Checks: They may feel like a relic of the past, yet they still find their way into our lives. And in some cases, they are absolutely essential.

If your check-writing (or check-receiving) skills need a refresher, we’ll help you catch up on everything you need to know to manage your banking with confidence and security. Because even with Venmo, Cash App, PayPal, Zelle, and Apple Pay at your fingertips (we could keep listing...), there will come a time when you’ll need to handle a check or two.

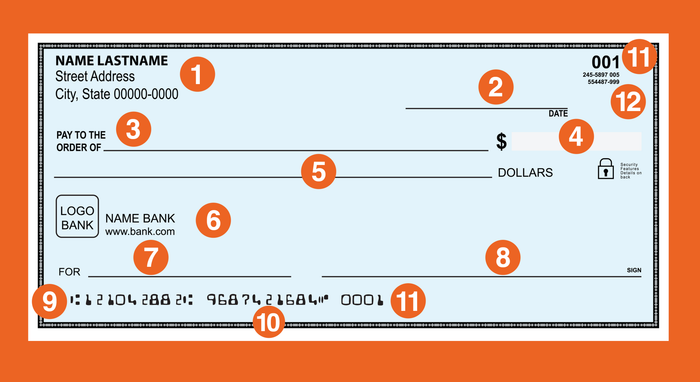

How to Fill Out a Check

If you’re a bit out of practice with writing checks, here’s a step-by-step guide to help you do it like a pro. Refer to the diagram to see what goes where and why.

Your name and address.

The date.

The payee—that’s the person or business you're paying.

The amount, in numerals. This part is called the dollar box.

The amount, written out in words. Be sure to fill the whole line to prevent tampering. For instance, write “Four dollars and zero cents————-” or “Four dollars —————xx/100” to fill the entire line.

Your bank’s name and contact information.

The memo line. You might note an account number or write a reason like “gift for Janet.”

Your signature. If you forget to sign the check, your recipient won’t be able to cash it.

The routing number of your checking account. This number corresponds to the bank where your account is held.

Your checking account number.

The check number. It appears twice: once near the account number and once in the upper right corner. Each check has a unique number, which was useful for record-keeping back in the day, and though not strictly necessary now, it’s still good to keep them in order.

The fractional routing number for the bank. It appears in a specific format.

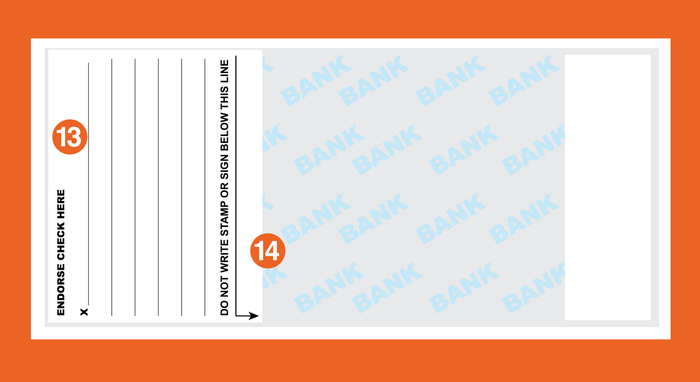

On the back of the check (as shown in the graphic below), sign here to either deposit or cash the check. Be careful not to write below the line!

The security zone. This area is for bank use only to verify the authenticity of the check.

How to Receive a Check

When you get a check (thanks, grandma!), you’ll need to endorse it. This means signing your name in the area labeled #13 on the back of the check. Make sure your signature matches your ID and how the check writer spelled your name. Stick to the designated area, as the rest of the check is for bank use only.

This area is where you may need to provide extra details or instructions. For instance, if you're depositing via mobile or ATM, you’ll likely sign and write “for deposit only” in the endorsement section. If you're depositing the check at a branch, you'll usually need to include your account number either above or below your signature.

Next, it’s time to deposit or cash the check. Keep your debit card or account details ready and be mindful of when your funds will be accessible. If you’re depositing via your phone, hold onto the check for two weeks to ensure the transaction went through correctly.

As you may already know, banks aren’t the only place to cash a check: Many large grocery stores offer check-cashing services, as do businesses specifically dedicated to it. However, if you’re not at your own bank, you might face a fee of around $5 to cash your check, depending on the check amount.

Your Odd Check Questions, Answered

Can I postdate a check to force the recipient to delay depositing it?

If you pay rent via check, you might use this trick: Write the check on the 25th or 26th, mail it, but date it for the 1st of the next month so your landlord can’t cash it before you get paid.

While your recipient and some banks may honor a postdated check, there’s no guarantee they will and nothing stopping them from cashing it anyway. If you need your recipient to wait before depositing the check, make sure to communicate that clearly to them.

I’m writing a check as a wedding gift. How should I handle the names?

Don’t make assumptions about name changes, nor assume the couple has a joint account. Address the check to “Legal Name One OR Legal Name Two” so that either person can deposit it.

What does it mean to endorse a check to someone else?

When you receive a check, you can decide to let someone else access the funds. For example, this could happen if someone else is managing your finances on your behalf.

To do this, first check with the third party’s bank to see if they’ll accept endorsed checks. If they will, the bank will provide instructions. You may be told to write “Pay to the order of [Person]” and sign the check, or simply have the third party sign below your endorsement.

Remember, everything needs to fit within the endorsement box, so avoid getting too creative with your cursive.

What’s a counter check or a starter check?

Your bank gives you starter checks when you open a new account, since it takes a little while to print personalized checks. Keep in mind, not all businesses accept starter checks, so it’s best to ask beforehand if you plan to use one.

Counter checks are temporary checks your bank can print if you need one but don’t have any available. Expect to pay a small fee for this service.

What’s a cashier’s check and why would you need one?

A cashier’s check is issued by your bank and includes the payee’s details printed directly on it. This type of check provides a guarantee that the funds are available—like your bank has given it their official stamp of approval. You might need one for larger payments, such as a rental deposit.

What about the checks that come with your credit card for a balance transfer?

Credit card companies send you blank checks with balance transfer offers so you can easily access the funds they’re making available. For example, you can use one of these checks to pay off another debt, effectively moving that debt to the credit card offering the balance transfer.

Balance transfer checks can be a helpful tool for paying off debt quickly, but they can also complicate the process. It’s a good idea to avoid using them if possible.

My checks are outdated and don’t reflect my current address. Can I still use them?

You can still use old checks as long as your account information (routing and account numbers) are up to date. Simply cross out the old address and write your new one for the recipient’s reference. (Some businesses might ask you to provide ID for verification.)

Where can I order new checks that won’t break the bank?

Banks tend to charge a premium for checks—expect to pay at least $25-30 per box. However, you don’t have to order them directly from your bank. Various services offer affordable options—check out Vistaprint, Checks.com, or even Walmart for budget-friendly alternatives.

It’s 2020. Are paper checks still safe to use?

Like any payment method, the safety of using checks depends largely on how you handle them. To reduce the risk of checks being intercepted, take them directly to the post office instead of leaving them in your home mailbox for pickup. Avoid carrying your checkbook with you to prevent it from being lost or stolen.

As always, be cautious of check scams. If someone asks you to cash a check for an amount greater than what you’re owed, it’s a red flag—chances are, you’re dealing with a scammer.