Loans are not always identical, so understanding how to calculate monthly repayments and due interest is key to selecting a loan that fits your needs. While grasping the exact calculation may require studying complex formulas, it's possible to simplify the process using tools like Excel.

Steps

Quick Overview of the Loan

Entering loan details into an online calculator will quickly help you figure out the interest payments. However, the equation for calculating interest is not straightforward. Fortunately, by searching for 'interest payment calculator' online, you can easily find the result by entering your loan details, such as:

- Principal: The loan amount. For a loan of 5,000 USD, the principal is 5,000 USD.

- Interest Rate: The percentage of the amount you need to pay to borrow. This could be represented as a percentage (e.g., 4%) or a decimal (0.04).

- Term: Usually measured in months, it's the duration over which you'll repay the loan. For mortgages, the term is often measured in years.

- Payment Method: Typically, loans are on a 'fixed term.' However, this can vary for special loans. If you're unsure, always ask whether the interest and payment term are fixed before borrowing.

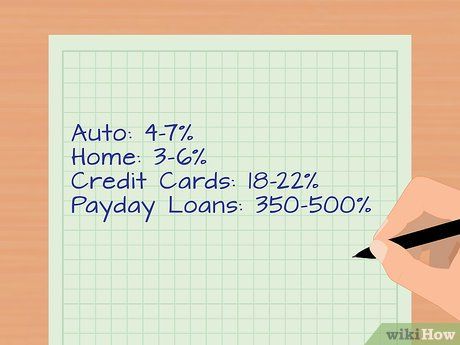

Understand interest rates before borrowing. The interest rate is the fee you pay to borrow money. It represents the amount you must pay on the principal loan over the borrowing term. The lower the rate, the better; even a difference of 0.5% can add up to a significant amount. Choosing lower monthly repayments may lead to a higher interest rate and overall more interest paid, but the monthly payments will be smaller. People with limited savings or incomes based on commissions and bonuses often prefer this option. However, aim to borrow with an interest rate below 10% whenever possible. Common interest rates for various loans include:

- Car loans: 4-7%

- Home loans: 3-6%

- Personal loans: 5-9%

- Credit cards: 18-22%. This is why it's best to avoid making large purchases on a credit card if you can't pay it off right away.

- Short-term loans (payday loans): 350-500%. These loans are very risky if you're unable to repay within 1-2 weeks.

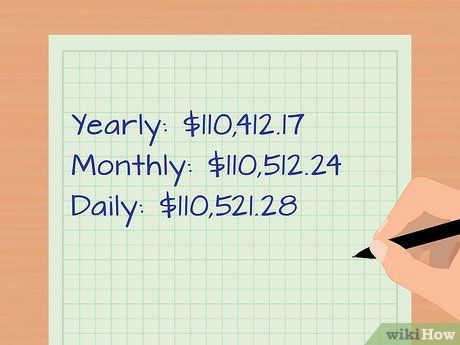

Ask about the compounding rate to know when interest is due. The compounding rate tells you how often the lender calculates the interest you're required to pay. The more frequently payments are made, the higher your total debt will be, as you have less time to repay. However, the upside is that you won’t pay as much interest. For example, consider a loan of 100,000 USD with a 4% compound interest rate calculated in three different ways:

- Annually: 110,412.17 USD

- Monthly: 110,512.24 USD

- Daily: 110,521.28 USD

Long-term loans result in lower monthly payments but higher total interest. The term is the period over which you must repay the loan. Each loan comes with a different term, and you need to choose one that suits your needs. Longer terms typically lead to higher overall interest but lower monthly payments. For instance, if you borrow 20,000 USD for a car with a 5% interest rate, your total repayment will be:

- 24-month term: You’ll pay a total of 1,058.27 USD in interest, with monthly payments of 877.43 USD (principal + interest).

- 30-month term: You’ll pay a total of 1,317.63 USD in interest, with monthly payments of 710.59 USD.

- 36-month term: You’ll pay a total of 1,579.02 USD in interest, with monthly payments of 599.42 USD (principal + interest).

Estimate Payment Amount

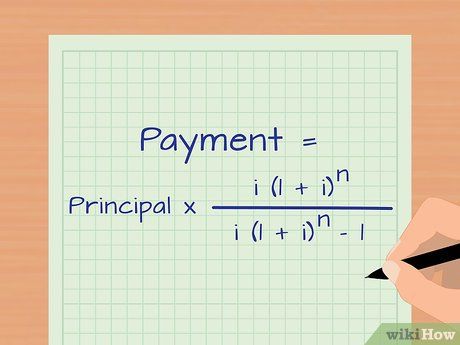

Learn the formula for compound interest.

Learn the formula for compound interest.- "i" stands for the interest rate, while "n" represents the number of payment periods.

- Like most financial formulas, the calculation for periodic repayment is much more complex than simple arithmetic. Once you understand the logic behind the numbers, calculating the periodic payments becomes a breeze.

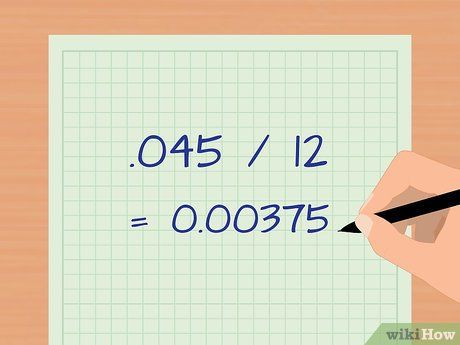

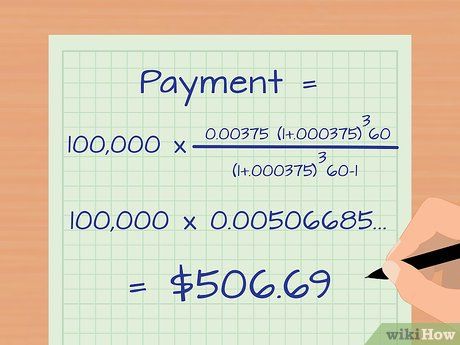

Adjusting the interest payment frequency. Before entering the numbers into the equation, you need to adjust the interest rate frequency, denoted as "i".

- For example, let's say you take a loan at an annual interest rate of 4.5% with monthly repayments.

- Since repayments are monthly, divide the annual rate by 12. 4.5% (0.045) divided by 12 equals 0.00375. Enter this result into "i".

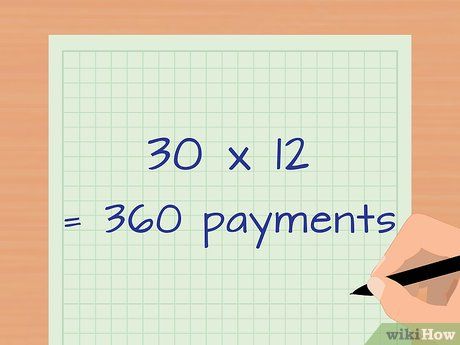

Adjusting the number of repayments. To find out the value of "n", the next step is to calculate the total number of repayments during the loan term.

- If you are making monthly payments for a 30-year loan, multiply 30 by 12. This gives you a total of 360 repayments.

Calculate the monthly repayment amount.

Calculate the monthly repayment amount.

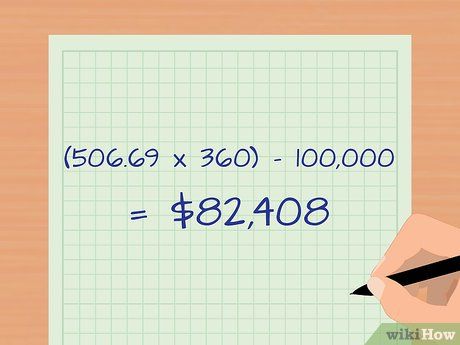

Calculate the total interest to be paid. Now that you know the monthly debt amount, you can calculate the total interest to be paid over the loan term. Multiply the number of payments by the monthly debt amount. Then subtract the principal debt.

- Using the example above, multiply 360 by 506.69 USD to get 182,408 USD. This is the total amount to be paid during the loan term.

- Subtract 100,000 USD from the result, and you get 82,408 USD. This is the total interest you will pay by the end of the loan term.

Calculating Interest with Excel

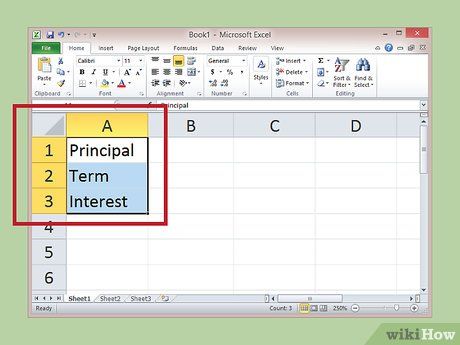

Enter the principal, loan term, and interest rate in one column. Fill in the other fields with their respective values, and Excel will automatically calculate your monthly payment. To help illustrate, use the example below:

- You borrow $100,000 to purchase a house with a 4.5% annual interest rate, for a 30-year term.

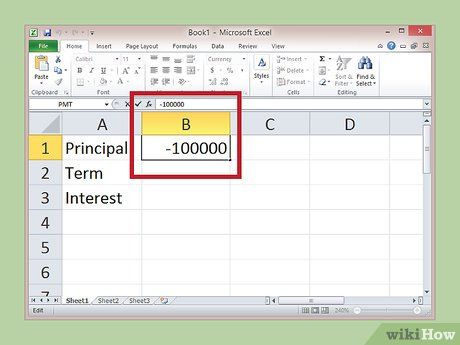

Enter the principal as a negative number. Excel needs to know that you are repaying a loan, so you must enter it as a negative number without any currency symbols ($).

- -100,000 = Principal Amount

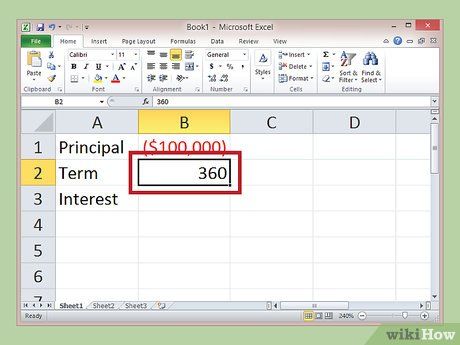

Determine the number of payment periods. You can choose years, but the result will give you yearly payments instead of monthly ones. Since most loans are repaid monthly, simply multiply the number of years by 12 to get the total number of payments. Enter this result in another cell.

- -100,000 = Principal Amount

- 360 = Number of Payments

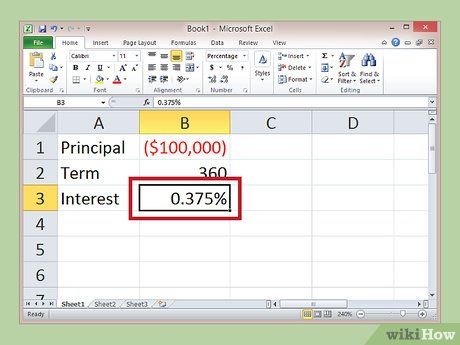

Adjust the interest rate to match the number of payment periods.

Adjust the interest rate to match the number of payment periods.

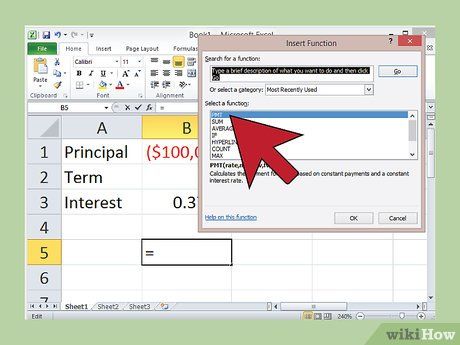

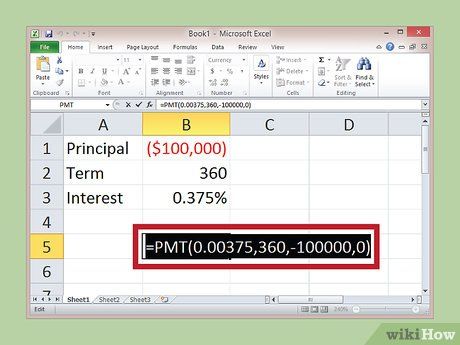

Use the =PMT function to calculate interest payments. Excel can automatically compute monthly debt payments if you know the interest rate. Simply input the necessary information, and Excel will do the calculations. Click on an empty cell, then find the formula bar located just above the spreadsheet (marked as "fx"). Click on it and type "=PMT("

- Do not include quotation marks.

- If you're proficient with Excel, you can create a custom formula to calculate the repayment value.

Input data in the correct positions. Place the values for debt calculations inside parentheses, separated by commas. In this case, you need to enter (interest rate, term, principal debt, 0).

- For the example above, the full data entry would be: "=PMT(0,00375,360,-100000,0)"

- The final number in the sequence is 0. This number signifies that the remaining balance after 360 debt payments will be 0 USD.

- Remember to close the parentheses.

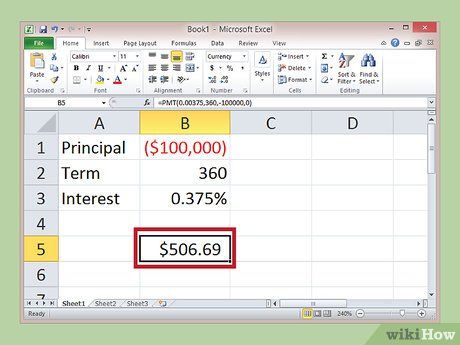

Press Enter to get the monthly debt repayment result. If the formula is entered correctly, you will see the result in the =PMT cell on the spreadsheet.

- In this case, the result will be 506.69 USD. This represents your monthly repayment amount.

- If you see an error like "#NUM!" or an incorrect result, it indicates incorrect data input. Double-check the formula in the formula bar and try again.

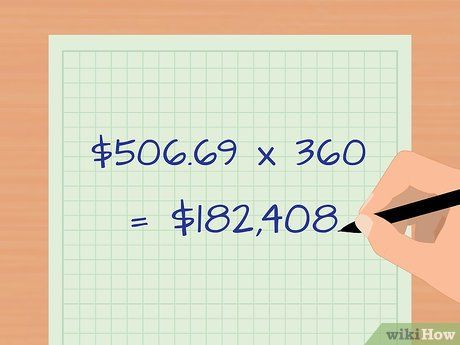

Calculate the total debt repayment by multiplying by the number of installments. To find the total amount to be paid throughout the loan period, simply multiply the periodic repayment by the total number of payments.

- For the example above, multiply 506.69 USD by 360 to get the result 182,408 USD. This is the total amount to be repaid by the end of the loan term.

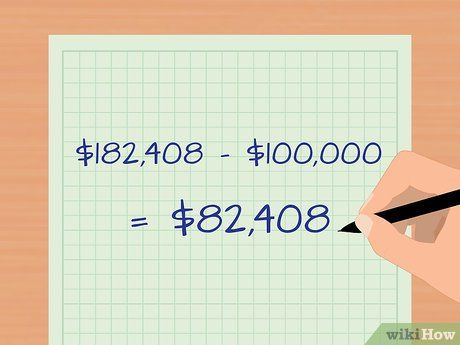

Calculate the interest by subtracting the principal debt from the total repayment. To determine the total interest, perform a subtraction. Take the total debt repayment at the end of the term and subtract the principal debt.

- In this case, subtract 100,000 USD from 182,408 USD. The result will be 82,408 USD, which is the total interest to be paid.

Create a Sample Spreadsheet for Loan Interest Calculation

| A | B | C | D | |

|---|---|---|---|---|

| 1 | [Nợ gốc] | [Số lần trả nợ] | [Lãi suất] | [Lãi suất/tháng] |

| 2 | Khoản vay âm (-100000) | Tổng số lần trả nợ theo tháng. (360) | Lãi suất, ghi bằng số thập phân. (0,05) | Lãi suất/tháng (chia lãi suất/năm cho 12) |

| 3 | Nợ trả/tháng | FX=PMT(D2,B2,A2,0). CHÚ Ý: Số cuối cùng là số 0. | ||

| 4 | Tổng tiền vay | FX=PRODUCT(D3,B2) | ||

| 5 | Lãi vay | FX=SUM(D4,A2) |

Advice

- Understanding how to calculate loan payments will give you the tools to filter out unsuitable loans.

- If your income is irregular and you're considering a loan with a higher interest rate but lower periodic repayments, opting for a longer loan term could be more beneficial, despite the higher total interest over time.

- If you're able to save more than necessary and seek the lowest possible interest rate to meet your needs, a short-term loan with higher periodic payments and lower total interest might be more suitable for you.

Warning

- Sometimes, the lowest interest rate doesn't necessarily mean the lowest borrowing cost. By fully understanding how interest is calculated, you'll be able to quickly determine the true 'cost' of a loan compared to the benefits gained from it.