a successor to Silk Road, became the victim of a £60 million heist, causing the site to collapse shortly after. The hackers managed to manipulate account balances, ultimately wiping the site clean in under a week.

Since Bitcoins can't truly vanish, they must be laundered differently from regular currency. The stolen Bitcoins are gradually shuffled through blockchain networks, mixed with others, and eventually vanish without a trace.

Tracking the process is possible, and many Sheep Marketplace users managed to uncover where their stolen Bitcoins were being shuffled. In 2016, two men from Florida were arrested for the heist, but by that point, the stolen Bitcoins had depreciated to just $6.6 million.

6. Bitcoins Have Become the Currency of Choice for Extortionist Hackers

In February 2016, Hollywood Presbyterian Medical Center became a victim of a hacking attack where its systems were held hostage. With critical operations paralyzed and lives at stake, the hospital was forced to meet the hackers' demands of $17,000 in Bitcoins. This despicable act wasn't an isolated incident.

Prior to the hospital hack, there were other instances of extortion involving smaller sums. For example, a police department in Boston was forced to pay $500 in Bitcoins to hackers, and a sheriff's department in Maine faced a similar situation.

Though the extortionists remain unidentified, it's known that one criminal network, based in either Russia or Ukraine, has raked in almost $16.5 million in Bitcoin from hacking victims in the United States. The typical extortion demand is around $20,000, always paid in Bitcoin.

Because Bitcoin wallets aren’t required to be registered with any government, Bitcoin has become the preferred currency for digital extortionists. One such group, known as DD4BC, has gained notoriety among corporations for demanding $10,000 in Bitcoins.

One of DD4BC's public emails states: “Do not ignore me, as it will just increase the price. […] Once you pay me, you are free from me for the lifetime of your site.” While some digital security experts have proposed solutions—such as marking the Bitcoins used, similar to how stolen cash is tracked—the extortion continues unabated.

5. Bitcoins Facilitate Easy Scamming

Considering the range of crimes that can be fueled by Bitcoin, it’s not surprising that scammers have embraced the cryptocurrency. A 2015 report by Southern Methodist University highlighted some of the most prevalent Bitcoin scams. Between 2011 and 2014, 41 scams occurred, totaling nearly $11 million in losses.

Bitcoin investment schemes are relatively straightforward and bear resemblance to Ponzi schemes. Investors are promised unrealistically high returns, only to find that their funds have been funneled into the scammer’s wallet.

For instance, in the case of fake Bitcoin mining operations, scammers promise to mine Bitcoins on your behalf for a fee, but in reality, they simply pocket the payment. There are also Bitcoin wallet scams, where it appears you’re making a deposit into a verified wallet, but eventually, all the funds are redirected to the scammers. Another common scam involves Bitcoin exchanges offering low conversion rates for turning Bitcoin into cash, but they fail to follow through on the transaction.

4. Bitcoins Could Be Exploited for Terrorist Financing

In 2014, an individual known as Amreeki (‘American’) Witness published a .pdf on WordPress, explaining that it was difficult for many ISIS supporters to contribute financially due to restrictions from the Iraqi government. His proposed solution was for supporters to donate in Bitcoins, which could be anonymized through the process of 'mixing', making them untraceable.

Bitcoins present a potential shift in how terrorism is financed because of the anonymity they provide. While it is possible to track transactions to some extent, Bitcoin can be effectively laundered (through multiple rounds of 'mixing') and sent to illicit groups like ISIS. Even though ISIS would still need traditional currency for their operations, the Pentagon has flagged digital currencies like Bitcoin as a potential threat, as they could serve as a significant revenue stream for terrorist groups.

After the 2016 Paris attacks, the European Union took action to combat terrorist financing, with Bitcoin being one of the primary focuses. The European Commission, the EU’s financial body, is considering implementing regulations that would require Bitcoin transactions to be linked to an individual's identity, in an effort to prevent funds from reaching terrorist organizations.

Just like the Silk Road, the deep web remains a favorite platform for ISIS, where Bitcoins from sympathizers are funneled. While removing Bitcoin's anonymity would alter one of its core features, most users and exchanges would not oppose such changes, as the majority of Bitcoin transactions are legitimate.

3. Bitcoins Might Collapse In The Future

As mentioned earlier, Bitcoin enthusiast Mike Hearn believes that Bitcoins might fail in the future if they continue to follow their current path. According to Hearn, those in control of Bitcoin have lost track of the original purpose of the currency. Many discredited Hearn, but his prophecy has caused some to look deeply into Bitcoin’s functions and the reasons why he claimed Bitcoins are doomed.

His first reason was that Bitcoins were initially meant to be a decentralized currency, unlike most other physical currencies. However, Bitcoins are now controlled by a small group of people, the exact opposite of what was supposed to happen.

Hearn also claimed that there is an internal split at Bitcoin between those who want technology to increase transactions and those who are opposed to this. Blockchain, the technology behind the Bitcoin transactions, has become increasingly random as to the speed of transactions. Hearn said that it could take anywhere from 60 minutes to 14 hours for a transaction to go through.

However, his primary concern was the limited number of individuals (around 10) who control Bitcoin. He suggested that as long as this small group holds the reins, Bitcoin is destined to be an 'inescapable failure.' Whether Hearn's prediction will come to pass is still uncertain, but for now, Bitcoin has become one of the most intriguing developments in the digital age.

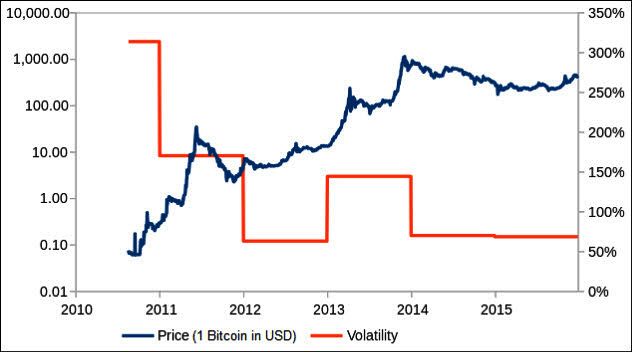

2. Bitcoins Are Extremely Volatile For Various Reasons

Since the introduction of Bitcoin, its price has risen from just a few cents to several hundred dollars by mid-2016. Despite this remarkable increase, the value remains unstable and subject to significant fluctuations. As a result, many people remain cautious about the currency. Over time, several factors have been proposed to explain why Bitcoin's value can plummet or skyrocket unpredictably.

The value of Bitcoin is influenced by the basic economic concept of supply and demand. In 2014, the price plummeted by 60 percent, leading many to believe that Bitcoin's decline was inevitable.

However, in the same year, a number of companies in Silicon Valley began investing in Bitcoin, and many businesses started accepting it as a payment method. This contributed to a rise in Bitcoin's value once again. While Bitcoin didn’t become widely adopted by the general public, its technological progress continued to support its growth.

In 2015, Bitcoin's value became volatile again due to a Russian pyramid scheme that gained massive popularity in China. Since the scheme only accepted Bitcoin, Chinese investors started buying in large quantities, pushing the price upwards.

This year, demand from China surged once more, particularly after the yuan's devaluation. As a result, Bitcoin's price increased by 20 percent. Although the price continues to fluctuate, experts generally believe Bitcoin will remain a part of the market for the foreseeable future, especially as more companies integrate it as a payment method and demand holds steady.

1. The True Identity of Bitcoin's Creator Remains Unknown

The only thing known about Bitcoin's creator is the pseudonym Satoshi Nakamoto. Just like the cryptocurrency he developed, Satoshi remains largely anonymous. He introduced Bitcoin in 2009, communicating only via email with early users—never by phone or in person. Even after Bitcoin's meteoric rise, Satoshi remained out of the public eye and completely vanished in 2011.

In 2014, Newsweek published an article claiming to have uncovered Satoshi's true identity, identifying him as a reclusive, unemployed engineer in his sixties from a Los Angeles suburb. However, those within the Bitcoin community quickly dismissed the claim, affirming that this individual was not Satoshi.

A popular theory within the Bitcoin community suggests that Satoshi could be a reclusive American named Nick Szabo, of Hungarian descent. Despite this, Szabo has denied being Satoshi, though he remains an influential figure in the world of Bitcoin.

Although Satoshi has not been involved in Bitcoin since 2011, his identity continues to spark speculation. However, in the grand scheme of things, his absence has not had a significant impact on the evolution of Bitcoin.

In May 2016, Australian entrepreneur Craig Steven Wright made a claim to be the elusive Satoshi Nakamoto. However, his assertion was quickly met with skepticism, with many asserting that if the real Satoshi wished to be known, his identity would be indisputable. Supporters of Wright, however, argue that the identity of Satoshi is irrelevant, as Bitcoin's growth would continue regardless of who its creator is.

At the time of Satoshi's disappearance, he is believed to have held as many as one million Bitcoins. Today, those Bitcoins could be worth hundreds of millions of dollars, highlighting the incredible value that the cryptocurrency has accumulated over the years.