The recently passed coronavirus relief package introduced more flexible rules for withdrawing funds from your retirement account. While this offers a financial lifeline to those in need, there are important factors to consider before you begin making withdrawals.

Let’s take a closer look at the changes.

New rules for early withdrawals from retirement accounts

You can withdraw up to $100,000 from your retirement account for coronavirus-related reasons, with the usual 10% penalty being waived. This option is available until the end of the year.

If you repay the withdrawn amount within three years, you won’t owe any income tax on it. If not, you have a three-year window to pay the taxes due on that sum.

You may also borrow up to $100,000 from your 401(k) (or 403(b) or similar employer-sponsored account), rather than the usual $50,000 limit. However, loans cannot be taken from your IRA.

This option is only available for 180 days after the bill’s passage on March 27—so it expires at the end of September.

Normally, you're restricted from borrowing more than half of your account balance, but that limit is suspended during this period. If you currently have a loan due this year, you get an additional year to repay the full amount.

Who qualifies for an early distribution without penalties?

The broadened rules for penalty-free early distributions apply to three groups of individuals:

Individuals diagnosed with the coronavirus

People whose spouse or dependent has been diagnosed with the coronavirus

Those facing financial strain due to the coronavirus

The third category, financial hardship, has specific inclusions. Here’s what qualifies as ‘financial hardship’:

Being quarantined

Being furloughed or laid off from work

Experiencing a reduction in work hours

Inability to work due to lack of childcare

Closure or reduction in hours of a business you own or operate

“Other factors as determined by the Secretary of the Treasury”

“The rules are quite flexible,” explained Whitney Morrison, a CFP and director of financial advisory at LegalZoom. “It’s accessible to most people.”

This should be your last option

Before withdrawing from or borrowing against your retirement savings, make sure you've explored all other alternatives.

“$100,000 is a significant amount,” Morrison cautioned. She noted that while small business owners with payroll obligations might require such funds to weather the current challenges, it may be unwise for an individual to access that much. “You could end up depleting your entire 401(k),” she said.

“The market has been volatile and down,” Morrison remarked. “Any withdrawal you make now, even if you replace the funds later, is locking in those losses.”

While withdrawing funds or taking a loan may be better than high-interest debt like payday loans, Morrison advised that it should only be considered if you lack income, savings, family support, or access to low-interest options like credit card balance transfer offers.

Don’t forget about the other resources currently available, said Jorge Soriano, a CFP and financial advisor at GTE Financial in Tampa. From your relief check to expanded unemployment benefits to options for deferring your mortgage or utilities, “Find ways to pay [your bills] before dipping into your retirement savings,” he said.

If you must go this route, Morrison cautioned against acting impulsively due to fears of not having enough cash to manage—or worse, trying to access funds because you’d prefer cash over weathering a turbulent stock market. “Start with small withdrawals, and if you need more, you can take out additional funds later,” she advised. With loans available until September and distributions possible until December, you can revisit your retirement savings if you need financial relief later on.

A retirement loan or distribution doesn’t require a credit check, which makes it a viable option if your credit is less than ideal. However, even with no penalties and extended time for taxes, “you’re still withdrawing from your future self,” Morrison cautioned.

The younger you are, the greater the risk

If you're in your 20s or 30s, you might think you have plenty of time to recover after withdrawing from your retirement savings. However, Morrison cautioned that you could be putting yourself at a significant disadvantage. “Consider why retirement accounts are so effective: the extended time they have to grow due to compound interest,” she explained. Withdrawing funds at 55 won’t impact your growth potential as much, but someone who’s 35 could miss out on decades of growth.

“Withdrawing during a time when the market has seen such a dramatic downturn, like we’ve experienced in the past month, significantly hurts your retirement savings,” Soriano remarked. “Recovering from that loss will be extremely challenging.”

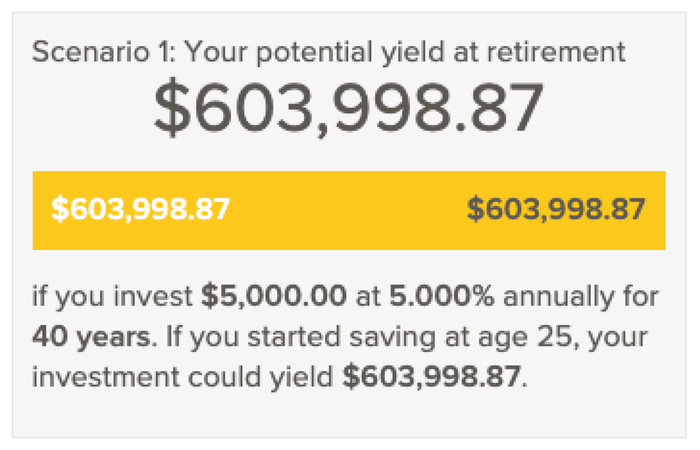

Let’s look at some simple calculations. Imagine you start saving for retirement at 25, contributing $5,000 annually with a 5% return (we’ll keep it conservative for now, just for demonstration).

That’s nearly $604,000. But let’s say you started that account and then emptied it out back to $0 when you’re 29. The next year, you start saving again. You might think you’ve only lost five years of progress, but it’s really five years plus the compound interest you could’ve earned in those five years—and every year thereafter.

Yes, you made it through some tough times, but by doing so, you’ve set your future self back by $153,000.

If you decide to take a distribution now, “Try withdrawing from the position that hasn’t experienced significant losses,” Soriano suggested. This could be from a cash-equivalent IRA or a money market account. The more conservative your investment, the better you can minimize the loss when you withdraw funds.

Get ready for the upcoming tax bill

While you won’t face an early distribution penalty on the money you withdraw, you’ll still be responsible for paying income tax on that amount.

Morrison mentioned that some companies will automatically withhold 20% of your funds to cover taxes before releasing the remainder to you. If that’s not the case for your account, make sure to reserve at least 20% of the amount for taxes.

If you know your tax rate, Soriano suggested it can help guide you in setting aside the correct amount for your tax obligations. For example, if your tax rate is 24% and you take a $100,000 distribution, you’ll owe $24,000 in taxes on that withdrawal.

“Keep it in a savings account and set it aside,” advised Morrison. “If you end up needing to use that money later, you may be able to arrange a payment plan with the IRS” for the taxes you owe.

Consult with someone before making this decision

Morrison and Soriano both emphasized that withdrawing from your retirement savings should be a last resort. They also highlighted the importance of speaking with someone first. “Having a second opinion is always valuable,” Soriano remarked.

If you’re already working with a financial planner, don’t rush to fill out online forms late at night without informing them of your plans. Take the time to sit down and review all your options. If you don’t have an advisor, there are low-cost and pro-bono options available during the pandemic.